Headwinds for SSAs down under but market position remains

After a very positive start to the new year in Australia, supranational, sovereign and agency Kangaroo issuance has dialled right back as the sector goes through a periodic revaluation of relative value and appeal to domestic and offshore investors. Assisted by their affinity with sustainability-labelled issuance, however, these issuers remain a core part of the market in Australia and New Zealand.

Lara Sonnenschein Staff writer KANGANEWS

The first and second quarters of 2022 demonstrate how supranational, sovereign and agency (SSA) issuance can run hot and cold in Australia and New Zealand. As the new year began, the Kangaroo market facilitated high issuance volume and diversity of supply.

The change in tone toward the end of the quarter, however, saw a significant retreat in demand for SSA paper in Australian dollars from domestic and offshore investors. Australian investors in particular report they are struggling to see value in SSA issuance in mid-2022, while second-order effects have also sparked a notable selldown from a key offshore jurisdiction.

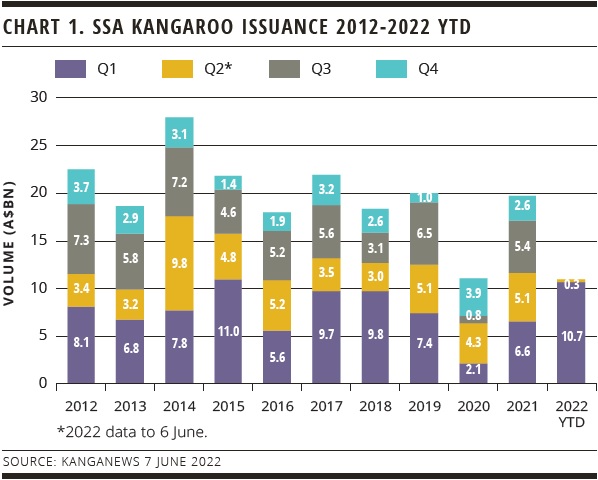

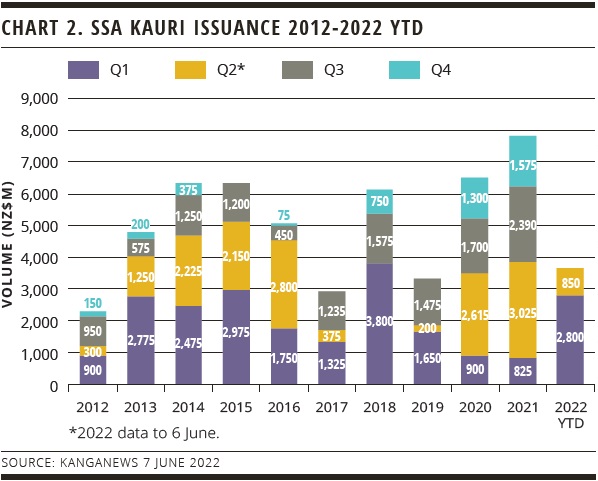

The change in sentiment is clearly reflected in issuance volume. After a near-record Q1 for SSA Kangaroo issuance, supply slowed to a trickle in the second quarter (see chart 1). The situation is similar in New Zealand, though a NZ$850 million (US$552.5 million) May print by Asian Development Bank somewhat masks the second quarter slowdown (see chart 2).

“While Japanese lifer demand for Kangaroo bonds has fallen in absolute terms, within the foreign bond allocation and on a relative basis Australian dollars still remains attractive on an FX-hedged basis.”

Button TextKBN and L-Bank. NWB Bank then priced a A$650 million deal on 24 February, hours before Russia began its invasion of Ukraine, which more than doubled its last Australian dollar deal volume.

“The first few weeks of 2022 were a cracker,” says Marayka Ward, director, liquid markets group at QIC in Brisbane. “I was thinking ‘this is going to be interesting’ – especially because there seemed to be a much broader range of investors involved. But it has fallen off a cliff since then.”

Global debt markets have clearly confronted challenging circumstances since late February, with the Russia-Ukraine war accelerating inflationary pressure and the tightening rate cycle. Bond yields have been on a rising trajectory while all asset classes have been subject to a surge in volatility.

This has not sparked concern about SSA credit, market sources say. But it has had two key negative impacts: starting a domino effect that led to a major sell-off from the Japanese investor sector, and bringing to the fore issues that have long made SSAs a less favoured asset class among the Australian investor base.

