Investor sentiment unveiled

KangaNews Sustainable Finance and Commonwealth Bank of Australia conducted their third annual survey of environmental, social and governance sentiment among Australian fixed-income investors in August 2022. Sustainable investment approaches are evolving but asset managers report that, in some cases, they are effectively being forced to take backward steps by asset owners.

Helen Craig Head of Operations KANGANEWS

Samantha Swiss Chief Executive KANGANEWS

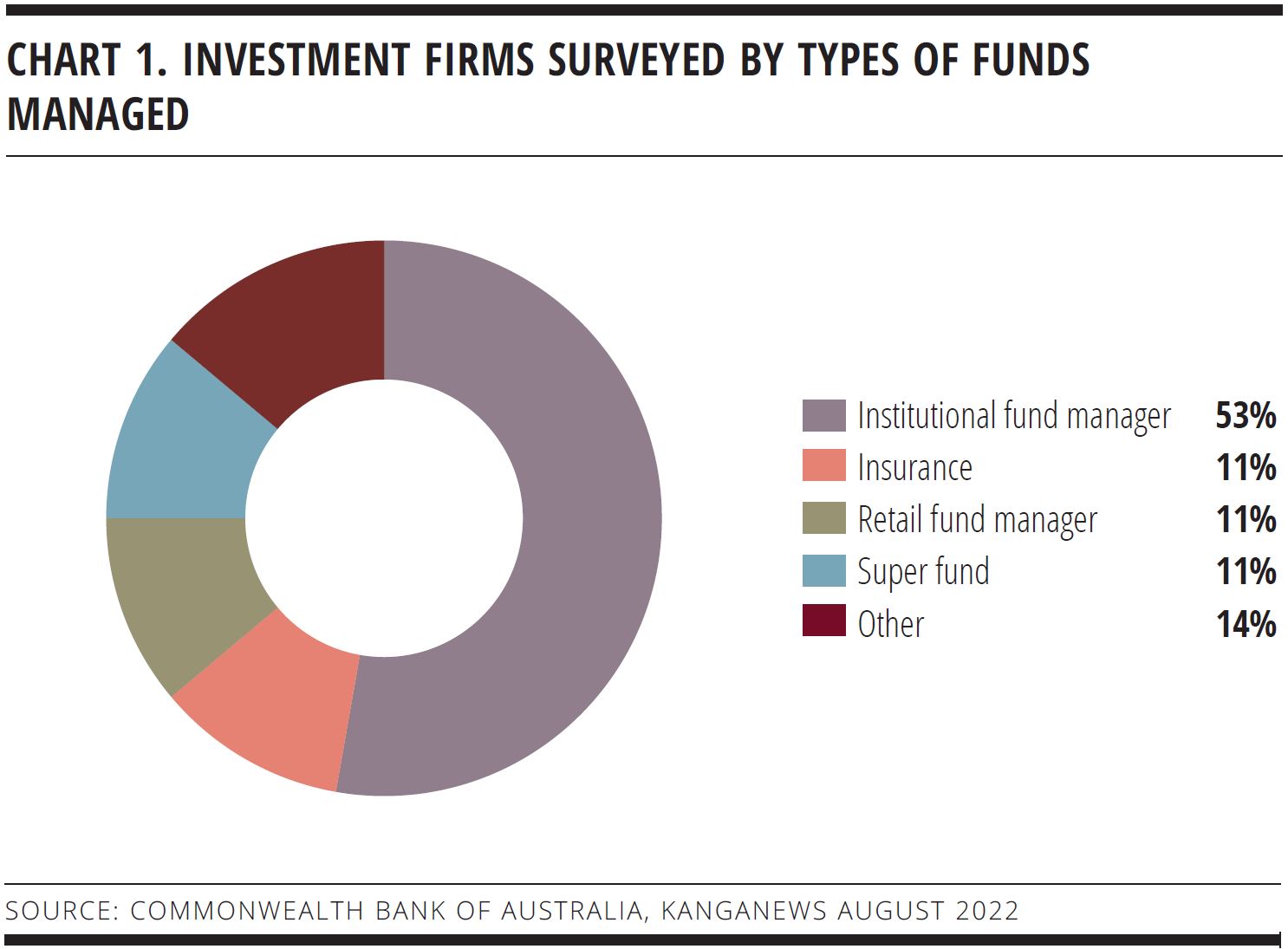

More than 35 Australian-based investment firms completed the survey. They include boutique funds, asset managers and owners, and private debt funds (see chart 1). The survey did not target specialist ESG investors but combines the views of fund managers with specific mandates in the space with those of mainstream fixed-income managers.

