ASB US dollar tier-two attracts strong offshore interest

ASB Bank is the first New Zealand issuer to price an offshore tier-two deal under the Reserve Bank of New Zealand’s new bank-capital definitions. The US dollar transaction was popular with investors – about five times oversubscribed – and priced tighter than similar tier-two debt issued by Australia’s big-four banks.

ASB Bank’s US$600 million, 10-year non-call five-year tier-two deal priced on 9 June at 225 basis points over five-year US Treasuries. Barclays, Citigroup, Commonwealth Bank of Australia (CBA) and HSBC were joint leads.

Steve Lucas, general manager treasury at ASB in Auckland, tells KangaNews the bank’s latest deal builds on previous offshore issuance executed in US dollars and euros, particularly in 2021 (see table).

ASB Bank benchmark US dollar, euro issuance 2018-22 YTD

| Announced | Volume (million) | Tenor (years) | Format | Coupon |

|---|---|---|---|---|

| 7 June 18 | US$500 | 5 | Senior-unsecured | 3.75 |

| 7 June 18 | US$500 | 5 | Senior-unsecured | 2.65771 |

| 24 Sept 18 | €500 | 7 | Covered bond | 0.75 |

| 6 Mar 19 | €500 |

5 | Senior-unsecured | 0.75 |

| 16 May 19 | US$500 | 5 | Senior-unsecured | 3.125 |

| 16 Sept 19 | €500 | 10 | Senior-unsecured | 0.5 |

| 10 May 21 | €750 | 10 | Covered bond | 0.25 |

| 31 Aug 21 | €750 | 7 | Senior-unsecured | 0.25 |

| 18 Oct 21 | US$500 | 10 | Senior-unsecured | 2.375 |

| 18 Oct 21 | US$700 | 5 | Senior-unsecured | 1.625 |

| 6 June 22 | US$600 | 10NC5 | Tier-two | 5.284 |

Source: Commonwealth Bank of Australia 10 June 2022

“This deal represents about half of our tier-two funding requirement for the next 12-month period,” Lucas explains. “We would like two tier-two benchmark transactions outstanding in the market, so we will certainly consider further issuance this upcoming financial year.”

This is the first foreign currency tier-two deal since the Reserve Bank of New Zealand (RBNZ) implemented its capital adequacy framework in July 2021, which it finalised in December 2019. The framework raised the total capital requirement on the big-four banks to 18 per cent of risk-weighted assets – from 10.5 per cent. For all other banks it is 16 per cent. Only 2 per cent of the total capital ratio can be in tier-two format.

