Tier-two activity points to emerging stability but challenges remain

More constructive new-issuance conditions persuaded ANZ Banking Group, National Australia Bank and Westpac Banking Corporation to return to tier-two issuance in late July and early August. Deal margins show a stark repricing over recent months but the issuers say demand was there for their domestic and US dollar prints.

Kathryn Lee Staff Writer KANGANEWS

National Australia Bank (NAB) got the ball rolling on 26 July, with a A$1.25 billion (US$887.9 million) 10-year non-call five (10NC5) deal. ANZ Banking Group priced A$1.75 billion with the same maturity profile on 3 August and Westpac Banking Corporation followed with a US$1 billion 11NC10 tier-two later the same day.

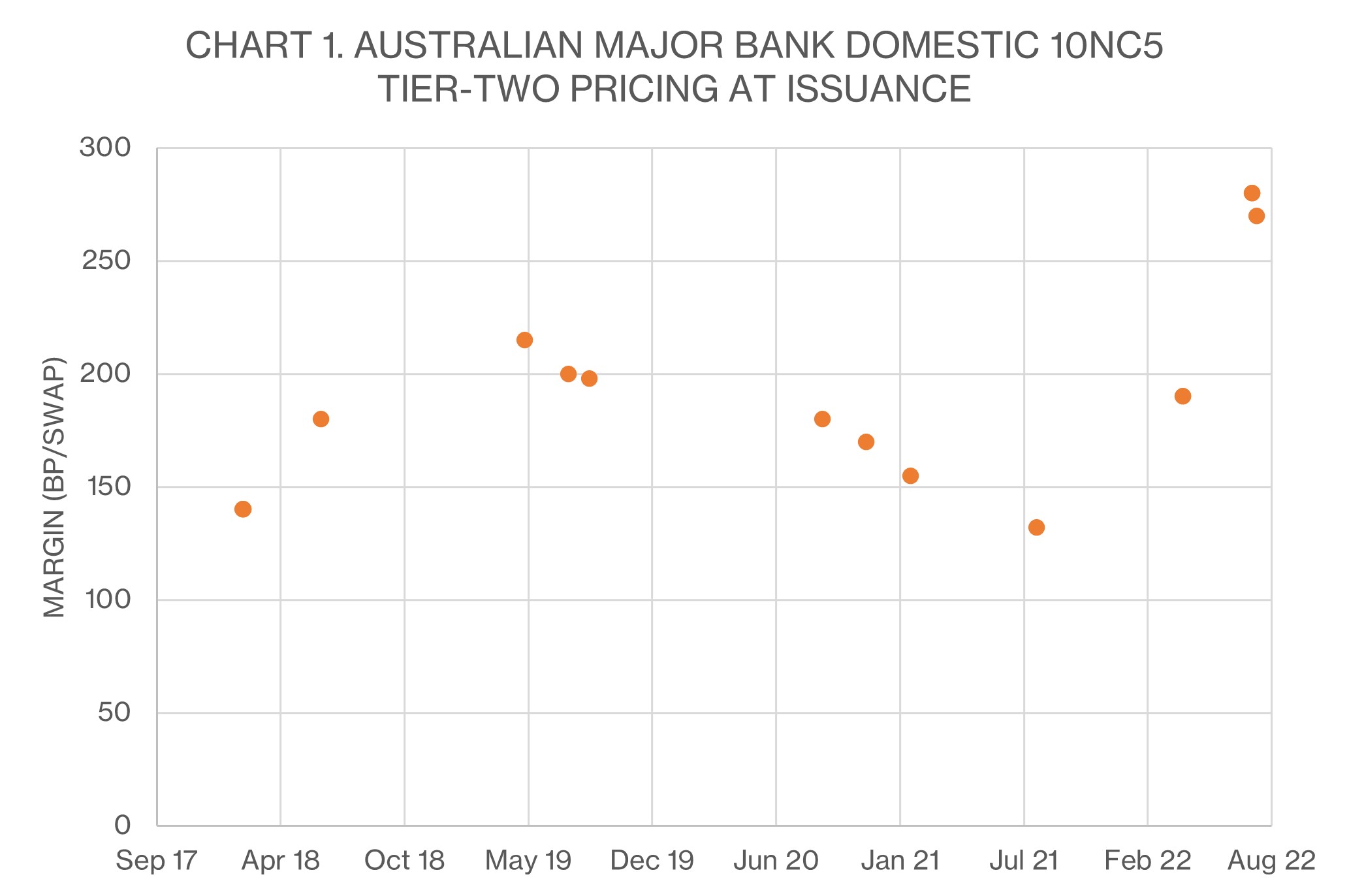

As the first major bank tier-two transaction since April, Michael Johnson, Melbourne-based executive, funding and liquidity at NAB, says some price discovery was needed for NAB’s return. The final transaction’s margin demonstrates the impact of market turbulence in recent months. The deal printed at 280 basis points over swap benchmarks, 90 basis points wider than a Commonwealth Bank of Australia print in April (see chart 1).

Johnson says the deal priced at an attractive level compared with benchmark tier-two pricing offshore. “This was a key factor in our decision to move forward,” he comments. “We have an ongoing funding task, specifically additional loss-absorbing capacity requirements. From a relative value perspective, this transaction made sense compared with alternative forms of funding.”

NAB’s trade is part of A$3-4 billion of tier-two issuance the bank expects to complete in the current financial year, Johnson explains. At its half-year results in March, NAB announced it had printed A$2.1 billion to March this year so it has now reached its issuance range for the product.

Simon Reid, ANZ’s Melbourne-based director, group funding, says the bank was confident conditions were ripe for its first domestic tier-two issue since August 2020. NAB’s trade “left a comfortable amount on the table” and was showing strong secondary market performance. “We also had some solid reverse enquiries,” Reid adds.

