Air NZ uses Qantas comp and supportive liquidity to land debut Kangaroo

Air New Zealand says parallels between its credit and that of Qantas helped its debut Australian dollar deal find strong local support as it kicked off the debt side of a major recapitalisation programme announced in March 2022. Familiarity with the Air New Zealand credit provided a good starting point and deal sources say the issuer’s investor engagement and marketing efforts ensured a successful landing.

Air New Zealand printed the A$550 million (US$387.2 million) transaction on 18 May. The issue comprises a A$300 million four-year tranche and a A$250 million seven-year note.

ANZ, Citi, Commonwealth Bank of Australia (CBA) and MUFG Securities acted as joint lead managers (JLMs) on the deal, which is Air New Zealand’s first Kangaroo transaction. It issued New Zealand dollar notes in 2011 and 2016 totalling NZ$200 million (US$127.9 million).

Leila Peters, Auckland-based general manager, corporate finance at Air New Zealand, tells KangaNews the airline wants to establish an ongoing relationship with the Australian investor base. Australia is the number-one international tourist market into New Zealand and the airline has material Australian dollar revenues, she adds.

“There is also a degree of familiarity with the Air New Zealand credit, given the [status of] Qantas in Australia, so we viewed it as a really attractive market to achieve what we were looking to do – which was quite a bit of volume,” Peters tells KangaNews.

Keith Mitchell, Sydney-based director, debt capital markets at Citi, says Australian investors responded well to the credit. “The similarities [between Air New Zealand and Qantas] resonated with investors, such as the domestic market share that each of them holds and the fact that they are flag carriers for their respective countries,” Mitchell explains.

The transaction was not just a positive outcome for the issuer but also speaks to the ongoing functionality of the Australian dollar corporate market despite limited recent deal flow.

Gwen Greenberg, Sydney-based executive director, debt capital markets at ANZ, comments: “This was a very good transaction and a strong result, especially in the context of what Air New Zealand set out to accomplish as a debut issuer. It is also the first corporate deal to price since early April, and it achieved a strong result and good volume across two tranches that worked well within the issuer’s debt maturity profile.”

Peters adds: “We would not have gone to the market if conditions were not conducive – it is something we had been monitoring very closely over the last few weeks, given volatility certainly has increased.”

On 30 March, the airline launched a NZ$2.2 billion recapitalisation package to fund its COVID-19 recovery strategy and maintain its Baa2 stable rating. Air New Zealand has traditionally relied on secured financing, including for a recent refresh of its fleet, but it is now adding unsecured debt as a means of diversifying its portfolio, according to Peters.

The bond issue, which the airline had targeted at NZ$600 million equivalent, follows a successful NZ$1.2 billion equity raise Air New Zealand completed on 5 May. The company will use the bond proceeds partially to buy back preference shares previously issued to the New Zealand government – a majority holder of the airline’s equity.

“This was a very good transaction and a strong result, especially in the context of what Air New Zealand set out to accomplish as a debut issuer. It is also the first corporate deal to price since early April, and it achieved a strong result and good volume across two tranches that worked well within the issuer’s debt maturity profile.”