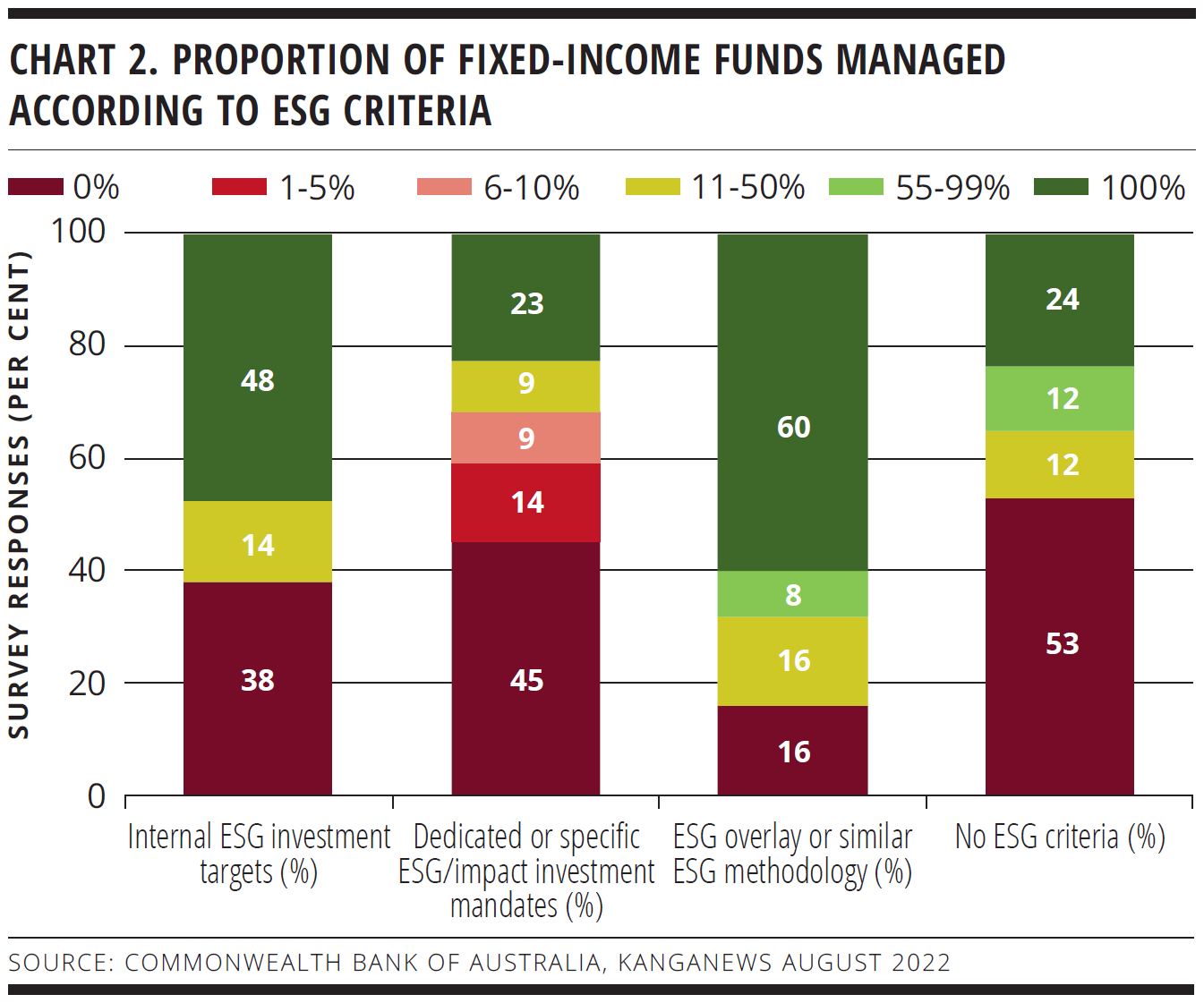

The proportion of fixed income managed under ESG mandates in Australia is not significantly different from 12 months ago, according to the survey results. In 2022, 84 per cent of respondents indicate their firms apply an ESG overlay to more than 10 per cent of their assets under management (see chart 2), compared with 79 per cent in 2021. In both years, around 60 per cent of respondents say they have this approach across all their funds.

Market participants say they have noticed a change in tone since the previous survey was undertaken, though. Anthony Kritikides, managing director, institutional sales at Commonwealth Bank of Australia (CBA) in Sydney, says standards have risen because investors are more sophisticated and have subsequently increased their demand for information.

He comments: “In 2020-21, it felt like every deal we brought to market was a huge success: each was oversubscribed and priced attractively, for issuers at least. Around this time last year, we started to note that conversations with investors were getting harder – that the tide was turning. This has brought us to more difficult territory for issuers, as investors are demanding a lot more when ESG tagged bonds are brought to market.”

CBA also invited investors to a roundtable discussion to analyse the survey results. Participants say environmental, social and governance (ESG) has become a more authentic discussion with seasoned clients, which has led to an increase in sophistication in investment approaches when applying ESG strategy.

However, at the same time they point to the role played by clients that are engaging with sustainability for the first time, which can pull asset managers back to older-style investment approaches like divestment and exclusions. Meanwhile, fund managers continue to seek greater ambition in issuer targets and transition.

““In 2020-21, it felt like every deal we brought to market was a huge success: each was oversubscribed and priced attractively, for issuers at least. Around this time last year, we started to note that conversations with investors were getting harder – that the tide was turning. This has brought us to more difficult territory for issuers, as investors are demanding a lot more when ESG tagged bonds are brought to market”