Based on these markers, ANZ readied itself to mandate the deal shortly after the Reserve Bank of Australia (RBA)’s August monetary policy decision. “We wanted a stable market reaction – if the RBA had surprised the market with a 75-basis point hike we would not have announced the trade,” Reid tells KangaNews.

ANZ’s pending acquisition of Suncorp’s banking business also played a role, specifically that ANZ was not able to issue subordinated debt ahead of the 18 July publication of its ASX cleansing notice while it considered the Suncorp acquisition.

ANZ has a tier-two funding task of around A$5 billion per year. Reid says this will be reassessed in the bank’s November results announcement but could grow depending on how it decides to incorporate Suncorp.

To meet its tier-two requirement, Reid says ANZ will pursue as many markets as possible. “We are very happy with the investor support we have received for deals across US and Australian dollars, euros and sterling. But over time we also hope to issue in yen, and Singapore and Canadian dollar markets as well as anywhere else we may be able to find receptive investors,” he comments.

“FRNs have been the benchmark tranche of Australian bank credit for a long period. It seems that the FRN remains dominant in shorter-dated senior debt, but elsewhere [the move to fixed] is a really significant change for the market and appears to be a broad shift.”

Button TextMARGIN HIT

The ANZ tier-two priced at 270 basis points over swap benchmarks – having launched with price guidance flat to NAB’s final margin. Secondary-market commentary suggests the NAB deal had tightened by roughly the same amount, with the fixed-rate notes performing particularly well.

“We hoped to move pricing tighter as we saw the book grow,” says Reid. “We were fortunate to receive great support from our investor base and this allowed us to comfortably price our equal largest Australian dollar tier-two deal.”

Westpac also reports good interest for its tier-two trade. The US$1 billion deal priced at 268 basis points over US Treasuries – equivalent to 308 basis points over BBSW, according to a Westpac Institutional Bank research note – and the orderbook peaked at US$3.9 billion.

