Australian major banks keep printing despite volatility

Rising inflation and geopolitical risk created turbulent market conditions in March, leading Australia’s big-four banks to push on with funding tasks via covered-bond issuance. Westpac Banking Corporation also reopened the Australian dollar credit market with a significant pricing concession to secondary marks.

Laurence Davison Head of Content KANGANEWS

Lisa Uhlman Senior Staff Writer KANGANEWS

When markets are volatile and issuance windows shrink, the purpose of the covered-bond asset class is to provide a defensive funding platform. This is not lost on Australia’s major banks, which tapped the market during March’s elevated volatility.

ANZ Banking Group and Westpac Banking Corporation printed €1.75 billion (US$2 billion) three-year and £700 million (US$928 million) four-year covered bonds on 8 March. National Australia Bank followed the day after with a four-year €1.5 billion deal. ANZ New Zealand was last to market, issuing a €750 million five-year covered bond on 14 March.

Lucy Carroll, Sydney-based director, global funding at Westpac, says volatility made the covered-bond product a natural choice. She adds the asset class has remained available for issuers to achieve their primary-market goals, despite secondary spread moves globally.

“It felt like the right trade and right product to do. Making the right funding decisions ensures we stay ahead when things become increasingly volatile and that we are not forced into markets at any point,” Carroll tells KangaNews.

Only two days after its covered bond, Westpac executed a A$2.5 billion (US$1.9 billion) three-year, senior-unsecured transaction. Alex Bischoff, managing director, balance sheet, liquidity and funding at Westpac in Sydney, says the bank was contemplating the Australian dollar market when it executed in the UK.

“The advice we were receiving from our institutional bank suggested there was strong liquidity in the domestic market, with three years being the right tenor for a volatile environment,” he reveals.

Bank of New Zealand likewise chose two-year tenor for its first domestic benchmark deal of the year to meet institutional investor preference in a turbulent market and to fulfil a specific balance-sheet management goal of its own.

Lucy Carroll, Sydney-based director, global funding at Westpac, says volatility made the covered-bond product a natural choice. She adds the asset class has remained available for issuers to achieve their primary-market goals, despite secondary spread moves globally.

“It felt like the right trade and right product to do. Making the right funding decisions ensures we stay ahead when things become increasingly volatile and that we are not forced into markets at any point,” Carroll tells KangaNews.

Only two days after its covered bond, Westpac executed a A$2.5 billion (US$1.9 billion) three-year, senior-unsecured transaction. Alex Bischoff, managing director, balance sheet, liquidity and funding at Westpac in Sydney, says the bank was contemplating the Australian dollar market when it executed in the UK. “The advice we were receiving from our institutional bank suggested there was strong liquidity in the domestic market, with three years being the right tenor for a volatile environment,” he reveals.

Bank of New Zealand likewise chose two-year tenor for its first domestic benchmark deal of the year to meet institutional investor preference in a turbulent market and to fulfil a specific balance-sheet management goal of its own.

BNZ’s domestic return hits issuer and investor tenor preference

Bank of New Zealand (BNZ)’s March transaction is the second local big-four bank benchmark deal for 2022. Market participants are optimistic volatility will temper the corporate issuance pipeline.

Bank of New Zealand (BNZ)’s March transaction is the second local big-four bank benchmark deal for 2022. Market participants are optimistic volatility will temper the corporate issuance pipeline.

BNZ’s NZ$750 million (US$515.4 million) deal is the country’s largest bank transaction since Westpac New Zealand’s NZ$900 million five-year print in 2019. BNZ’s bond was also a purely institutional trade, where most local credit deals in 2022 have leaned heavily on retail investors. Wholesale accounts are exhibiting shorter tenor preferences in the newly volatile market environment. “We identified healthy demand in short-dated paper – meaning two years or less, and definitely not as long as three years,” says Mike Faville, head of debt capital markets at BNZ in Auckland. “Investors have been selling equities and duration, so two years certainly fits a buy-side preference for putting cash to work.”

