Risky business

Geopolitical tensions and their ramifications for inflation and rates are driving heightened anxiety among Australian investors, according to the latest Fitch Ratings-KangaNews Fixed-Income Investor Sentiment Survey. But investor responses are far from crisis levels.

Lisa Uhlman Senior Staff Writer KANGANEWS

More than 30 Australian institutional investors completed the survey in March 2022 – the 15th iteration of a survey Fitch and KangaNews conduct annually. Surveys from recent years provide a vivid snapshot of the global cycle as alarm over COVID-19 in 2020 dwindled with last year’s effective pandemic responses only to be displaced by fears about Russia’s invasion of Ukraine.

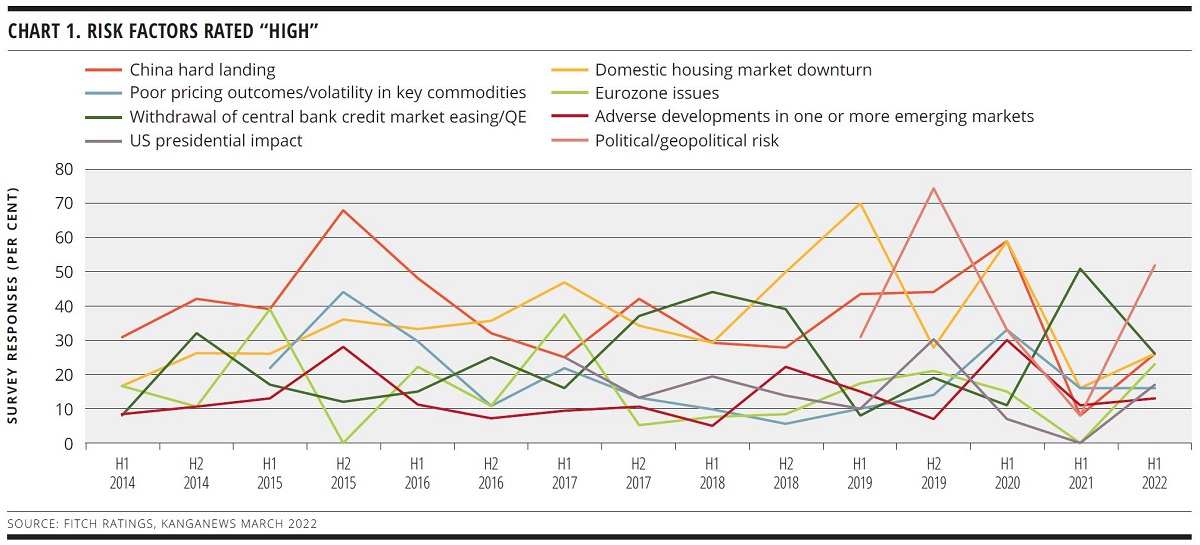

More than half the survey respondents say geopolitical concerns present the highest risk to credit markets in the coming year (see chart 1). Risk perception has drifted higher across the board: only one of the eight risk factors highlighted by the survey – the withdrawal of QE – worries investors less this year than it did in 2021. However, only around a quarter of investors rate any individual risk apart from geopolitical as “high”.

The transmission mechanism by which the conflict in Ukraine could have a negative impact on the Australian fixed-income market is clear: elevated oil and gas prices add yet more weight to the inflation story, placing upward pressure on rates and the cost of credit.

