New Zealand securitisation takes a breather

After many years of promise, New Zealand securitisation broke through in 2021 with an unprecedented volume of public issuance – all from nonbank names. The turmoil of 2022 has put paid to any hopes for further momentum. But market users say local lenders have been able to manage liquidity and anticipate better times ahead once the dust settles.

Jeremy Chunn Editorial Consultant KANGANEWS

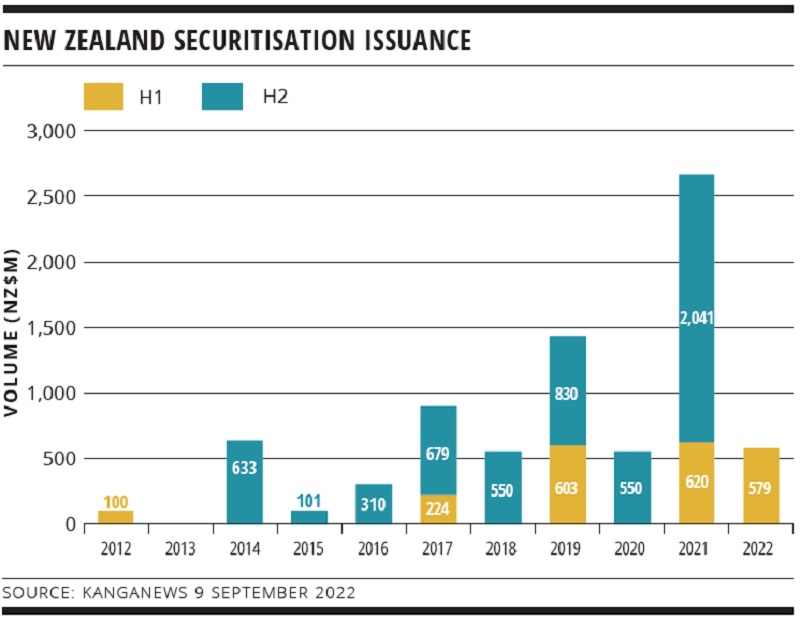

Securitisation deals in New Zealand have not quite ground to a halt, but the handbrake is engaged. A solid start to the year saw NZ$579 million (US$352.5 million) priced in the first half – only marginally short of the 2021 equivalent (see chart). But just NZ$295 million was added to the total in July and August, and market users have little expectation of the full-year total from 2022 matching the NZ$2.7 billion printed last year.

The backdrop to the slowdown is rising rates driving volatility – and investor hesitancy – in all credit asset classes. The New Zealand securitisation market has not had long to put down roots, so market participants say it is no surprise momentum has stalled.

New Zealand has also been at the tip of the spear of global policy reversion. The Reserve Bank of New Zealand (RBNZ) moved early to stanch inflation, with a tentative 25 basis point lift in October last year preceding a run of larger increases to the official cash rate (OCR). The RBNZ implemented another 50 basis point hike at its August meeting, bringing the OCR to 3 per cent. By contrast, the Reserve Bank of Australia did not begin hiking until May 2022 and its cash rate was 65 basis points lower than New Zealand’s by September.

The signs of a market slowdown appeared early. Bluestone Group priced New Zealand’s first new securitisation deal in the year in mid-March, and while the issuer was pleased with the NZ$280 million outcome it acknowledged that investor interest had narrowed. “We had already embarked on the transaction when market conditions changed, but we were fortunate in that we had strong support from existing investors and had not locked down a structure,” Milos Ilic-Miloradovic, the issuer’s Sydney-based treasurer, told KangaNews.

“Anecdotally, we have received reports from our origination network of increasing dishonours leading to an increase in 1-30 day arrears. But there is no evidence of any trend or breakout of the range experienced over the past two years at portfolio level.”

Button TextASSET RESILIENCE

Higher interest rates have had an impact on loan serviceability, particularly for home owners rolling off fixed rates and refixing at double or triple what they had been paying previously. A Fitch Ratings report from March 2020 said the standard New Zealand mortgage had a fixed term of between six months and five years. CoreLogic data suggest around 60 per cent of New Zealand mortgages were due to be refinanced in 2022.

