Funding diversity and sustainability top the agenda for SSAs

KangaNews surveyed supranational, sovereign and agency issuers in May-June 2022, marking the ninth year in which these entities have provided their views and outlook on global funding. The latest survey shows a resurgence in use of noncore markets – most notably the Australian dollar – and the ever-growing significance of sustainability labelled bonds.

Courtney Barrett Peters and Laurence Davison

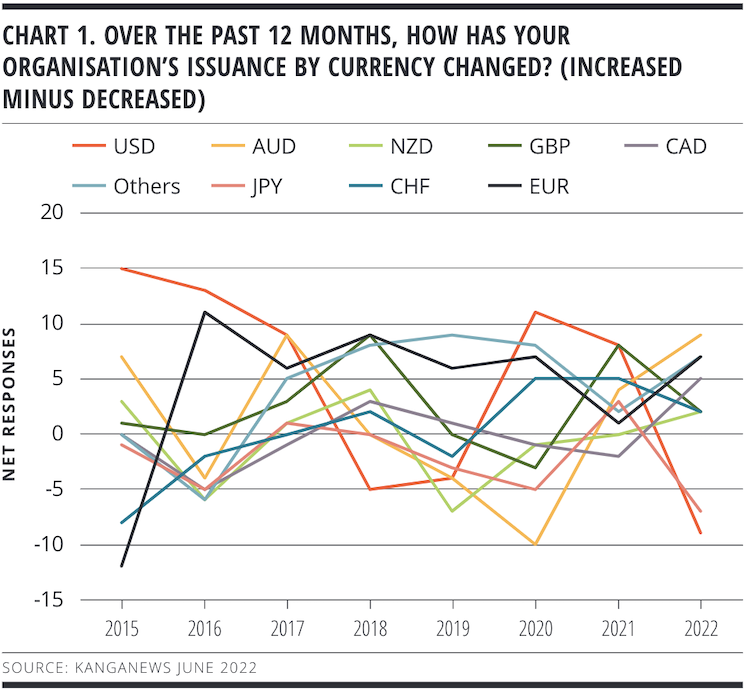

To some extent, the COVID-19 pandemic saw supranational, sovereign and agency (SSA) issuers increase their focus on core global markets – especially the US dollar. In 2020 and 2021, the net number of borrowers reporting increased US dollar issuance was higher than for any other currency. Other currencies have all suffered at times – most notably Australian dollars in 2020, which recorded one of the largest net negative issuance responses in the survey’s history.

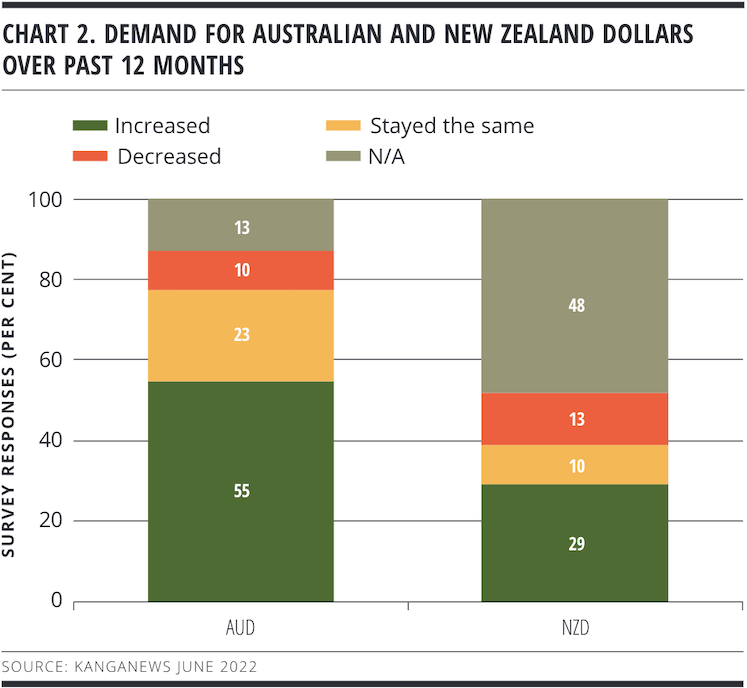

This year’s data show a resurgence in issuance of Australian dollars and euros in particular (see chart 1). A clear majority of SSAs report increased Australian dollar demand over the past 12 months, and a similar proportion have the same experience with New Zealand dollars once those that are not currently engaged with the currency are stripped out (see chart 2).