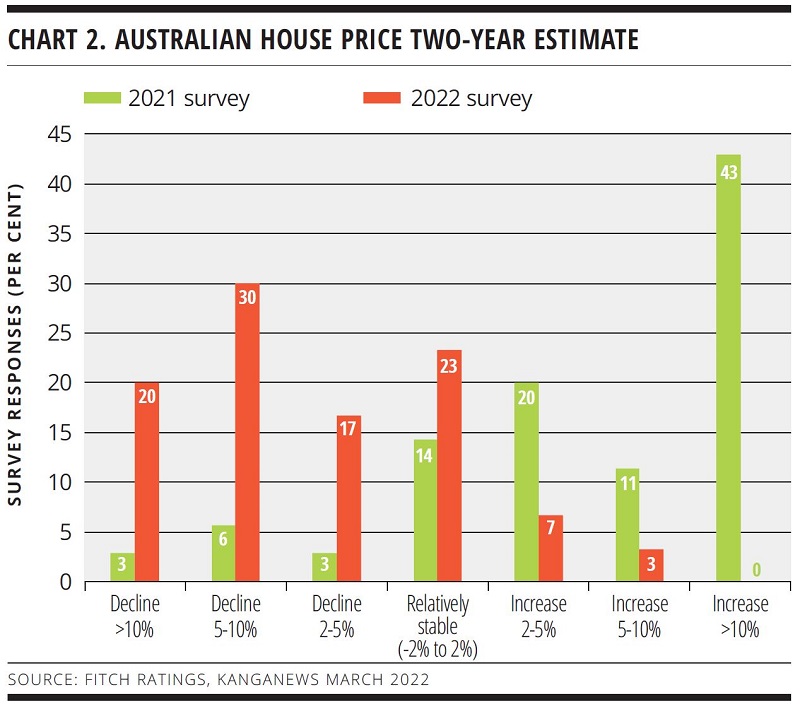

Investors are conscious of the potential impact on domestic sectors like housing. While 74 per cent of March 2021 survey respondents believed house prices would increase over the next two years, in March 2022 the equivalent figure dwindled to 10 per cent. None expect double-figure growth (see chart 2).

Fitch’s analysts say the knock-on effects of the war are eroding confidence engendered by Australia’s pandemic outcome. “Prior to Russia’s invasion of Ukraine, the global economic recovery from the effects of the COVID-19 pandemic was on track,” Fitch says, noting Chinese, Eurozone and UK annual growth beat forecasts in 2021.

But the rating agency’s survey report continues: “However, the war in Ukraine and the economic sanctions on Russia, which are unlikely to be rescinded any time soon, have put global energy supplies at risk. The jump in oil and gas prices will add to industry costs and reduce consumers’ real incomes.”