Westpac’s local deal priced at 69 basis points over swap, 22 basis points wider than National Australian Bank’s A$850 million tranche issued in February – the most recent previous big-four bank three-year senior deal in Australian dollars. Market users say Westpac’s level reset the secondary market 6-10 basis points wider following minimal trading volume in recent weeks.

Bischoff says the premium was the right balance given market risk and allowed the issuer to find strong underlying demand at the new level. The book closed at around A$3.9 billion, allowing scaling of bids.

The deal outcome was also sufficient to persuade other issuers to return to the primary market in the following days. Bendigo and Adelaide Bank issued A$750 million of three-year notes on 11 March – at 98 basis points over swap – and on 16 March Svenska Handelsbanken priced three- and five-year tranches at 85 and 110 basis points over swap benchmarks.

Westpac’s final margin does not represent a cost of funds out of line with the historical three-year major bank issuance range and remains attractive to the issuer, Bischoff says.

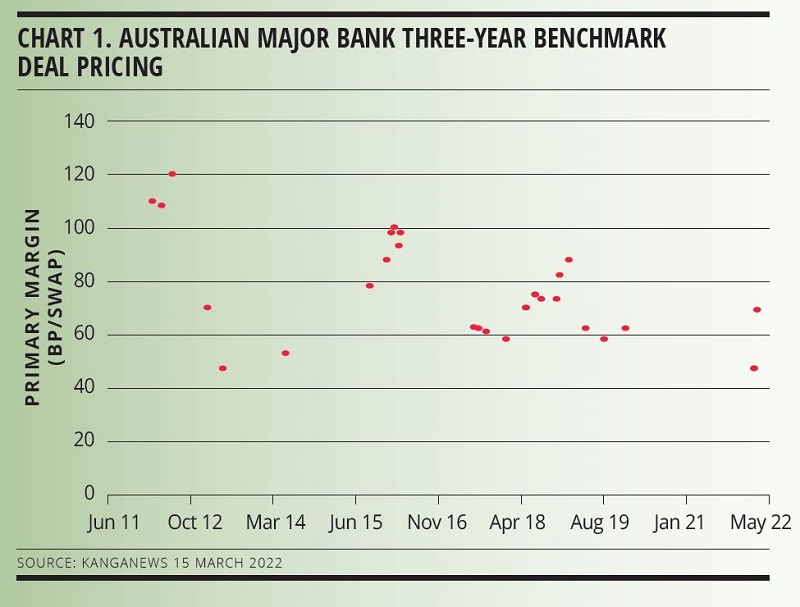

KangaNews data confirm pricing is in line with typical issuance levels from prior to the start of the COVID-19 pandemic. The average margin for major-bank three-year domestic benchmarks over the past decade is 75 basis points over swap, making Westpac’s latest print if anything slightly tighter than the long-run norm (see chart 1).

“The size and diversity of the book supported our view that we had the right clearing price,” Bischoff tells KangaNews. “We launched the deal after a more positive overnight session – allowing demand to drive the final landing point.”

ANZ’s covered-bond deal was particularly significant because, unlike the other major banks, the issuer has not completed any benchmark wholesale issuance since the end of the Reserve Bank of Australia’s term-funding facility (TFF) in June 2021. It has not issued an unsubordinated benchmark bond since January 2020.

The timing of ANZ’s latest transaction was “a question of monitoring customer balance sheet dynamics and our funding position”, says Simon Reid, director, group funding at ANZ in Melbourne. “We have had a very different balance sheet position from some of our peers,” Reid says. “We are also probably a little less focused on TFF refinancing, as we have a smaller TFF than some of our peers.”

Reid also points to ANZ’s smaller committed-liquidity facility, which it has reduced proactively. The bank has also enjoyed strong deposit growth and a stable asset book, he continues.

It felt like the right trade and right product to do. Making the right funding decisions ensures we stay ahead when things become increasingly volatile and that we are not forced into markets at any point.