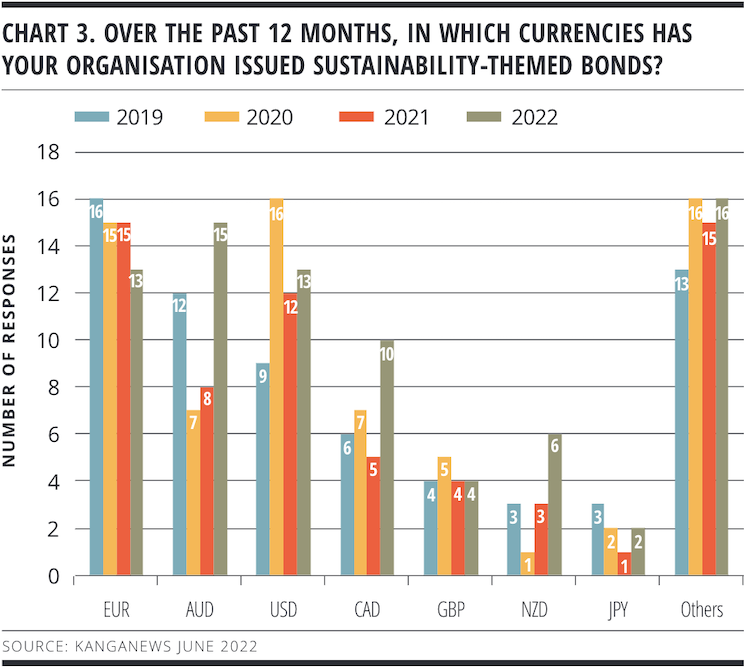

The Australian dollar has also been a fruitful venue for SSAs’ labelled green, social and sustainability (GSS) issuance, with 15 of the 30 borrowers that responded to the survey reporting activity in this format over the past 12 months – more than any other single currency, for the first time ever (see chart 3). The number of SSAs issuing New Zealand dollar GSS bonds also saw a significant jump.

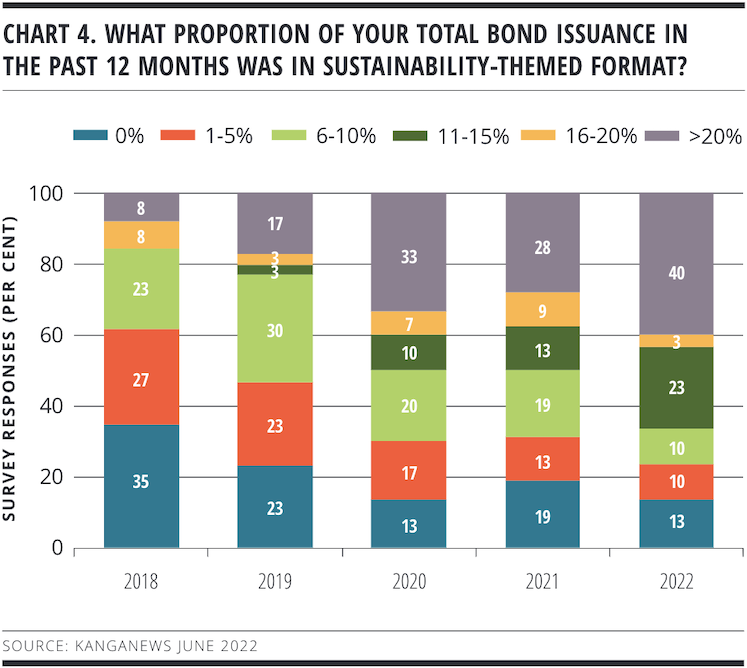

The survey demonstrates that the GSS format is certainly not losing its lustre for SSA borrowers. The proportion that reports raising more than 20 per cent of total funding via GSS is at its highest-ever level – 40 per cent – while the 13 per cent of survey respondents that have not issued GSS bonds in the past 12 months is the equal-lowest ever (see chart 4).