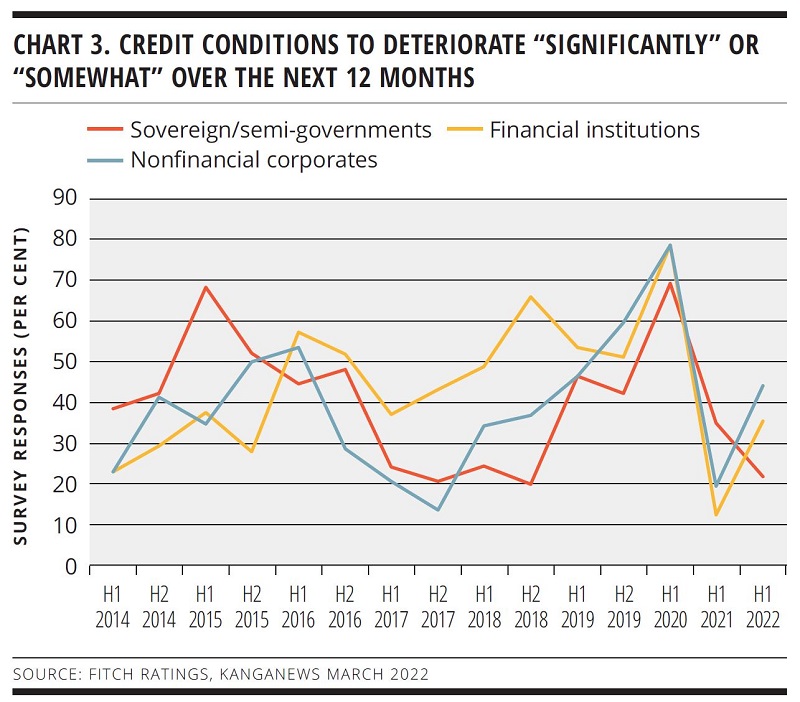

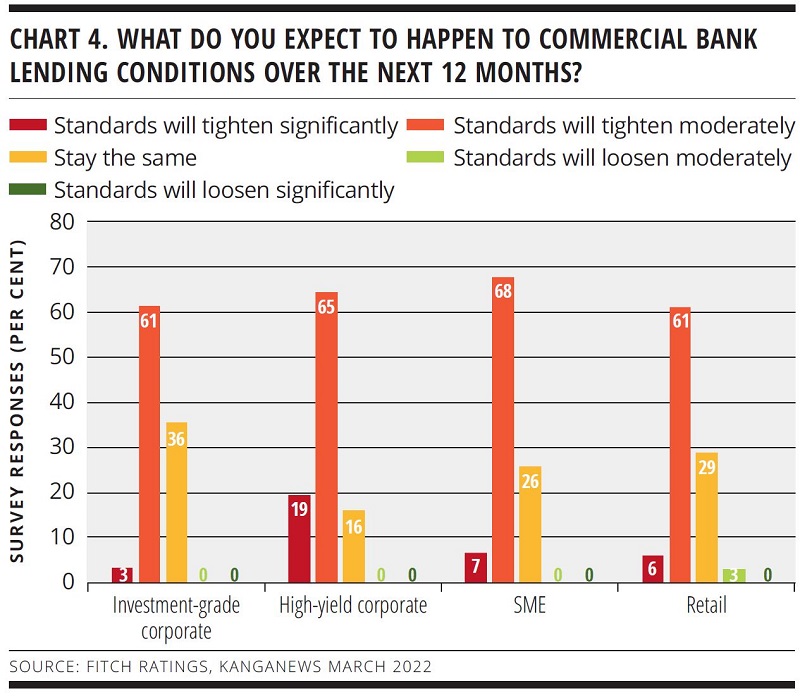

Investors are also more pessimistic about credit conditions in 2022 than they were in 2021, when no more than 20 per cent of survey respondents expected conditions to deteriorate for financial institutions or corporates. The numbers double in 2022 (see chart 3). There is also a negative outlook on commercial banks’ lending conditions over the next year (see chart 4).

While there is undoubtedly a pessimistic tone to the survey, investors do not appear to believe the Australian economy or market is at crisis point. Risk-factor concern and expectations of weaker credit conditions are well below their peaks. Even geopolitical concern is notably lower in 2022 than it was in late 2019, when the relevant global events were US-China trade tensions and a possible no-deal Brexit.

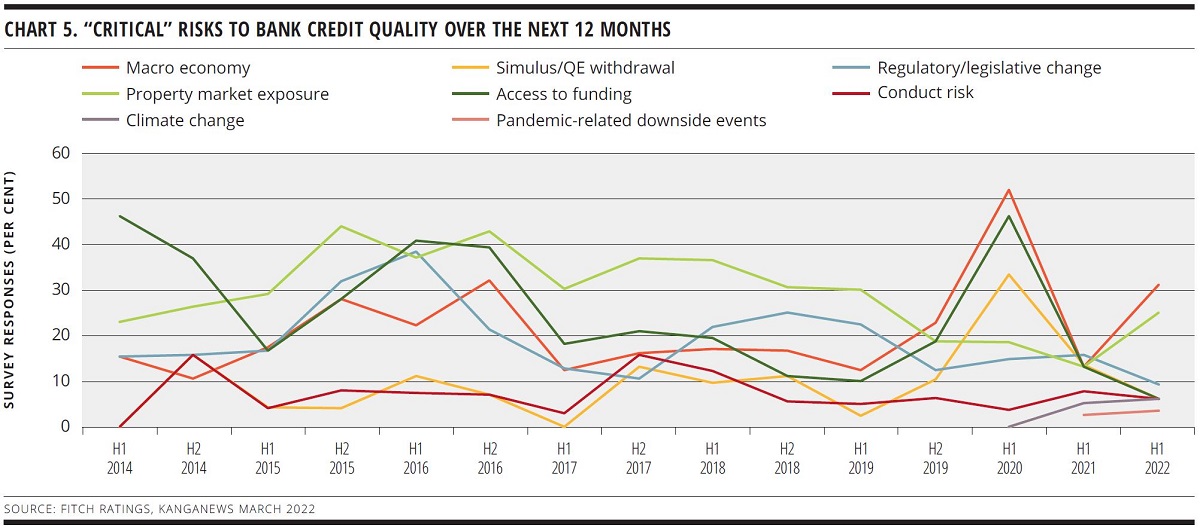

Perceptions of risks to Australian bank credit have changed since the 2021 investor survey, although investors are less negative here than in other areas. Macroeconomic factors and the Australian property market are at the forefront of respondents’ concerns about bank credit quality over the next 12 months while most other risk factors have declined in investor minds (see chart 5).

