Deeper roots support corporate issuance in Australia

Not long ago, the Australian corporate credit market was struggling to shake off the perception of being the first to close and the last to reopen. While corporate deal flow has been limited in 2022, investors and intermediaries say there has not been a full-scale retreat of liquidity – which represents a step-change in market maturity.

Dan O'Leary Editor KANGANEWS

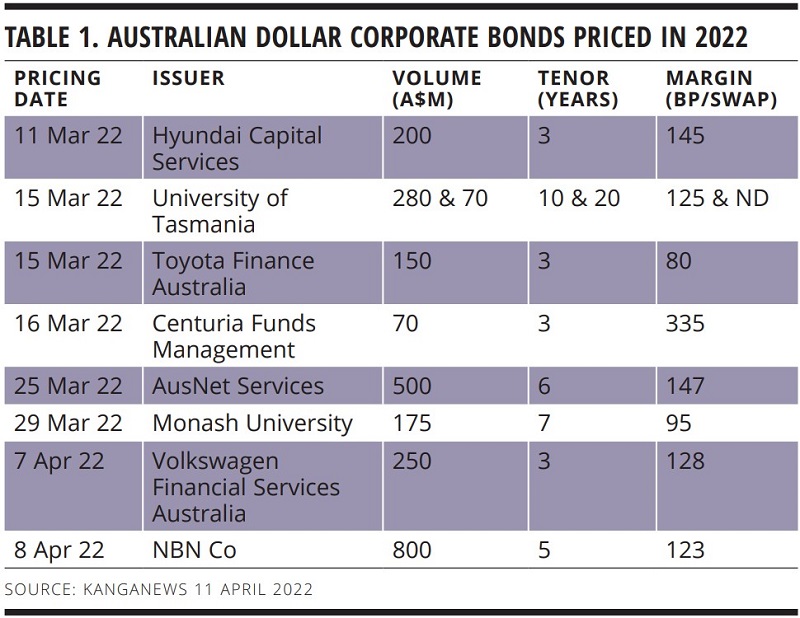

The Australian dollar corporate credit market recorded decent primary deal flow from early March onwards (see table 1) despite a slew of fear-inducing headlines concerning rising inflation, an interest rate sell-off and the start of Russia’s invasion of Ukraine.

Uncertainty typically leads to lower Australian dollar corporate issuance as borrowers either avoid the market completely – often reverting to bank loans for refinancing – or print offshore. For instance, no deals were recorded in Q1 2008, the height of the financial crisis, while the January 2016 sell-off of Chinese equity markets also correlated with low Q1 Australian dollar corporate credit volume. However, a slow start is not necessarily a precursor of low full-year volume: the turmoil of early 2020, for instance, was followed by a surprisingly active corporate issuance environment over the course of the year.

SLOW AND STEADY

Participants from all sides of the market say the steady flow of deals in 2022, while smaller than usual, is an encouraging sign of the growing resilience of the Australian dollar funding option. As is often the case in the local market, limited corporate issuance appears to be driven at least as much by supply factors as any jitters on the buy side.

Michael Larkin, group treasurer at Lendlease in Sydney, says the Australian market is a different proposition than it was even five years ago. “The market has continued to develop and grow – it is deeper and broader,” he comments. “I am not concerned if we have slower periods because, taking a step back and looking at the trajectory of the market overall, it has developed significantly and in a positive way.”

Corporate issuers priced about A$20 billion (US$15.6 billion) in the Australian dollar market in 2021, the highest volume year since 2017 and the second largest of all time. Stability and lack of competition certainly helped, as the Australian economy reopened while banks spent much of the year well supplied with wholesale funding from the Reserve Bank of Australia.

Indeed, part of the reason flow has been limited so far in 2022 could be issuers moving to take advantage of the positive environment last year. Lendlease, for example, finalised more than A$3 billion of green or sustainability-linked bonds (SLBs) and sustainability-linked bank facilities over the last 18 months, adding more than A$1 billion in SLBs and sustainability-linked loans for Lendlease managed funds over the same period.

“Market conditions were conducive last year and we felt there was a reasonable likelihood that rates were going to rise, so we wanted to get to market while conditions were amenable,” Larkin notes. “It is possible other issuers are ahead of their funding requirements, too – so they can now sit and wait to see how volatility plays out.”

For Phil Schretzmeyer, Sydney-based head of treasury and group planning at Charter Hall Group, the funding task is never complete so the company will consider issuance throughout market cycles. Nonetheless, Charter Hall was active in the positive environment of 2021. It printed three Australian dollar transactions last year, totalling A$950 million.

“We want to grow our Australian dollar MTN presence – our focus is the domestic market,” Schretzmeyer says. “We are not finished as an issuer, but it is about timing.”