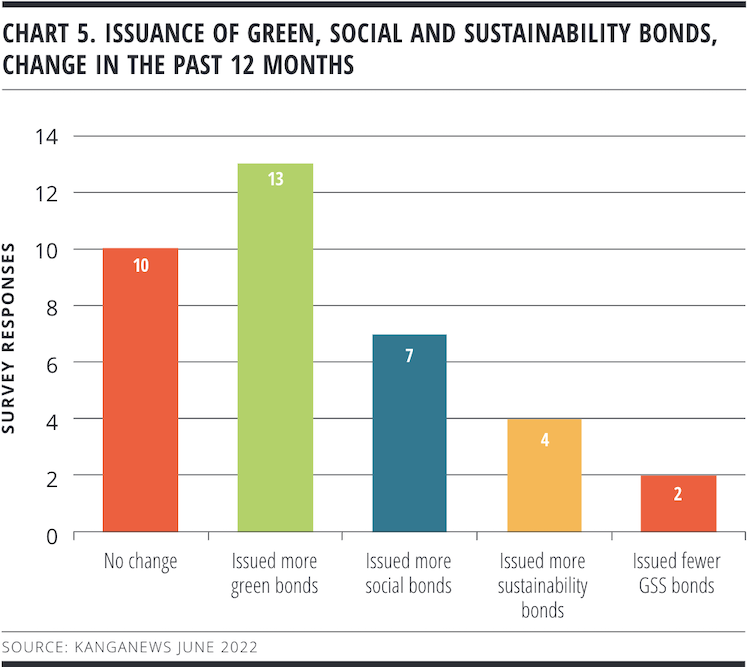

Green bonds continue to drive ongoing growth in environmental, social and governance (ESG)-labelled deals. A total of 13 SSAs say they increased this type of issuance in the past 12 months (see chart 5). A smaller group of SSAs also added to their social or sustainability bond supply.

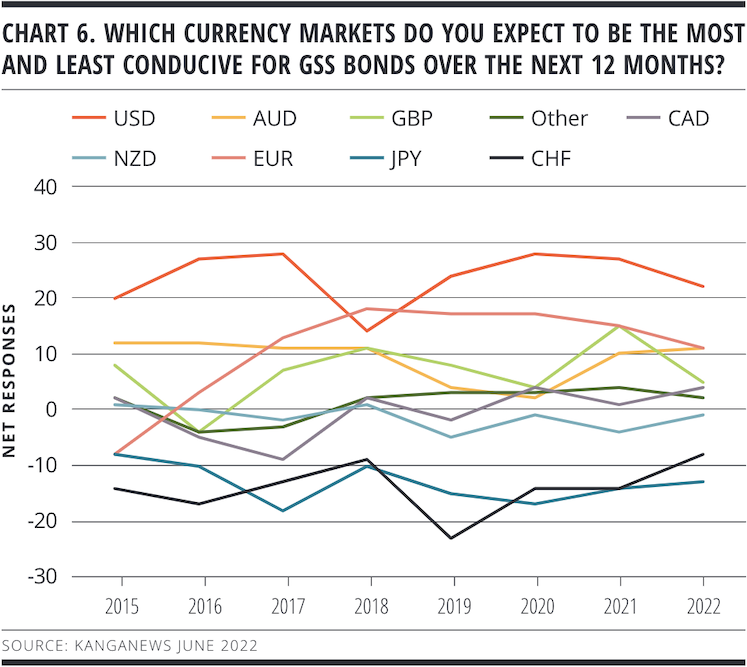

Regarding the outlook for GSS bonds, the move to enhance issuance currency diversity in 2021-22 does not appear to have an impact on issuers’ expectations. The US dollar retains its primacy as the currency with the highest net score for expected conduciveness for issuance over the coming year (see chart 6). Expectations on issuance currency are relatively consistent year on year, though in 2022 sterling declines to close to net zero from a generally optimistic outlook.