This leaves the market at an interesting juncture in late 2022. Rates are still rising and at the same time there is a lagging effect from the preponderance of fixed-rate loans. This is leading to understandable caution on the investor side.

“We are tracking the performance of fixed loans in a rising rates environment especially closely,” says Victoria Gao, ABS portfolio manager at CIP Asset Management in Sydney. “Fixed rates mean the impact of higher interest rates is lagged, so the current sound performance we have seen to date may not provide the best leading indicator for the months and years ahead.”

Even so, Gao says CIP is “still actively investing where we see value”. While the backdrop is clearly still uncertain, local market participants also believe firmer ground may be in sight. The consensus among economists is that the RBNZ will keep hiking in 2022, taking the OCR to at least 4 per cent. But it may pause at that stage.

“We should see expectations adjust and margins normalise over the next six months,” says MTF Finance’s Dunedin-based head of treasury and funding, Fraser Wilson. “We have been through this before – but not to the extent we are experiencing currently.”

The signs so far are that borrowers are meeting their obligations. Delinquency rates are holding steady despite a fairly aggressive spate of rate hikes, says Tally Dewan, financials and securitisation strategist at Commonwealth Bank of Australia in Sydney. “So far it seems borrowers are very resilient – they have been able to save money, which is cushioning rate rises.”

The same story comes from lenders with personal and auto finance books. Wilson comments: “About 30 per cent of our borrowers are homeowners, so higher rates – along with changes to the Credit Contracts and Consumer Finance Act (CCCFA) and higher vehicle prices – have contributed to an increasing proportion of borrowers seeking five-year loan terms.”

So far, says Wilson, MTF’s arrears greater than 30 days are still at a record low. “Anecdotally, we have received reports from our origination network of increasing dishonours leading to an increase in 1-30 day arrears. But there is no evidence of any trend or breakout of the range experienced over the past two years at portfolio level,” he says.

Mark de Ree, head of treasury at UDC Finance in Auckland, adds: “We are confident the vast majority of our customers are well placed to handle the dual challenges of higher interest rates and increased living costs. In part this reflects demand in the economy that is running ahead of supply capacity. People are employed or their businesses are operating at or near full steam, so they have the ability to make loan repayments.”

New Zealand lenders are also quick to point out that local credit standards support market resilience. The CCFA changes require borrowers to meet stricter criteria. “Lenders have applied a more robust process across the spectrum,” says Avanti Finance’s Auckland-based head of funding, Caroline Dunlop. She also notes that the change in legislation was well-timed for an era of higher interest rates.

On the other hand, idiosyncrasies of the New Zealand market add to the challenges. In particular, its population – and therefore loan distribution – is concentrated in three centres: Auckland, Christchurch and Wellington. This makes it hard for securitisation to offer the diversification investors crave. Realm Investment House’s Melbourne-based partner and investment manager, Rob Camilleri, tells KangaNews: “New Zealand issuers are concentrated within a small geographic region, so we don’t get the diversity we get with an Australian programme.”

“We are confident the vast majority of our customers are well placed to handle the dual challenges of higher interest rates and increased living costs. In part this reflects demand in the economy that is running ahead of supply capacity. People are employed or their businesses are operating at or near full steam, so they have the ability to make loan repayments.”

Button TextFUNDING OUTLOOK

Overall, however, issuers remain somewhat optimistic. The pandemic was a test of consumer resilience, they tell KangaNews, but borrowers are so far keeping up with repayments. With a plateau in the rates cycle perhaps not far away, the dynamics of funding are starting to settle.

Domestic and Australian demand for New Zealand securitisation is still relatively robust, Wilson says, as higher margins are catching the attention of potential buyers. Limited supply is an advantage in this context. “There seems to be a healthy level of demand from investors that have not had the opportunity to participate in transactions this year due to preplacing of notes,” Wilson adds.

As investors wait for issuance to pick up, borrowers are watching for trends in demand. Avanti’s Auckland-based group treasurer, Paul Jamieson, highlights growing interest in the securitisation asset class from institutional funds managing KiwiSaver money – a pool worth NZ$92 billion at March 2022.

“We have seen a lot more funds come into securitisation from KiwiSaver in the last couple of years,” Jamieson comments. “The pool of investors in New Zealand interested in securitisation has widened and we expect this to continue.”

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

Related news