He agrees the Australian corporate bond market has become more resilient, though with the caveat that more issuance is needed to demonstrate this resilience through the cycle and across market conditions.

“Some corporates have issued equity and some have tapped loan markets, while the pandemic has affected some such that they may be waiting to tell a better story. Others may not have any near-term funding needs. Many factors have contributed to the slow start in bond issuance this year aside from market volatility.”

Button TextTENOR OPTIONS

Issuers do not judge the supportiveness of the local market just on deal activity. There is also greater confidence nowadays that extended duration can be available in Australian dollars. This can be critical for some issuers.

Michael Momdjian, general manager, treasury, tax and insurance at Sydney Airport, says 10-year triple-B supply in Australia was rare prior to 2020. He tells KangaNews: “Over the last few years, I can no longer count 10-year triple-B issuance in the local market on just one hand. The market has definetly started to support longer-dated issuance.”

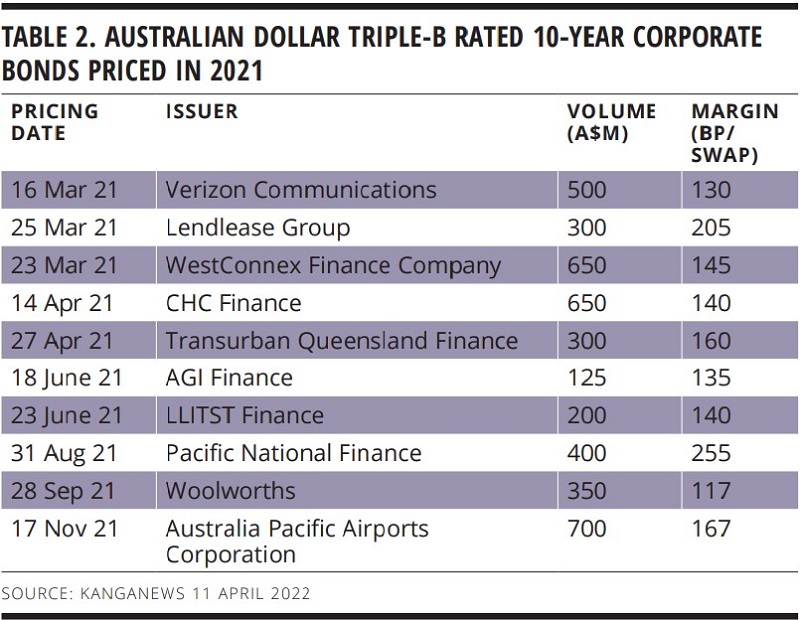

Triple-B rated corporate borrowers issued A$4.2 billion of 10-year bonds last year, in 10 deals (see table 2). This volume built on the momentum from the A$3.7 billion that came to market across nine deals in 2020.

Momdjian says Sydney Airport wants to diversify its funding sources through local bond issuance, but he highlights the importance of staying relevent in the world’s deepest and most liquid bond markets. “Our first ever 10-year US dollar bond matured earlier this year, with another due to mature in less than 12 months’ time,” he says. “Diversification is only one of many funding objectives we strive to achieve. We also need to remain relevant in our core funding markets.”

Sydney Airport has tapped the equity market for its funding requirements over the last two years. However, a consortium led by New York-based Global Infrastructure Partners and IFM Investors bought the company in 2022 and subsequently took it private, which changes the company’s funding plans independent of market behaviour.

Momdjian adds: “Some corporates have issued equity and some have tapped loan markets, while the pandemic has affected some such that they may be waiting to tell a better story. Others may not have any near-term funding needs. Many factors have contributed to the slow start in bond issuance this year aside from market volatility.”

Of the eight corporate credit deals priced by 11 April 2022, four were direct refinancing of facilities maturing this year.

“Market conditions were conducive last year and we felt there was a reasonable likelihood that rates were going to rise, so we wanted to get to market while conditions were amenable. It is possible issuers are ahead of their funding requirements, too – so they can now sit and wait to see how volatility plays out.”

Button TextA LINE IN THE SAND

While corporate issuance has been limited, the Australian dollar credit market overall has shown a good degree of resilience and openness to new issuance. Financial institution transactions were key to kick starting the Australian dollar corporate credit market in 2022. As more deals printed, investors and issuers alike gained greater clarity on pricing and market appetite.

Richard Garland, senior portfolio manager at QIC in Brisbane, says the three-year deal Westpac Banking Corporation priced on 10 March confirmed a new, wider level for local spreads that had been prefigured by a Commonwealth Bank of Australia (CBA) US dollar deal a week earlier.