Button TextLINE OF ATTACK

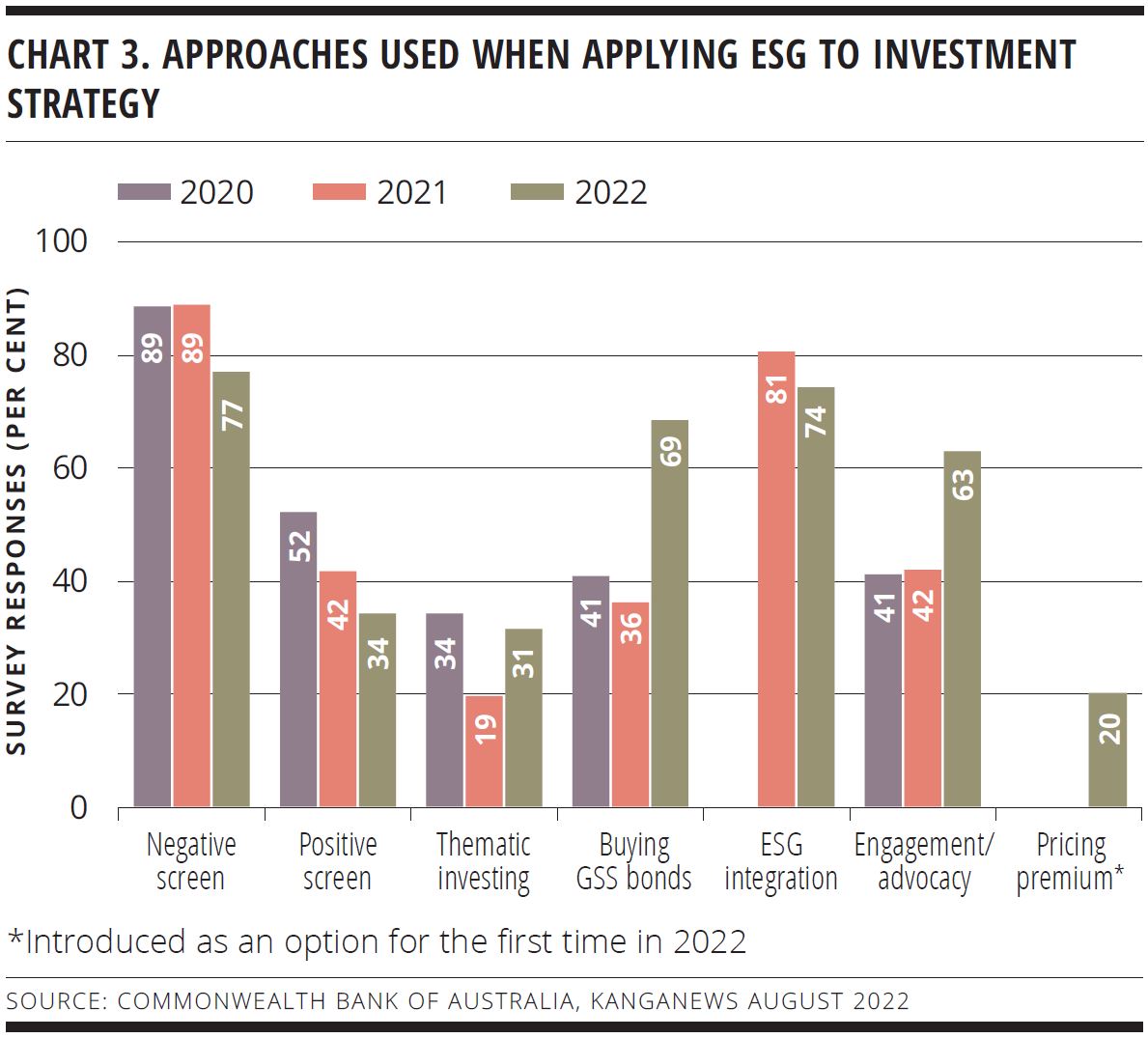

The survey certainly suggests investor ESG approaches are becoming more sophisticated. Negative screening was by far the most favoured approach by respondents to the 2020 and 2021 surveys, used by 89 per cent on each occasion, while the next most-used single ESG approach in both years was positive screening at 52 and 42 per cent respectively. In 2022, no single approach stands out. Responses are more evenly spread with 77 per cent of respondents saying they use negative screening, 74 per cent that they integrate ESG into the credit process and 69 per cent that they buy labelled ESG bonds (see chart 3). The popularity of positive screening appears to be on a downward trend, however.

One driver for the evolution beyond screening is increased interest in ESG from end clients. Several investors at the roundtable said client demand to complete questionnaires and requests for ESG-specific meetings have skyrocketed.

According to Marayka Ward, director, sustainable investments, liquid markets group at QIC in Brisbane, there are a few reasons for this. “End investors are increasingly interested in more sensitive sectors and there has also been regulatory prompting and modern slavery legislation,” she said at the roundtable. “There is greater pressure on our clients to be incorporating ESG and, by default, they are asking their fund managers for more detail on their processes.”

On the legal and regulatory front, Ward pointed to the Australian Prudential Regulation Authority’s Prudential Practice Guide CPG 229 – Climate Change Financial Risks as well as the Hutley and Mack legal opinion for superannuation trustees on how to fulfil their legal obligations with respect to climate change risk.

“It can’t just be a case of electing not to invest in fossil fuels. There is a simplistic view about exclusion lists that is not always the best approach, particularly given the requirement of green mining in the likes of aluminium, copper, cobalt and lithium that are critical for transition economies.”

Button TextInvestors note strong demand for understanding the ESG perspective across the board – from smaller wholesale clients to larger superannuation funds. This is driving demand for ESG integration from the demand side.