Alex Bischoff, managing director, balance sheet, liquidity and funding at Westpac in Sydney, says the deal was a targeted transaction to complete its FY22 funding task. At 11NC10, it is longer-dated than NAB and ANZ’s tier-two prints. “It keeps us ahead of run rate and puts us in a good position heading into 2023 as well as for APRA [Australian Prudential Regulatory Authority]’s minimum requirements in 2024,” adds Bischoff.

The extra margin was worth paying given this context, Bischoff continues. “Domestic pricing looked good for 10NC5 but we are getting almost four years of extra capital for this deal, which is important when we still see risks on the horizon from the global economic backdrop. Recent stronger liquidity supported the decision to move ahead with tier-two in an offshore market.”

Bischoff adds that there was no temptation to increase volume in response to demand, however. “We had a capped volume of US$1 billion and we were never going to take more, even though more was certainly available,” he says. “This is very different from our approach over the last few years. This deal was much more targeted and a smaller volume.”

All three recent tier-two deals from Australian major banks point to a need to issue in this format even at notably wider margins. The driver is clearly the need to build a total loss absorbing capacity (TLAC) capital buffer.

“Australian banks need to have a significantly higher proportion of tier-two in their funding mix going forward,” Bischoff confirms. “We are therefore taking a through-the-cycle view [on issuance]. Our latest deal printed considerably wider than our tier-two print from November last year, but importantly keeps us ahead of our run rate and means we won’t need to catch up if markets deteriorate.”