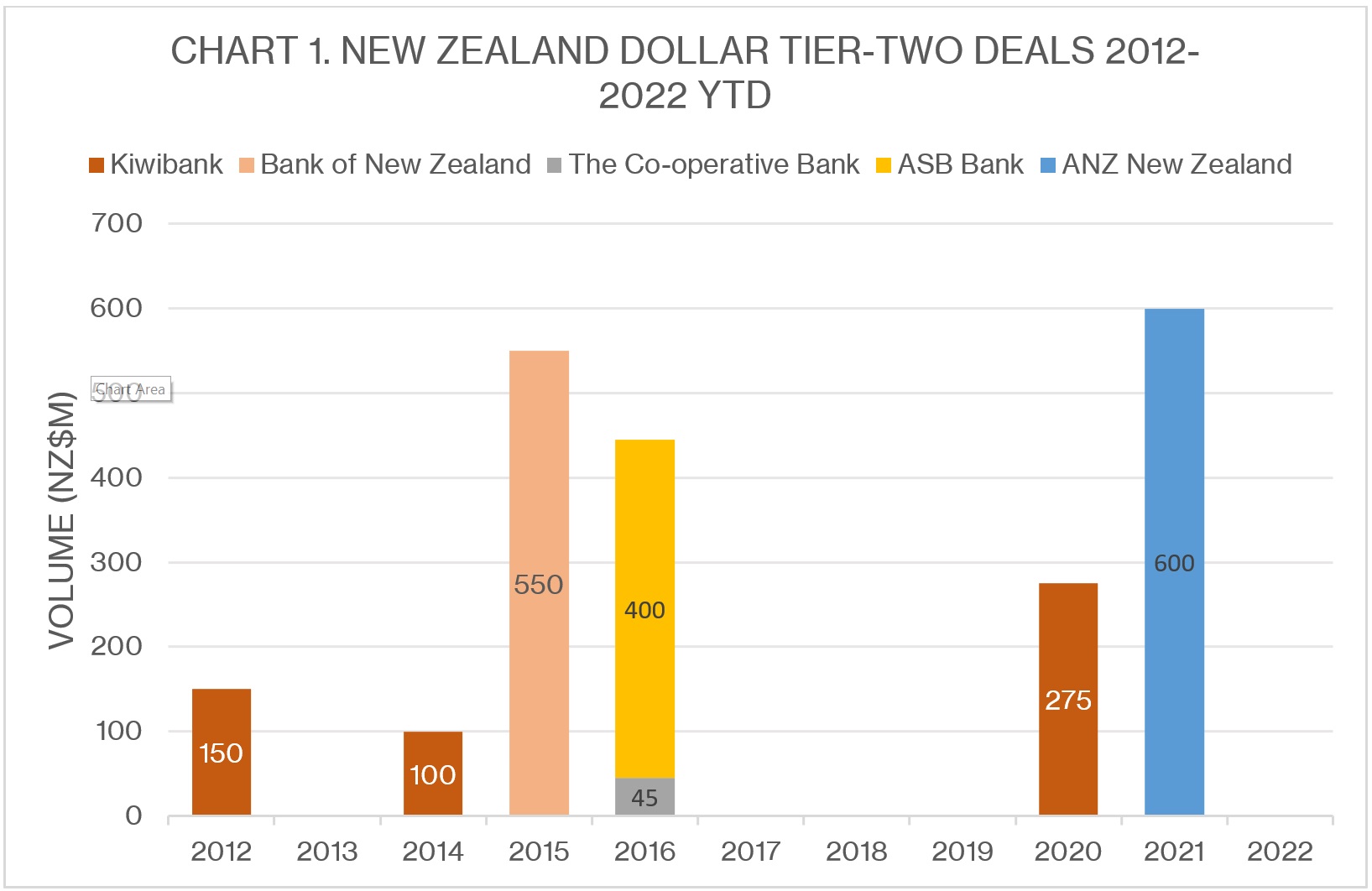

The capital requirements also changed the format of tier-two, stripping away the contractual non-viability clause – or loss-absorption triggers – found in typical tier-two deals in other jurisdictions, such as Australia. Only two New Zealand borrowers have issued domestic tier-two transactions since the capital requirements were finalised in 2019: Kiwibank in December 2020 and ANZ New Zealand in September 2021 (see chart 1).

Source: KangaNews 10 June 2022

Ollie Williams, managing director, head of debt capital markets – Australia and New Zealand at Citi in Sydney, says ASB’s inaugural transaction showed international investors endorsed New Zealand’s tier-two format. “It is also a strong signal to other New Zealand issuers that there is a deep and liquid pool of global US dollar demand for New Zealand bank subordinated capital product in the offshore markets,” he adds.

“Other New Zealand issuers will no doubt take comfort from the way this deal priced, which was essentially flat to the Australian major bank 10NC5 primary curve. It is a strong signal for other issuers, that may look to follow and use the US dollar 144A market to meet their tier-two funding requirements.”

The deal’s simple tier-two structure and higher credit rating engaged investors. At A-, ASB’s deal was rated one notch higher than typical Australian tier-two paper due to the RBNZ’s revised structure.

Lucas comments: “Investors have got comfortable over the past 10 years with Basel III features, such as the non-viability triggers, and there were questions on where the value of the trade sits with the absence of these mechanisms.”

He adds: “It is a great result for a debut New Zealand trade to be as close as it is to the Australian issuance curve. There is always price discovery when bringing new products to market, and there has been a lot of market volatility over the past three months. So we are very pleased with the take-up of this deal.”