In the private-debt sector, Lucie Bielczykova, Sydney-based portfolio manager at Revolution Asset Management, said demand for ESG integration is also being supported by supply. For instance, she revealed, the first sustainability-linked syndicated leveraged loan was executed in Australia in the past 12 months. “It originated from a European sponsor, demonstrating influence from offshore into the local ESG space that is leading to newer, emerging products,” she added.

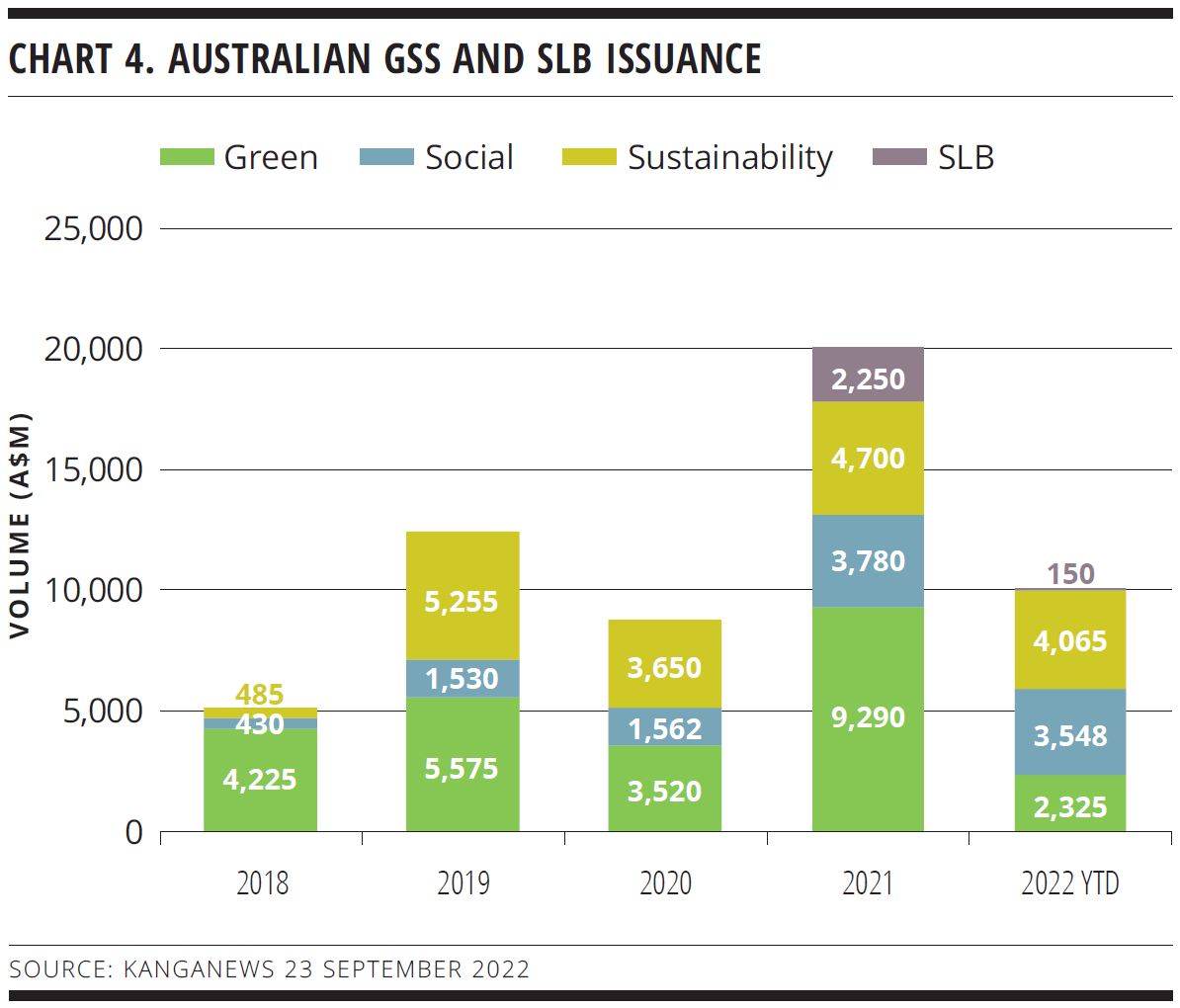

Bond supply is not keeping pace with burgeoning demand in the local market. According to KangaNews data, 2022 is set to be the lightest year for green-bond issuance in half a decade, while the excitement about a new product – sustainability-linked bonds (SLBs) – coming onstream in 2021 has eased this year with only one SLB issued to the end of September.