RATES TO RISE

Fitch’s analysts predict conditions for Australian banks will be steady in 2022. They expect GDP to grow this year while inflation will prompt the cash rate to rise by 65 basis points in the second half. “This, combined with the removal of pandemic support measures, could see asset quality weaken modestly,” Fitch’s survey report says.

“However, losses are likely to remain low due to adequate provisioning, tightening in underwriting in the years leading up to the pandemic and strong property prices, which should assist with resolution of nonperforming loans,” Fitch adds. “Rising rates are likely to slow house price and loan growth but should support bank net interest margins and, ultimately, profitability.”

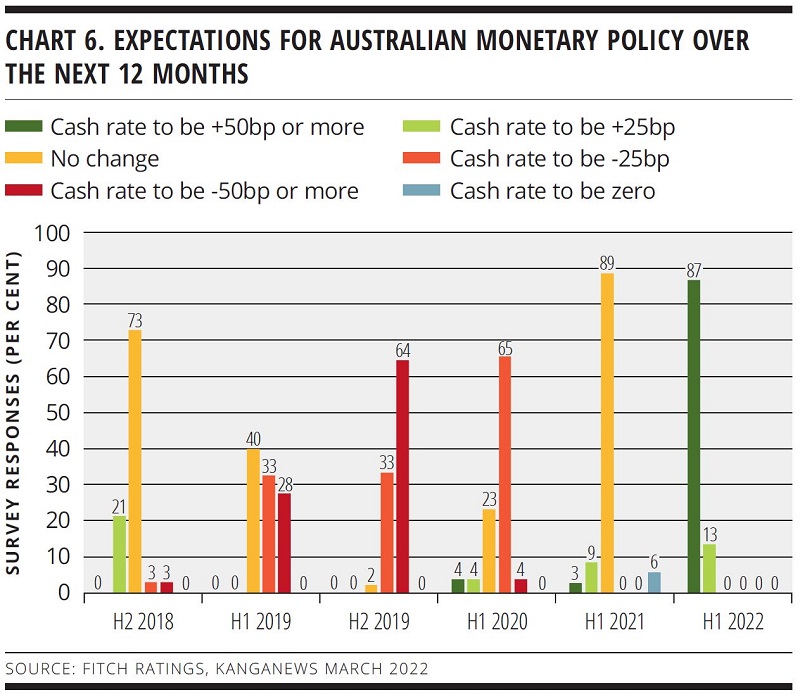

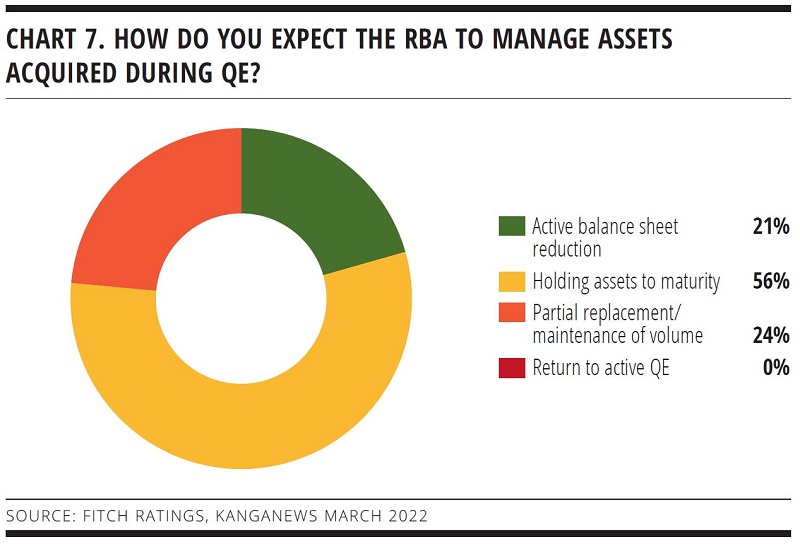

Nearly all survey respondents agree that the cash rate will rise by at least 50 basis points in the next year (see chart 6). However, the Reserve Bank of Australia’s notably dovish language – at least relative to other global central banks like the US Federal Reserve and Reserve Bank of New Zealand (RBNZ) – also has an impact on investors’ expectations about QE assets. The RBNZ has announced plans to sell down some of its QE holdings but barely 20 per cent of Australian investors expect their central bank to follow suit (see chart 7).