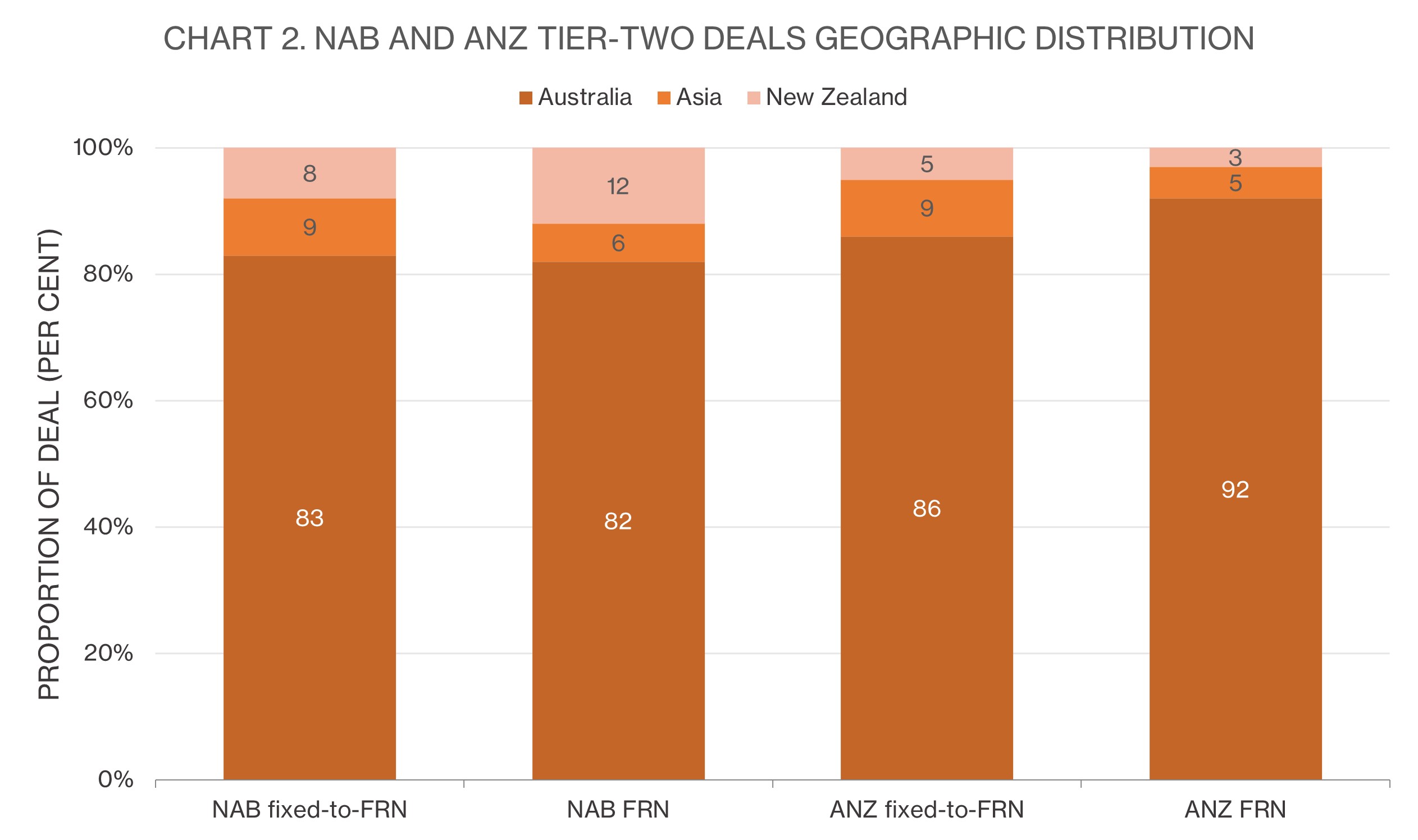

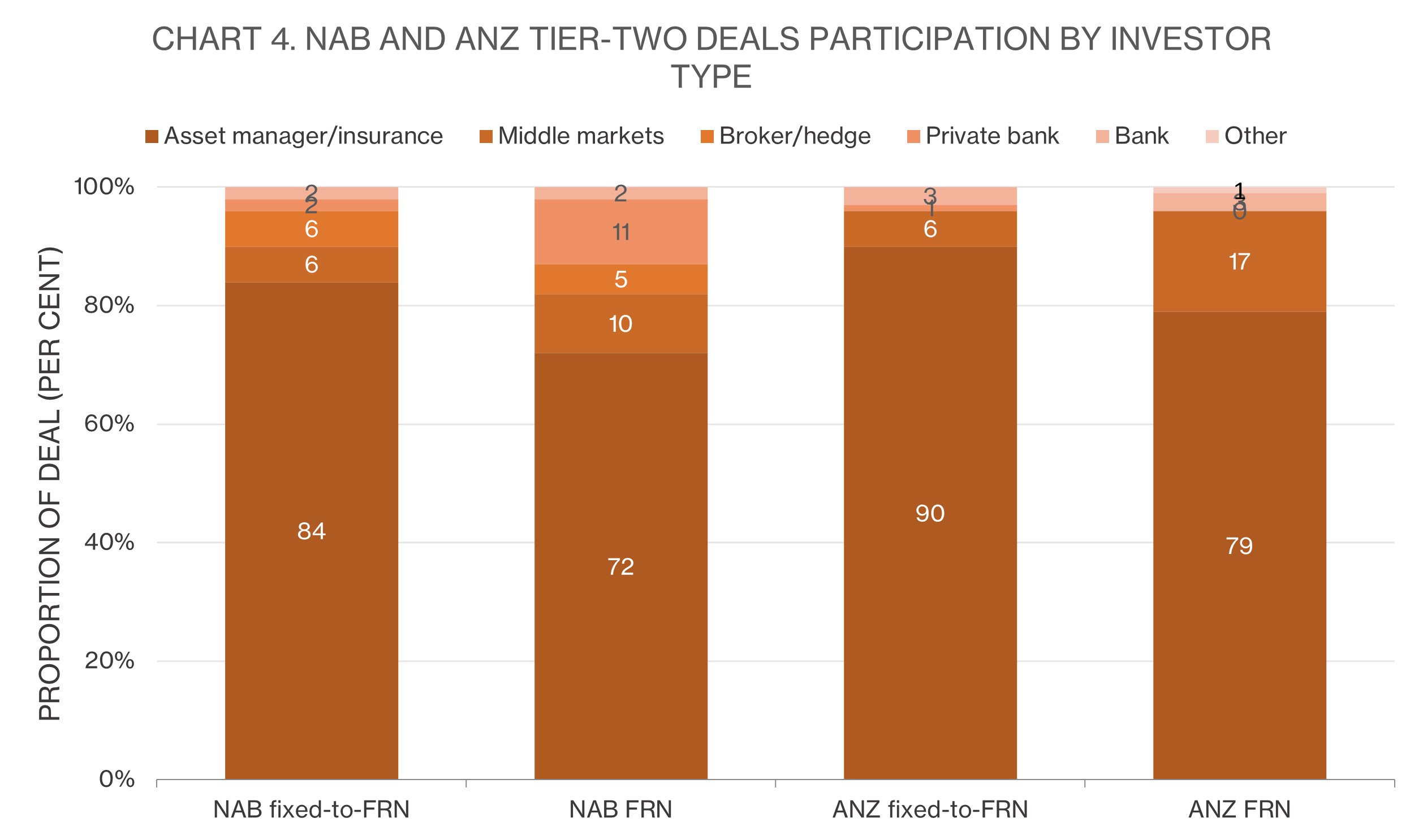

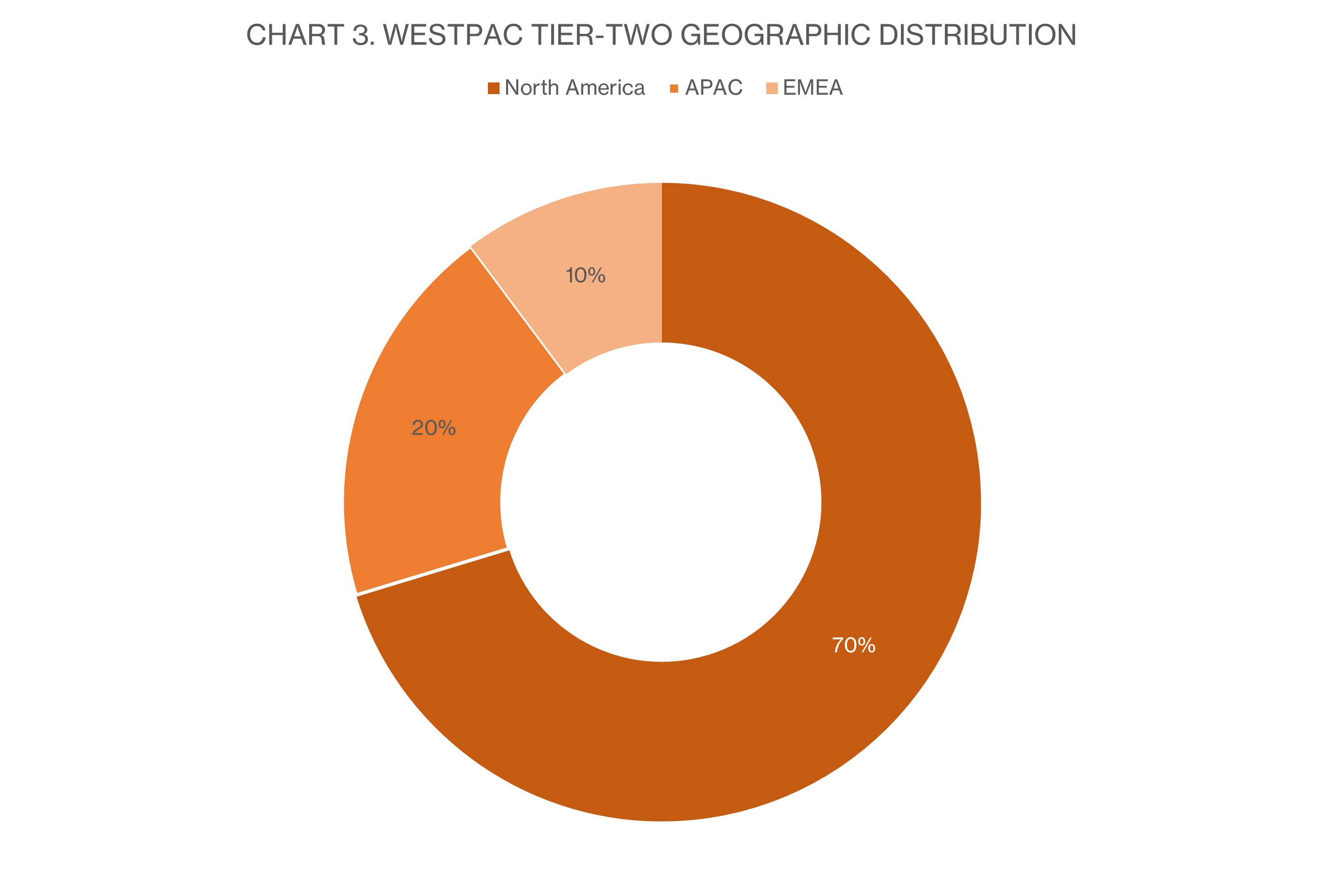

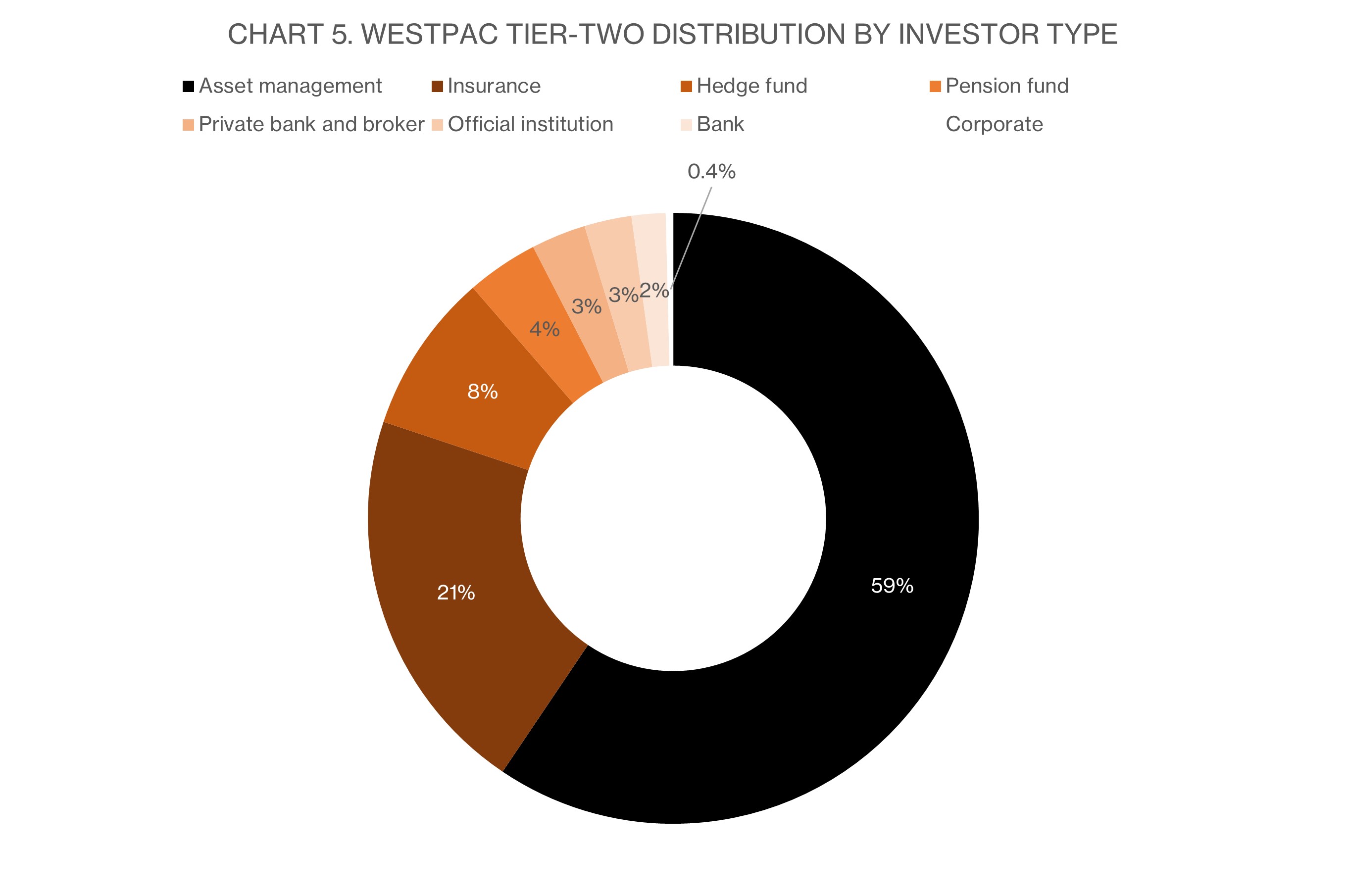

All three tier-two transactions attracted primarily local demand, though Westpac’s US dollar trade had an almost 20 per cent share from APAC investors (see charts 2 and 3). Asset managers and insurance were the most common investor type in all the transactions (see charts 4 and 5).

FIXED BIAS CONTINUES

The latest deal flow continues to demonstrate significant investor preference for fixed-rate notes. Johnson tells KangaNews NAB’s high proportion of fixed-rate notes – A$1 billion or four-fifths of total deal volume – catered to investor preference. Fixed-rate tranches from recent transactions in tier-two and senior format have been clear outperformers, which Johnson says combined with the outcome of a Macquarie Bank tier-two priced in June and CBA’s earlier print to give the NAB deal team confidence this is where demand would be found.