However, participants at the roundtable discussion said the primary reason current-year issuance has fallen is the lack of issuer and investor alignment on pricing and tenor across the market rather than ESG considerations.

David Gallagher, head of Australian fixed income at Artesian Capital Management in Sydney, commented: “Higher outright yield means investors are averse to longer duration, particularly with ongoing volatility. With three-year bank bonds at 4 per cent yield, adding credit provides a security with a lot less duration risk than the 7-10 year part of the curve.”

Gallagher said there would likely be more demand if there were more ESG-aligned deals at 3-5 year tenor. “Many of this year’s transactions have been at 7-10 year maturity, from real estate investment trusts or universities, and they have also had relatively small volume,” he explained.

But as Charles Davis, managing director, sustainable finance and ESG at CBA in Sydney, pointed out, the 3-5 year space is traditionally where the loan market is at its most competitive. “Historically, the crossover from loans to bonds has generally been at about the five-year tenor point, as there is more favourable pricing for longer tenor in the bond market and for shorter tenor – with greater flexibility – in loans. I don’t expect a shift in this dynamic.”

To some extent, lower primary supply has been offset by a more active secondary market, including in green, social and sustainability (GSS) bonds.

According to Gallagher, this is a unique situation. “At the height of the pandemic the market experienced large redemptions,” he said. “While we avoided further outflows in the recent run of volatility, index players have not. Essentially, fund managers sell vanilla bonds before labelled securities – but if the selling keeps coming they have to hit the bid eventually. I think it got to that point: there were huge flows out of bond funds and even the coveted labelled securities hit the streets.”

Davis added that this is an interesting shift from last year’s narrative. “What I’m hearing is that labelled securities are still the last to be sold – but we are starting to see the last being sold now.”

“Historically, the crossover from loans to bonds has generally been at about the five-year tenor point, as there is more favourable pricing for longer tenor in the bond market and for shorter tenor – with greater flexibility – in loans. I don’t expect a shift in this dynamic.”

Button TextNEW ENGAGEMENT

With 63 per cent of investors ticking this box, engagement and advocacy is one of the most favoured ESG approaches for debt investors. Roundtable participants argued that, rather than playing catch up with the equity market, fixed-income investors’ influence is complementary and just as effective.

There tends to be a delineation between the role of equity and fixed-income investors as the nature of their engagement is different. But CBA believes the ability of even individual debt investors directly to influence cost of capital is significant and should not be swept under the carpet just because equity investors have a wider presence and easier access to boards and management.

Gallagher argued that the nature of labelled debt forces issuers to be more focused on the detail, comparing these offers to share offerings. “In an equity pitch, half the deck will not be devoted to sustainability,” he argued. “When debt issuers and investors meet, there is a sharper level of engagement.”

Kylie-Anne Richards, Sydney-based deputy chief investment officer at Fortlake Asset Management, added that the buy side is asking deeper questions about ESG – a sign the market is starting to mature. However, she also noted that the differences between fixed-income and equity investment need to be acknowledged, in particular by addressing the additional complexity of the debt asset class.

Richards commented: “In Australia alone, we have around 1,700 investment grade bonds from 80-odd issuers. Of those issuers, only about 40 have an MSCI rating – and even these ratings do not account for the differences in ESG risk associated with different tenors. The challenges are greater for fixed income, but it is a more natural conduit to allocating capital to address climate change.”