DEAL DYNAMICS

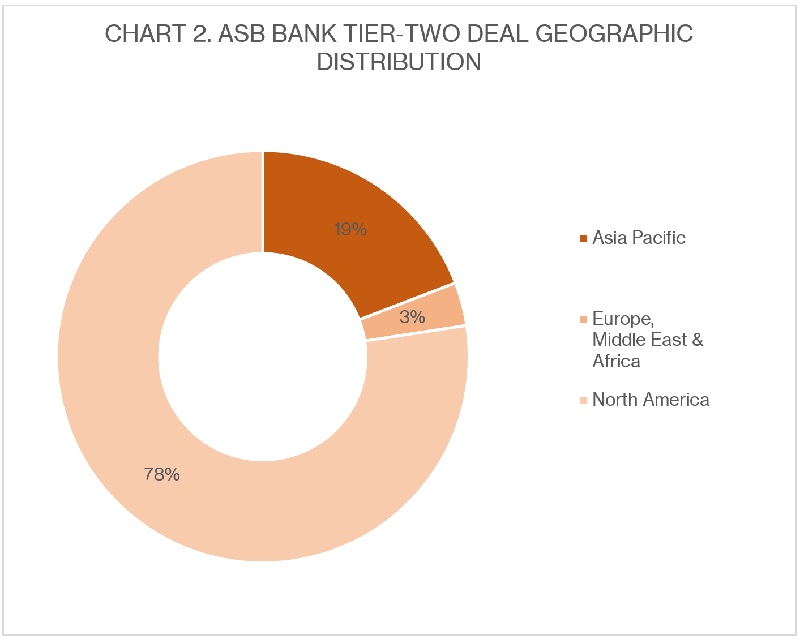

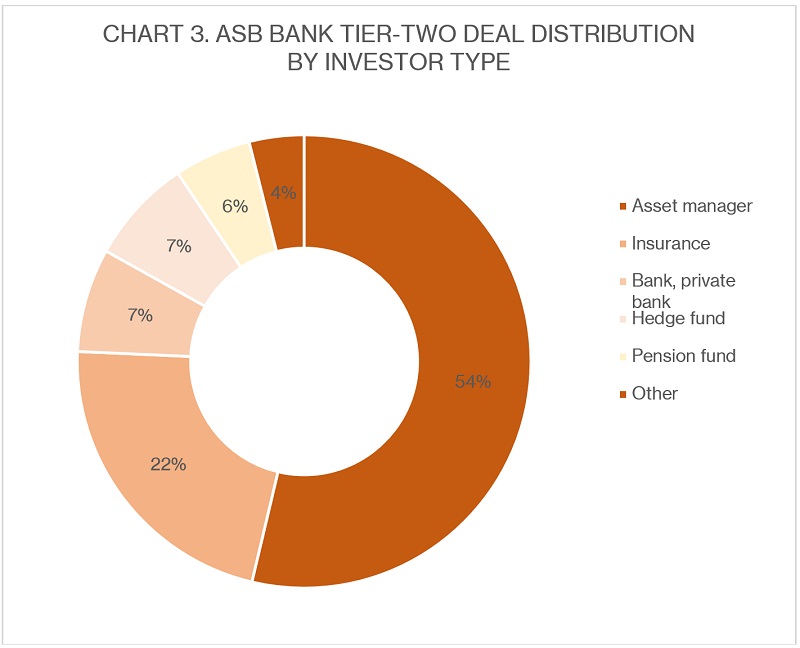

The final orderbook showed heavy distribution to North American investors, although Asian buyers bought nearly 20 per cent. Asset managers accounted for almost half of the deal (see charts 2 and 3).

Source: Barclays 9 June 2022

Source: Barclays 9 June 2022

Duncan Beattie, Sydney-based managing director at Barclays, says the scarcity value of tier-two ASB paper – particularly from an issuer with a strong international investor following – played into the deal’s success.

“New Zealand banks won’t issue anywhere near as frequently as the Australian majors. They just do not have the same size of tier-two needs,” he adds. “ASB is the first to access the offshore markets via tier-two. This is a new capital regime and this was the first offshore trade — and that makes it interesting.”

“New Zealand banks won’t issue anywhere near as frequently as the Australian majors. They just do not have the same size tier-two needs. ASB is the first to access the offshore markets via tier-two format. This is a new capital regime and this was the first offshore trade — that makes it interesting.”

James Holihan, head of Asian syndicate at CBA in Singapore, says Asian and US investors were familiar with the ASB credit due to past offshore issuance, so attention was focused on the structure. He notes that the shape of the yield curve lent itself to a five-year call structure.

“The structure suited the issuer – ASB has a limited amount of tier-two to issue, certainly less than the Australian major banks. The structure gives the bank an opportunity to refinance at an earlier date than a 10-year bullet transaction.”

Danny Keene, director debt capital markets at CBA in Auckland, adds that bullet structures in the US are more favourable. “However, given where five-year Treasuries are versus the 10-year, having that call makes a lot of sense.”