DEAL DYNAMICS

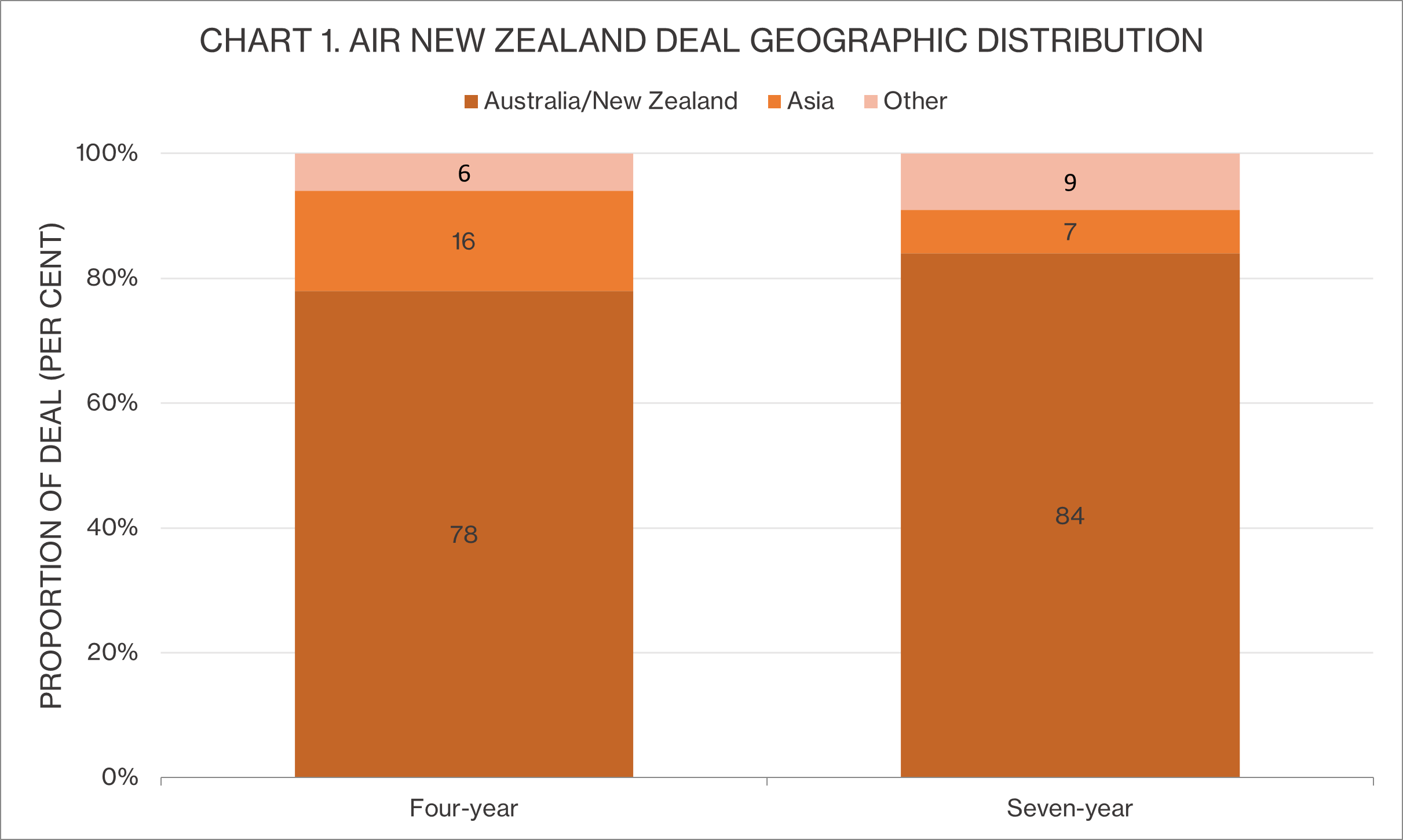

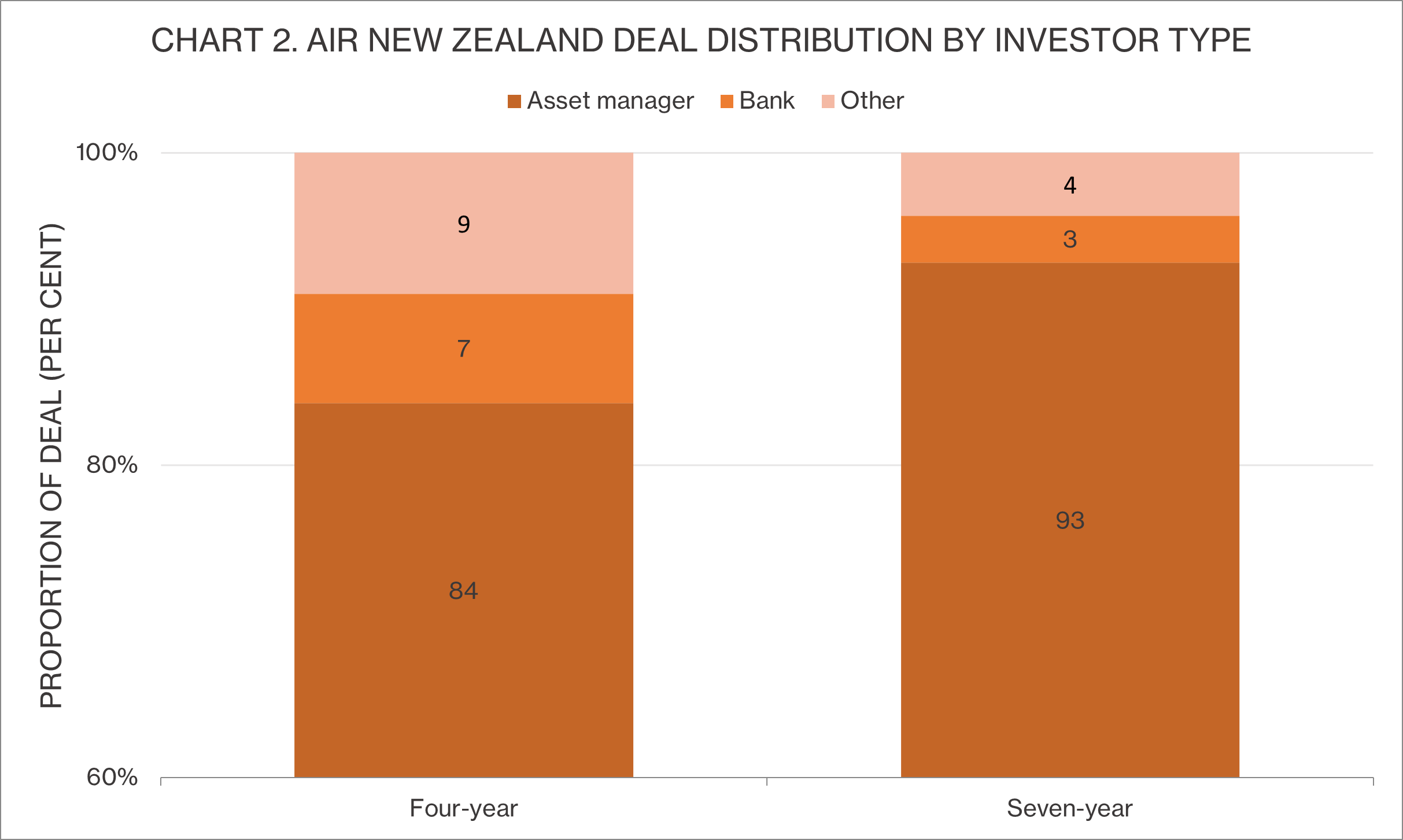

Australia and New Zealand investors dominated both tranches of the Kangaroo deal, particularly the longer tenor (see chart 1). The seven-year tranche also garnered strong support from asset managers (see chart 2).

Source: Air New Zealand 19 May 2022

Source: Air New Zealand 19 May 2022

“We received really good support from Australian and Asian investors, which provided early feedback to guide approach to market,” says Billy Sangha, director, debt capital markets at CBA in Sydney. “It was good to see the support for the Air New Zealand credit and the aviation sector following the COVID-19 disruption.”

The transaction drew 55 investors to a final orderbook of more than A$840 million after peaking at more than A$900 million. Initial price thoughts had the four- and seven-year tranches at 240-250 basis points and 300-310 basis points over semi-quarterly swap. Both priced at the tight point of the marketing range.

Mitchell says: “To get that response from the investor base, with a lot of high-quality investors engaged, is a tremendous result. The size and level of oversubscription for a debut borrower in the aviation sector is a very good outcome for the issuer.”

According to Peters, focused marketing and the deal’s dual-tranche structure helped attract investors, with good pricing outcomes flowing on from there. “We are very pleased to have got the deal done the way we did,” she says. “It was very smooth from our perspective and a great experience for the Australian market.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.