Corporate bond issuance set to spark

Corporate borrowers have leaned on bank loans in 2022, as volatility and rising cost of funds in fixed income markets have made public bond issuance less attractive. The situation will not last indefinitely, however – indeed, corporate issuers may be forced back into funding markets in H2.

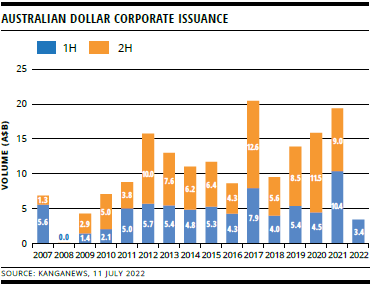

Australian corporate bond issuance stalled in the first half of 2022, falling to levels not seen since the immediate wake of the financial crisis (see chart). Although volatility contributed to lower issuance, 2021 had also been a bumper year for primary deals, meaning corporate Australia’s funding needs were largely met.

As the cost of funding in public bonds rose this year corporates sought cheaper pricing in bank loan markets, Ian Campbell, Sydney-based managing director, debt capital markets at Citi, tells KangaNews.

“One-month BBSW sat on average at 8-12 basis points for a long time; it is now at about 146 basis points,” Campbell says. “For floating-rate funders, the cheap issuance that was available over the last few years has completely and utterly disappeared in an instant.”

The three-month BBSW rate has also increased significantly, climbing to 196 basis points in July 2022 from 3 basis points 12 months ago.

Campbell says corporate borrowers with incoming quarterly rolls are experiencing sharp increases in their coupons across loans and bonds due to the rise in BBSW.

“Corporate borrowers’ repayments have risen sharply and duration has also come in very dramatically,” he says. “Investors do not want or need 10-year exposures – they can do five- and seven-year and get a fantastic return and lower duration risk, or they can simply buy one-year US Treasuries at 3 per cent and sit the volatility out.”

While the bond market may be looking good for investors from an all-in yield perspective, Campbell says corporates have turned to the slower-moving bank loan market to achieve their funding goals. Bank loan margins typically lag the public bond market. They take longer to execute and the terms of the loan are locked in earlier. The impact on banks’ net interest margin is the most likely factor to affect the price of a loan.

Campbell says borrowers have been rewarded for moving quickly. “Issuers need to be nimble and they must have their documentation up to date because the opportunity windows are much narrower than they were,” he says.

“We have seen more ‘no issuance’ days this year than in the past two years combined. Over the past few years, waiting has been a good strategy as spreads have continued to narrow, so issuers have been paid to sit out. We are seeing the complete reverse now. When the window is there, issuers should take it.”

Patrick Liddy, sales lead, Australia and New Zealand at SS&C Intralinks in Sydney, says deal participants should be agile given rising rates, inflation and geopolitical uncertainty, which are causing weak primary debt volumes globally.

SS&C Intralinks facilitates deal execution by providing virtual data room (VDR) technology via its VDRPro platform. The company has supported more than US$34 trillion equivalent of sensitive, high-value transactions across debt and equity markets globally over the past 24 years.

Liddy says issuers accelerated their debt issuance in Q1 ahead of rate increases. “Deals are not being abandoned – instead many are on hold or transaction timelines are prolonged,” he tells KangaNews. “Issuers should be mindful of elevated cybercrime and protect deal information as transaction timelines fluctuate. They need to ensure the technologies that facilitate their deals feature multiple layers of security, including encryption, multifactor authentication, data privacy certification and more.”

“With higher borrowing costs, corporates are less likely to opt for new financing. Green bonds might be somewhat more resilient to adverse economic conditions.”

Button TextFORCED ISSUANCE

Michael Momdjian, general manager, treasury, tax and insurance at Sydney Airport, says markets are highly volatile and corporates have good reason to sit on the sidelines.

This may not be an option for every corporate borrower, however. “Corporates that have not created flexibility by maintaining prudent levels of liquidity may be forced to issue in volatile markets,” Momdjian notes.

Sydney Airport has about A$4.8 billion (US$3.3 billion) of available liquidity – a substantial buffer that means it may not need to issue for several years. Other borrowers may only have several months of available funding.

“Being forced into the bond markets as a price taker with no flexibility is never a good thing,” says Momdjian, who points out that although loans can be a cheap source of short-term funding they are better suited as a stop gap in between long-term bond issuance.

Despite current pricing heavily favouring shorter-dated loans, Mondjian says Sydney Airport remains focused on spreading, lengthening and diversifying its debt maturity profile through bond issuance, Momdjian adds.

He explains: “We establish loans to fund near-term investment before terming. While loans provide flexibility in covering near-term debt maturities, if bond markets are not conducive to issuance we do not rely on these typically shorter-dated instruments to refinance maturing longer-dated debt, or simply favour them because of their relatively cheaper price.”

Momdjian believes bond issuance will pick up in H2. “While loans provide a competitively priced bridge into bond markets during volatile times, bond deals are getting done with strong oversubscription – albeit at high new-issue concessions. Issuers forced into bond markets during the second half may not fare so well, with investors increasingly selective and a number of high-quality names waiting for the right window.”

“While loans provide a competitively priced bridge into bond markets during volatile times, bond deals are getting done with strong oversubscription – albeit at high new-issue concessions. Issuers forced into bond markets during the second half may not fare so well.”

Button TextTHE GREEN-BOND ALTERNATIVE

Semi-government and financial issuers are considering other formats, including floating-rate notes and covered bonds, to help smooth execution and entice skittish investors. Corporate borrowers, by contrast, typically have a smaller range of instruments to choose from. In this context, green bonds could be an attractive option to help add execution certainty to transactions that print during periods of heightened volatility, according to Liddy.

“With higher borrowing costs, corporates are less likely to opt for new financing,” he explains. “However, green bonds might be somewhat more resilient to adverse economic conditions as the latest IPCC [Intergovernmental Panel on Climate Change] report and the Russian invasion of Ukraine highlight the need to move away from a fossil fuel-based economy.”

Liddy says green-bond issuers may enjoy lower cost of capital, tax benefits and attract strong investor demand. This continues to make them a more attractive financing option.

SS&C Intralinks’ VDRPro provides due diligence, collaboration and reporting solutions for issuers and deal teams engaged in the green-bond market. The platform features document sharing workflow, granular permissioning, security tools, deep insights and analytics.

Liddy says issuers and deal teams can use VDRPro to prepare deals by centralising, staging and structuring documents and folders. The platform can facilitate the bookbuild process, he says, by sending pre-sale documents and prospectuses, offering memos, and tracking and gauging investor engagement. The technology also streamlines the bond reporting process by giving bondholders secure access to performance, company financials and compliance information.

“Green-bond issuance can involve a massive amount of documentation with sensitive information that needs to be shared across internal and external channels with multiple collaborators and stakeholders,” Liddy says. “Issuers and deal teams need to work quickly and share documents efficiently. Sensitive information should only be available to those who really need to see it.”

Related news

Vicinity’s domestic print shows ongoing appetite for real estate

Vicinity Centres’ Australian dollar return provides another example of investor support for a wider range of corporate sectors – in this case, an oversubscribed book coming in for an issuer in the retail real estate sector as it seeks to move on from the pains of the pandemic. The issuer says domestic market conditions proved attractive for pricing and tenor.

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.