DEAL DYNAMICS

ANZ’s March 2025 covered-bond transaction priced at 7 basis points over mid-swap after launching in the 12 basis points area, while NAB’s March 2027 transaction priced at 12 basis points over mid-swap. Previously, Commonwealth Bank of Australia (CBA) executed a February 2028 euro covered bond on 16 February that priced at 10 basis points over mid-swap.

“Pricing was broadly in line with expectations but we were positively surprised with the size of demand,” Reid tells KangaNews. “We value the euro covered-bond market because it offers reliable access to term funding in difficult market conditions and it is clear the sector has grown since the last time we issued there.” He adds that ANZ was able to access a larger volume of funding than it expected at the price it was looking to achieve.

Westpac’s four-year floating-rate sterling deal priced at 45 basis points over SONIA – in line with guidance. NAB priced a £1.5 billion December 2025 covered bond in December with a margin of 27 basis points over SONIA.

Westpac’s covered bond represents the bank’s first issuance in sterling since January 2018. Having issued covered bonds in the euro and US dollar markets in the past six months, Carroll says the sterling market suited the bank’s needs and allowed it to issue into a diversified pool of demand.

“It definitely felt like there was some capacity in the market,” she explains. “It was a good funding opportunity from a relative-value basis versus covered options in euros and US dollars, as well as offering the volume we were targeting.”