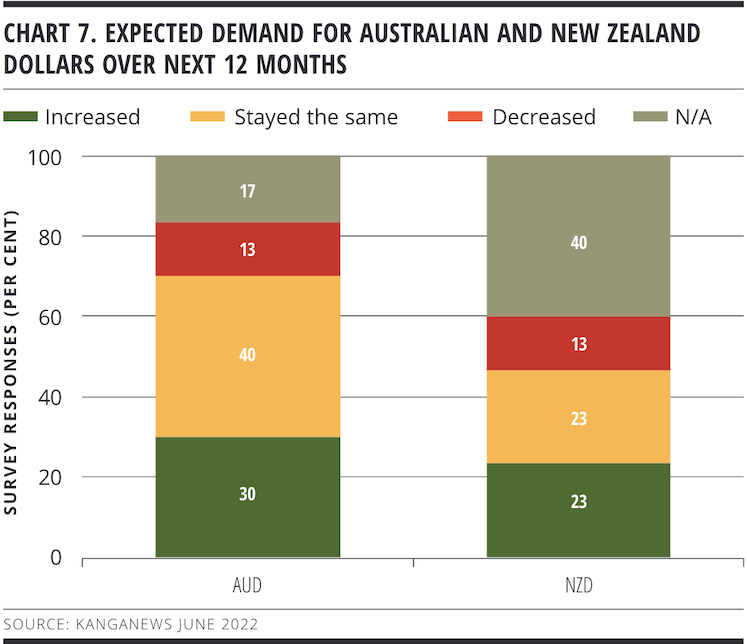

The outlook for Australasian currencies is broadly positive. Despite growth in the past 12 months, 30 per cent of survey respondents anticipate even more demand for Australian dollars in the year ahead and a further 40 per cent predict a stable year (see chart 7). The proportional response is similar or even marginally more positive for New Zealand dollars.

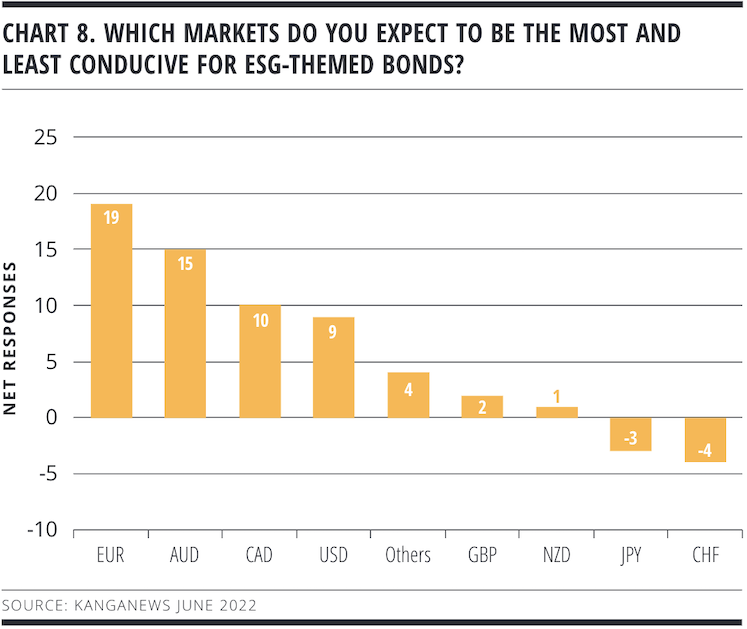

SSAs also expect the positive tone for Kangaroo GSS issuance to continue over the coming 12 months, with euros narrowly passing Australian dollars as the currency SSAs believe will be most conducive for GSS deal flow (see chart 8). The New Zealand dollar market is less favoured for GSS supply by SSAs, though this is just as likely to relate to its outright size – or that of other markets – as it is a comment on GSS labelled bond demand locally.

The survey’s issuance data highlights the value of GSS bonds to SSA issuers. And while sustainability-linked structures may be growing in relevance as a funding option for corporate credits, SSAs are if anything increasing their focus on use-of-proceeds securities.

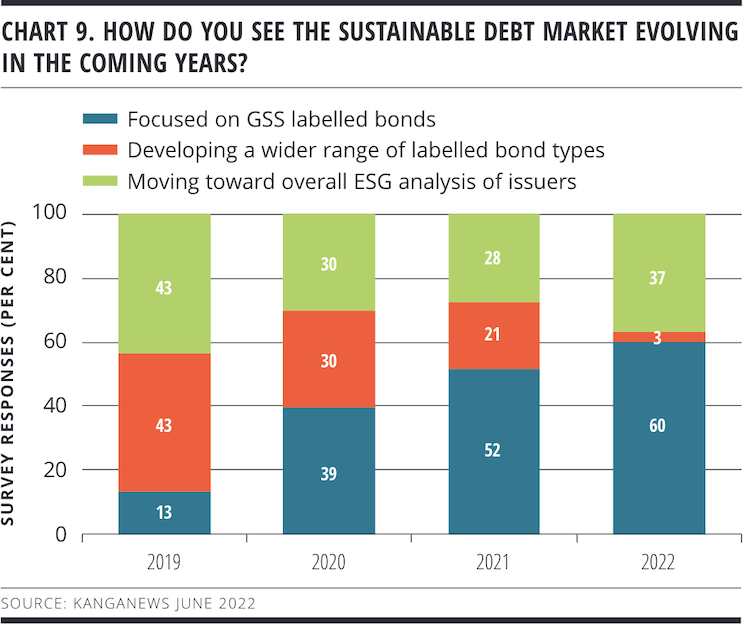

A record number of survey respondents – 60 per cent – predict the sustainable debt market in their sector will continue to focus on labelled GSS bonds in the coming years (see chart 9). While the number that expect the market to migrate to holistic, borrower-level analysis is also increasing, very few SSAs now forecast the development of a wider range of labelled bond types. The view seems to be that SSAs will either issue the instruments that are already available or move beyond labelled issuance entirely.