“Investors are attracted to the yield – of more than 6 per cent – on offer,” Johnson says. “Plenty of interest accompanied the deal and it was twice oversubscribed. This was pleasing given the challenging backdrop.”

ANZ received almost A$3 billion of total bids for its tier-two, of which roughly five-sixths was for the fixed-rate tranche. Reid says the issuer revised the composition of the deal to include a greater fixed-rate component in response to the demand skew, eventually printing A$1.45 billion of fixed-rate bonds and A$300 million of FRNs.

This is a notable change for the market, says Reid – though he also notes that a Westpac domestic three-year senior deal priced on 4 August was FRN dominant. “FRNs have been the benchmark tranche of Australian bank credit for a long period,” Reid says. “It seems that the FRN remains dominant in shorter-dated senior debt, but elsewhere [the move to fixed] is a really significant change for the market and appears to be a broad shift.”

Reid adds that the higher-yield environment is an obvious driver as it has supported interest from traditional fixed-rate buyers and accounts that usually buy FRNs. However, he is hesitant to say yield is the whole story.

He explains: “Perhaps some investors have a view that we will see rate cuts due to recessionary concerns at some point in 2023, which would explain why they see these higher yields as good value. But to me this does not fully explain the huge shift to fixed from floating. Perhaps more investors have fixed-rate mandates than in the past? It is difficult to make sense of the 180 degree turn.”

Jocelyn Wong, Sydney-based director, debt syndicate at ANZ, suggests it could also be to do with the development of the domestic major-bank tier-two market – specifically how the investor community is adapting.

“When APRA made its [TLAC] announcement there were a lot of reservations regarding the potentially significant tier-two supply from the major banks,” she explains. “However, the majors have shown in the last few years that the supply is manageable across various markets, while the recent issuance activity is a testament that the Australian dollar market has also grown.”

Wong tells KangaNews the size of ANZ’s orderbook demonstrates the level of liquidity available in the market in general, particularly in the tier-two space. She suggests growing demand for fixed-rate product is because the majority of the demand is from asset managers and insurance accounts, as bank balance sheets traditionally buy in FRN format.

“Investors are attracted to the yield – of more than 6 per cent – on offer. Plenty of interest accompanied the deal and it was twice oversubscribed. This was pleasing given the challenging backdrop.”

Button Text

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news