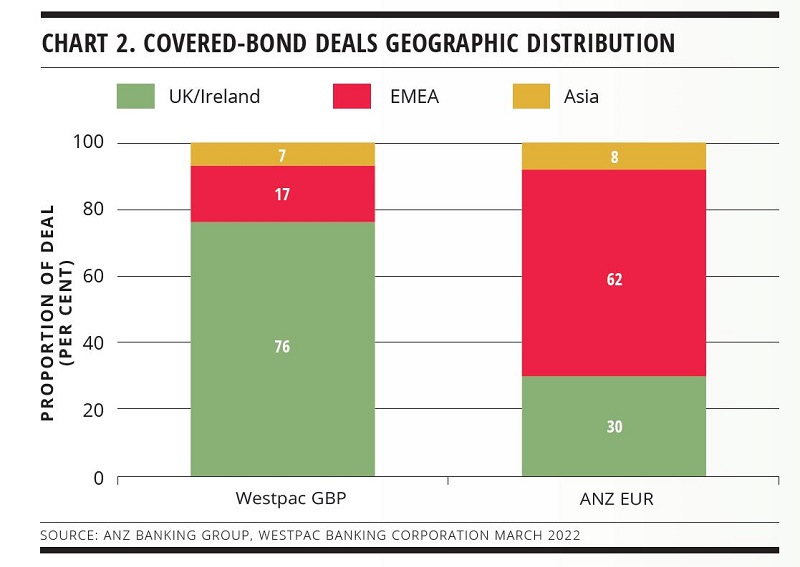

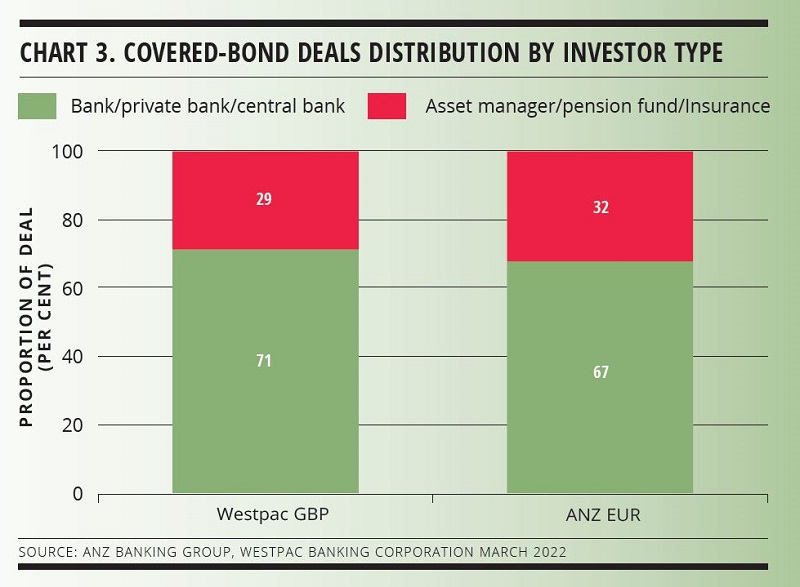

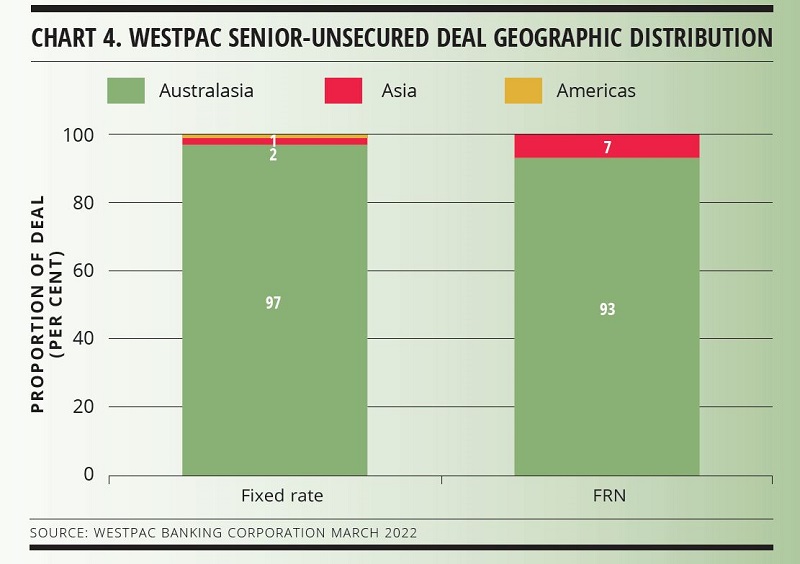

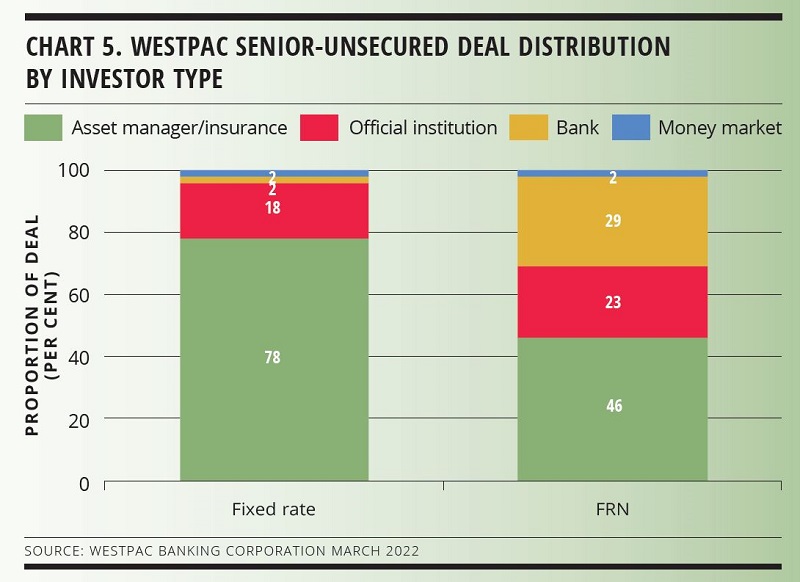

Bank books took most of the deals, while investors from Ireland and the UK dominated the Westpac sterling deal (see charts 2 and 3). The final book for Westpac’s domestic senior-unsecured deal skewed heavily to local investors (see chart 4).The real-money bid was notably strong, especially in the fixed-rate note (see chart 5). “The size and diversity of the book supported our view that we had the right clearing price,” Bischoff says.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news