This is despite a generally positive economic environment. Fitch notes the Australian economy grew by 3.4 per cent from the onset of COVID-19 to end 2021 and that GDP is now nearly back to its pre-pandemic implied path. “Inward migration has resumed gradually with the reopening of international borders in February,” the Fitch report points out. “This will add further impetus to the economic recovery, while elevated commodity prices are adding further support through higher mining-sector export earnings and outbound liquefied natural gas shipments as importers look for non-Russian sources.”

INVESTMENT OUTLOOK

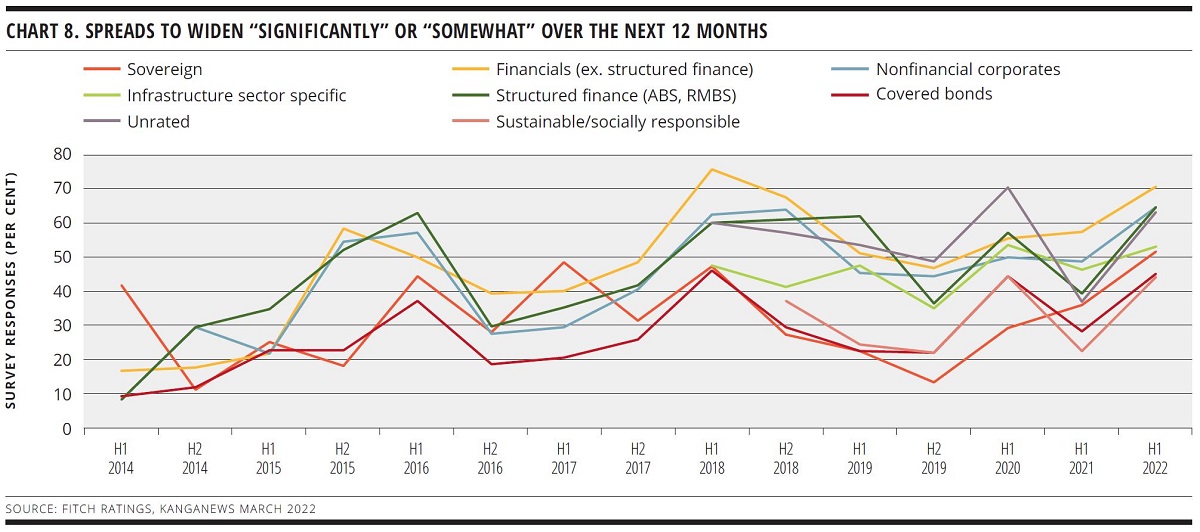

Even so, survey respondents in 2022 anticipate spreads will widen across all asset classes over the next 12 months, where 2021’s results predicted spreads would tighten in structured finance, covered bonds and sustainable instruments among other products (see chart 8). Again, however, expectations of spread widening are below peak levels for most asset classes.