The Westpac transaction offered a significant pricing concession to major bank secondary marks and earlier new issuance. It printed at 69 basis points over swap, 22 basis points wider than National Australia Bank (NAB)’s three-year tranche issued in February.

“We see this often in Australia: persistent volatility offshore leads to secondary trading falling away,” Garland adds. “Spreads are stagnant, which gives a false sense of resilience and we need new supply to reprice the curve. New senior major bank issuance is particularly helpful because sell-side traders use it as an input for where they price other parts of the market.”

Since the Westpac deal there have been further encouraging signs of robust underlying demand for credit. Suncorp and CBA have both tested the waters for subordinated issuance while AusNet Services and NBN Co printed 2022’s first true corporate deals of A$500 million or more. Such outcomes can establish confidence for other corporate names. “From an issuer’s perspective, we are watching what happens in this period of instability,” Schretzmeyer says. “When a large corporate transaction takes place it really sets the market.”

Barry Sharkey, Sydney-based partner at Barrenjoey, says the AusNet deal recorded strong investor interest with an orderbook topping A$1.1 billion at peak. The Barclays-Barrenjoey joint venture was joint lead manager on the deal with ANZ and NAB.

“In volatile conditions, primary transactions can play an important role in resetting secondary trading levels. This is particularly the case in the Australian dollar market, where secondary can be less active than in larger, more liquid jurisdictions. A new primary issue can sometimes reprice an issuer’s secondary curve, rather than the opposite,” Sharkey says.

He adds that more primary issuance is always welcome and a boost to confidence. “I’m not sure whether AusNet has broken the dam, but I expect to see other issuers of all types now look at the market,” he tells KangaNews.

“We see this often in the Australian market: persistent volatility offshore leads to secondary trading falling away. Spreads are stagnant, which gives a false sense of resilience and we need new supply to reprice the curve."

Button TextExpectations readjusted as volatility grows

As spreads widen, market participants say expectations on both sides of the market have to reset. Issuers need to rein in assumptions on pricing, tenor and size while investors may have to adjust their demands on deal execution.

In volatile times, issuers and syndicate desks want to price deals rapidly to reduce execution risk.

But the time given to conduct adequate due diligence is a perennial gripe for many Australian investors. In a volatile market, deals priced intraday, coming to market late on a Friday or closing after 4:30pm Sydney time make it difficult for investors to mark trades.

Phil Strano, senior investment manager at Yarra Capital Management in Melbourne, says if issuers and banks do not run an institutional process a deal will not be classed as institutional “and we will politely decline to participate in these opportunities”. He continues: “I understand the desire to minimise execution risk but investors need time. It is a balancing act between issuers and investors.”

I understand the desire to minimise execution risk but investors need time. It is a balancing act between issuers and investors.

CHANGED FUNDAMENTALS

That issuance is occurring at all during a period of heightened volatility shows the Australian corporate credit market has matured, participants say. While issuers need to reset their expectations on price, size and tenor (see box on facing page) the market should be there if they are flexible and ready to meet Australian dollar investor requirements.

The signs are that the local market has established deeper and more sound foundations over the past decade. For instance, Schretzmeyer comments: “Australian superannuation is growing and it is still in the accumulation phase. This should mean more money domestically that can ideally be allocated to fixed income. Our first issuance domestically was less than two years ago and the market has developed and grown even since then. It is now at a point where we can issue more domestically, which makes sense to do as an Australian company.”

Garland adds that recent volatility has provided some strong all-in yield opportunities and agrees that cash accumulation means investors are generally keen to put money to work. Volatility had not evolved into anything more malign by mid-April although issuers are content to wait for markets to settle, he says.

Widening spreads are actually a welcome factor after a long period of compression. “Investors have built up decent amounts of cash,” Garland says. “AusNet’s orderbook provided stability to the market at pricing that was fair.”

He adds that some deals come to market with wide initial price talk that borrowers are “not afraid to tighten”. AusNet’s deal, for instance, tightened by 13 basis points from guidance while Suncorp’s A$290 million 15-year subordinated note came in 20 basis points inside guidance when it priced on 29 March. Even so, Garland notes that there has still been some value even at final pricing levels

“Interestingly, we have not seen as much follow through in secondary market tightening,” he continues. “We view this as a confluence of continued rates volatility keeping investors cautious and issuers taking out some of the new-issue premium.”

Momdjian adds that local investors have become more sophisticated and mature. “There is an understanding that if domestic investors have money to put to work, they will have to be as competitive as possible,” he tells KangaNews. “Otherwise, issuers that value low execution risk will still go offshore.”

“It is not the end of the story even when we identify material risks. Where we can, we will continue an engagement process with the issuer in the hope that it begins to manage these risks and we can eventually include it in our investible universe.”

Button Text