Even in more difficult circumstances, though, the SSA market has been able to demonstrate its role within Australian and New Zealand capital markets. Primary flow has been minimal in Australian dollars but other global investors have largely absorbed the sales from Japan. The New Zealand market, meanwhile, has started to offer new issuance opportunities once more.

THE JAPANESE SELLOFF

Japanese investors often represent the largest contingent in the SSA Kangaroo market. At times they have been the primary driver of issuance, including reshaping the primary market in favour of small, typically long-dated, tap issuance from the middle of the last decade.

Recent months have posed new challenges for the Japanese bid. In March, SSA bonds came under considerable pressure as an ongoing rally in Australian dollar-yen sparked significant selling out of Japan. SSA spreads widened by 15-25 basis points against Australian Commonwealth government bonds and local semigovernment securities, according to deal sources.

The selloff contributed to the drop in primary deal flow, notes Jim Malone, managing director, fixed income sales at TD Securities in Singapore. He says there has been plenty of interest in Australian dollars given funding arbitrage opportunities but demand has softened amid heightened market volatility.

While Japanese investors typically undertake considerable rebalancing around the beginning of their new financial year, in March, the 2022 season proved to be more turbulent than most. Market participants say currency rather than credit was the primary catalyst for Japanese pullback from the Kangaroo market.

A depreciating yen often causes Japanese accounts to take profit on foreign currency holdings. By mid-April, the Australian dollar hit ¥95 (US$0.73) for the first time since 2015. Japanese retail funds often have triggers to sell at or around this level.

Anthony Kirkham, head of Australian and New Zealand investment management and business operations at Western Asset Management in Melbourne, says yen depreciation due to the Bank of Japan stance on QE triggered outflows at the worst possible time for the market, taking out a chunk of liquidity just as credit and SSA supply saturated the market.

The Kangaroo market has dealt with an elevated Australian dollar in the past: the currency has spiked above ¥100 four times in the past decade and a half, and demand has always recovered when Japanese investors start to forecast a declining trend.

“The first few weeks of 2022 were a cracker. I was thinking ‘this is going to be interesting’ – especially because there seemed to be a much broader range of investors involved. But it has fallen off a cliff since then.”

Button TextJAPANESE DOMESTIC YIELD

There may be a more structural challenge, however. For the first time in decades, Japanese investors are experiencing a comparatively attractive domestic market with a curve that offers value for an investor base with a bias for long-dated issuance.

As Japanese government bond (JGB) yields rise so foreign currency allocations potentially become less necessary for local investors. Sources say many of the country’s major life insurers have recently released comprehensive plans to reduce offshore exposures in favour of buying super-long domestic debt.

For example, Nippon Life – Japan’s largest life insurer – plans to reduce foreign currency hedged assets and switch to corporate debt from government bonds within its foreign bond allocation, while it expects unhedged assets to be stable or decrease for the fiscal year ending March 2023.

On the other hand, even this negative trend in some ways emphasises the resilience of the SSA Kangaroo market. Malone says the bulk of the flow out of Japan has been recycled to other international investors, particularly central banks targeting the healthy pick-up versus government and semis and in bonds marked cheap versus US dollar equivalents.

Thomas Archer, London-based product specialist in the global fixed income investment team at Nikko Asset Management, trades Australian and New Zealand dollar denominated debt and is particularly optimistic about the future of SSA environmental, social, and governance (ESG) issuance.

Nikko restructured its global green bond portfolio in 2018 so it could buy more triple A-rated SSA issuance. The asset manager holds close to the global benchmark – around 5 per cent – in Australian dollars, but Archer says this could increase if there is more Kangaroo ESG issuance in future. SSA issuers responding to a KangaNews survey say they expect the Australian dollar to be second only to the euro in its conduciveness to ESG issuance in the year ahead (see box).

ESG driving SSA demand

Green, social and sustainability (GSS) issuance has become a mainstay of supranational, sovereign and agency (SSA) supply in Australia and New Zealand, where it enjoys notably enhanced engagement from domestic investors. Market participants say there is goodwill on both sides to help meet net-zero commitments, though investors are focused on product rigour.

SSAs had something of a head start in GSS issuance in the sense that they were among the first to print such deals globally as environmental and social good principles are their raison d’être.

World Bank printed Australasia’s first green bond in 2014. Momentum has only increased since then. Last year, SSA issuers provided almost half the total GSS supply in the Australian market, while in 2022 to 7 June this jumped to 65 per cent. “If an investor wants exposure to GSS bonds, it is difficult to achieve size and spread without holding SSAs,” explains Jim Malone, managing director, fixed income sales at TD Securities.