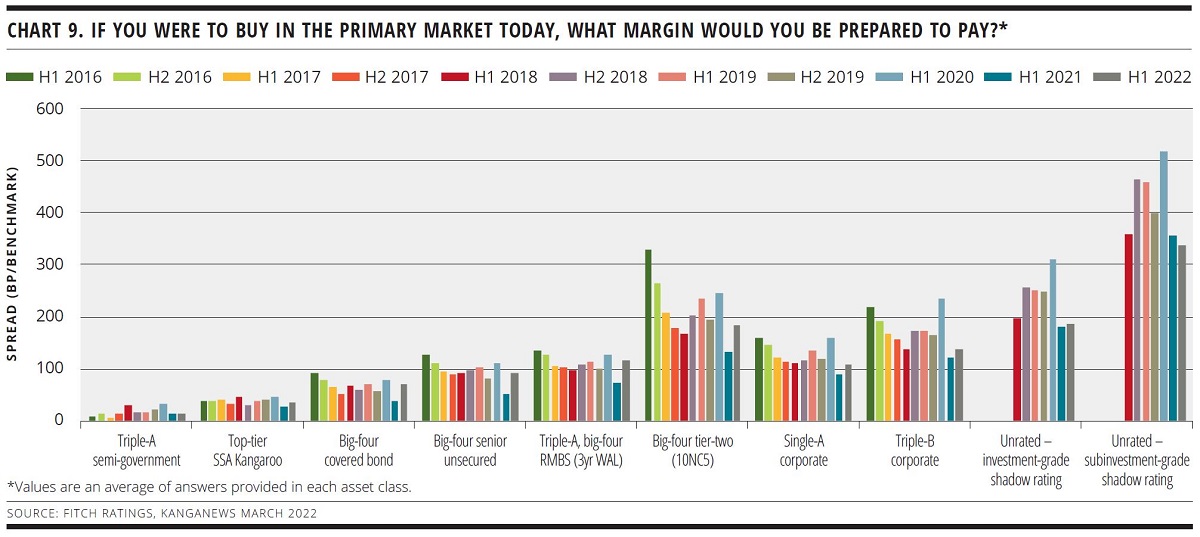

Unsurprisingly, the margin investors say they would pay for various assets widened across most asset classes in this survey compared with 2021’s results; the latter included record-low predictions for many asset classes. However, spreads are still tighter than results from 2020 (see chart 9).

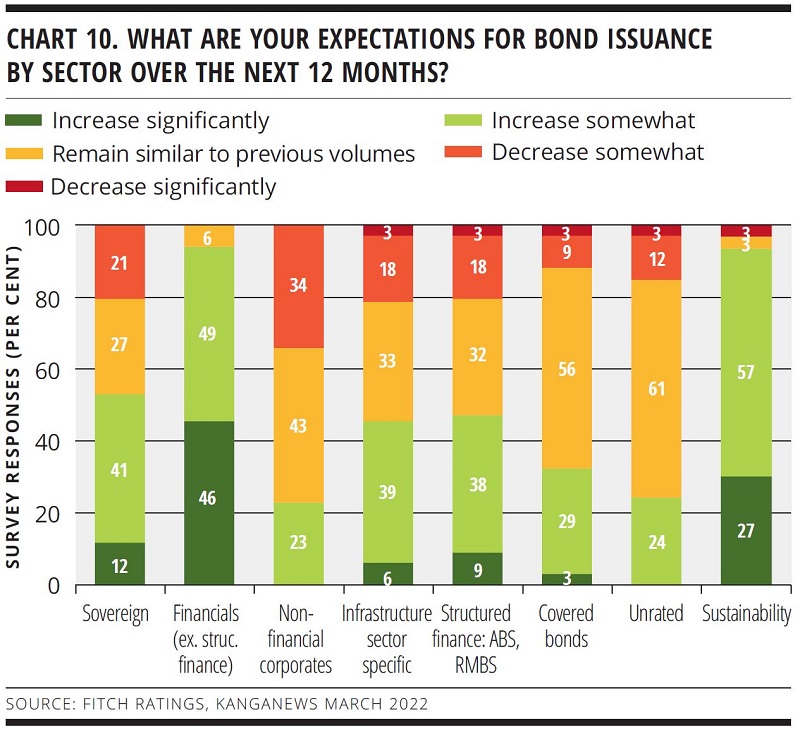

Investors expect bond supply to increase at least somewhat across the board in the coming year, with sustainability-aligned supply notably highlighted for growth (see chart 10).