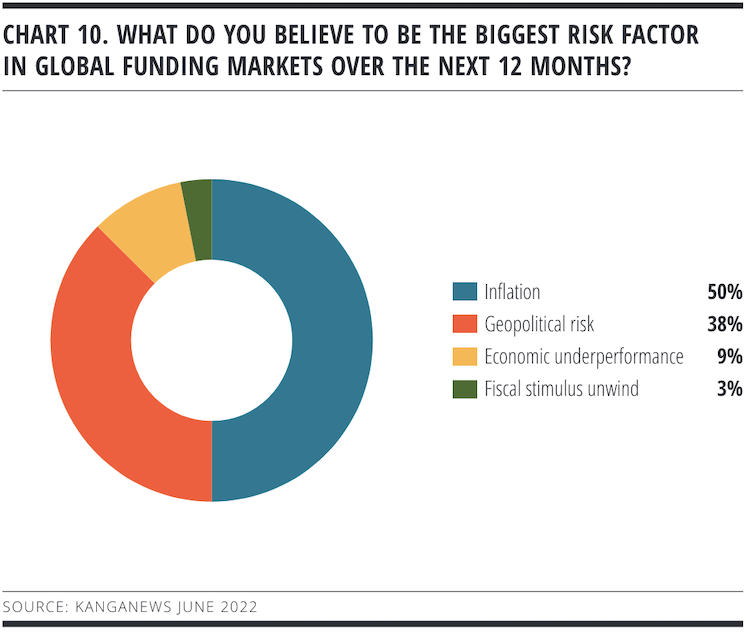

Also on the outlook, SSAs are focused on two primary risk factors for the year ahead: inflation and geopolitical tension (see chart 10). The former is not new, as more than 40 per cent of survey respondents highlighted inflation as the primary risk a year ago. Geopolitical risk, by contrast, barely featured in 2021.

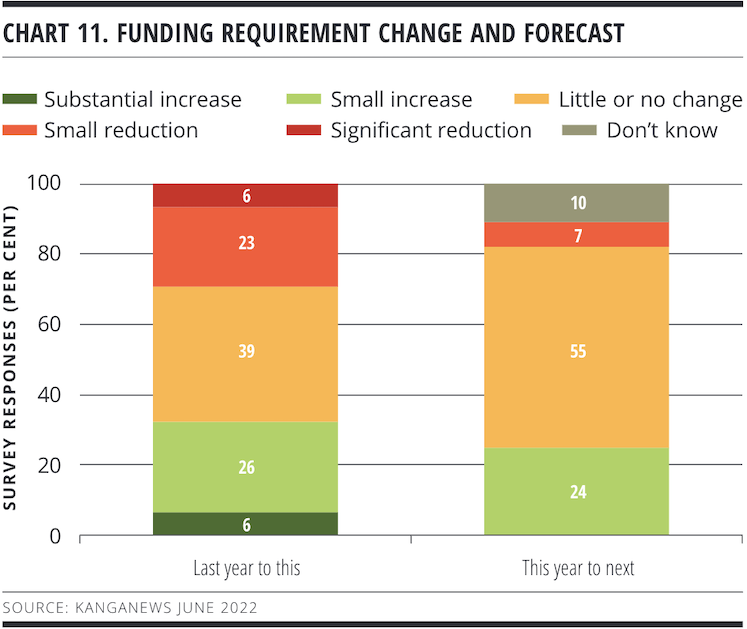

SSAs are at least facing an uncertain future with relatively stable funding tasks. More than half the survey respondents project little or no change to issuance requirements for the year ahead and none predict a significant change in either direction (see chart 11).

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

Quantum leap for Canadian provinces as Québec smashes Kangaroo record

Investor diversity, relative value and the growing status of the Australian dollar market lined up for Province of Québec as it shattered the record volume for a Canadian province Kangaroo transaction. The A$1.35 billion, 10-year print was nearly four times larger than any previous deal from the sector – a record that had stood for a decade.