Indeed, with growing investor interest in environmental, social and governance (ESG), domestic investors that are typically less engaged with the SSA sector are often much more active in the same issuers’ GSS supply. Issuers have consistently noted greater domestic interest in their GSS offerings than vanilla Kangaroo or Kauri deals. Market users report European Investment Bank has effectively revitalised its Kangaroo issuance opportunities thanks to its focus on ESG-aligned issuance.

There is also no indication the Japanese bid is set to disappear entirely. In fact, in the 10-year part of the curve and on a relative basis, Australian dollar bonds offer among the highest foreign currency-hedged yields globally. “While Japanese lifer demand for Kangaroo bonds has fallen in absolute terms, within the foreign bond allocation and on a relative basis Australian dollars still remains attractive on an FX-hedged basis,” says Malone.

Japanese demand could also follow the domestic bid into stronger alignment with sustainability. “I can foresee a real push in ESG products in Japan in the next 3-5 years,” Archer tells KangaNews. “When this happens, there will be a significant change in global capital allocation to these projects and products because of the sheer size of the Japanese market. This is very exciting.”

AUSTRALASIAN CHALLENGES

ESG is the main area where Australian domestic demand and SSA issuance have been most likely to coincide (see box). The challenge for global SSAs in Australia is well known: their bonds are perceived as being less liquid than the local government sector but they do not offer yield that competes with what is on offer from domestic high-grade credit, particularly major-bank issuance.

Darren Langer, Sydney-based co-head of Australian fixed income at Yarra Capital Management, confirms: “We find that generally the single- or double-A credit market will give us a much bigger pickup with less trouble. We can get in and out of bank bonds and in and out of universities – this is high-grade credit that is generally much more attractive than SSAs.”

SSA spreads in mid-2022 are quite attractive on a historical basis versus Australian sovereign and semi-government bonds. But it is the recent uptick in major-bank covered-bond issuance that is most noteworthy, Malone says. He views this as a competitive headwind to similar-rated SSA supply, especially for domestic investors looking to maximise returns. “Indexed Australian investors always seek to maximise return over benchmark,” Malone explains. “SSAs face competitive headwinds from other well-priced issuance for those tracking the Composite Bond Index. However, for investors tracking more high-grade benchmarks – like central banks – or those targeting a high quality strategy, the sector offers good pick-up and good liquidity underpinned by a truly broad and global investor base.”

Defensive positioning is not helping, however – despite SSAs’ largely unimpeachable credit quality. Ward explains that even though SSA spreads are fairly attractive relative to local semi-governments, QIC views the domestic sector as the natural defensive asset class. However, she adds that SSA pricing could become compelling if it was slightly wider.

“We used to mark all our New Zealand bond holdings versus a risk-free government benchmark but we have shifted to the investment grade corporate bond index. SSAs had positive carry versus the government benchmark but they are much less likely to have this versus corporate credit.”

Button TextLanger is unconvinced. “There is still a lot of dynamic in the market to keep semi-government spreads a little tighter than there is additional demand in the SSA market,” he says. “Some of this comes from changes to the CLF [committed liquidity facility], but it is also significant that we do not know what is in store for Japanese investors over the next 6-12 months.”

It is a similar story in New Zealand. Iain Cox, Auckland-based Australasian head of fixed income and cash at ANZ Investments, says his firm’s interest in the SSA market has waned to some extent. “We used to mark all our New Zealand bond holdings versus a risk-free government benchmark but we have shifted to the investment grade corporate bond index. This allowed us to buy triple-B credits – something we had not previously done – in a low-yielding environment,” Cox explains. “SSAs had positive carry versus the government benchmark but they are much less likely to have this versus corporate credit.”

If relative value and thus demand start to return, they will likely emerge in the short end. Malone says Australian dollar SSAs are trading cheap to US dollar equivalents in the front end before losing value at 5-7 years. “Domestic credit curves are far steeper than the SSA curve,” he notes. “Investors are getting more compensation further out the curve by investing in familiar names and wider-spread products such as covered bonds and major-bank senior-unsecured.”

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

Quantum leap for Canadian provinces as Québec smashes Kangaroo record

Investor diversity, relative value and the growing status of the Australian dollar market lined up for Province of Québec as it shattered the record volume for a Canadian province Kangaroo transaction. The A$1.35 billion, 10-year print was nearly four times larger than any previous deal from the sector – a record that had stood for a decade.