The 2022 survey addresses, for the first time, respondents’ perception of and approach to environmental, social and governance (ESG) investment issues. The responses show ongoing growth in interest and importance for fixed-income investors.

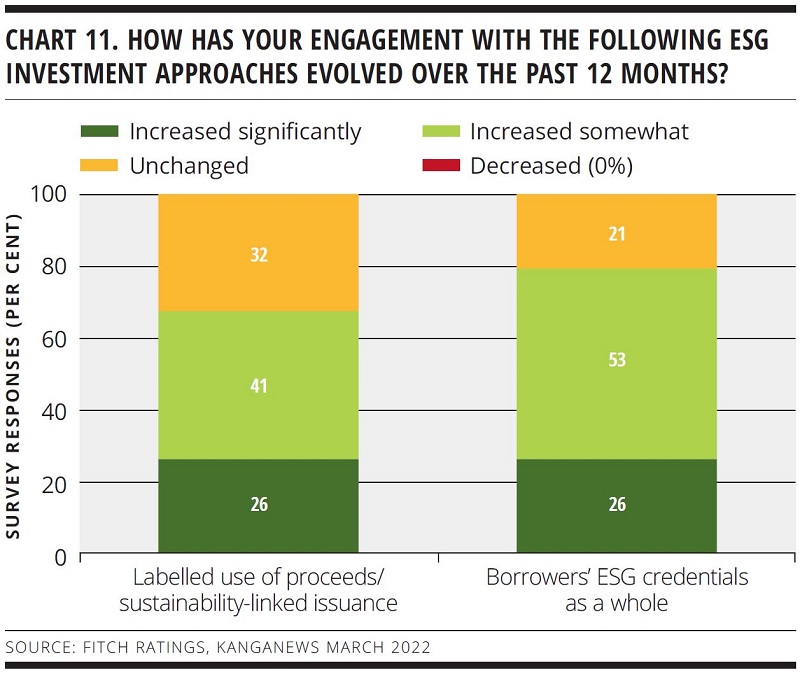

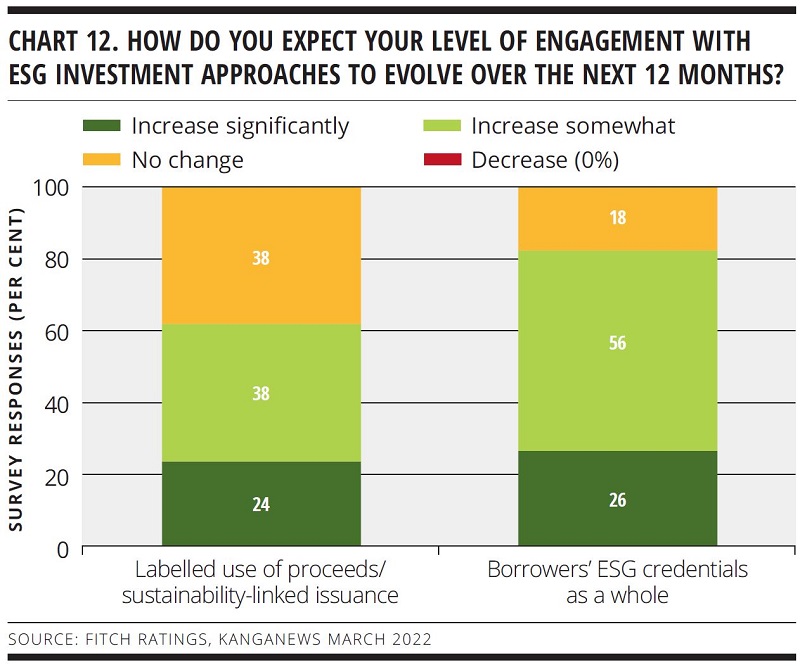

About one-quarter of respondents say their engagement with labelled issuance over the past 12 months increased significantly. Borrowers’ ESG credentials are of even greater importance, with 26 per cent of respondents saying their engagement has been increasing significantly and will continue to do so. More than half of respondents say they will increase engagement with both these approaches; no respondent flagged decreased engagement with ESG investment approaches (see charts 11 and 12).

Sponsored by

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news