INTO DETAIL

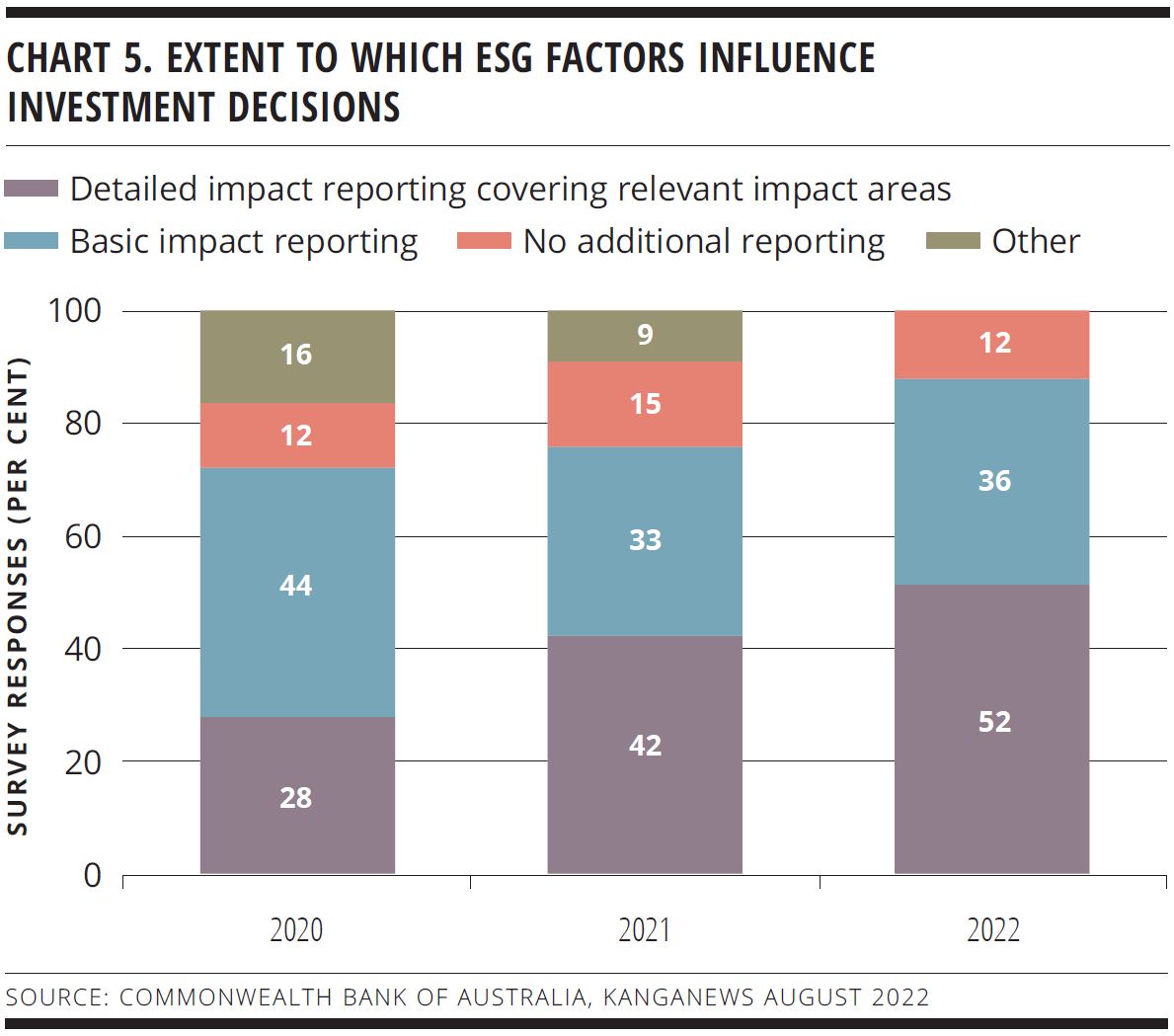

Investors’ expectations on issuer reporting continue to increase. More than 50 per cent of respondents to the 2022 survey require detailed impact reporting compared with 36 per cent in 2021 and 12 per cent in 2020 (see chart 5).

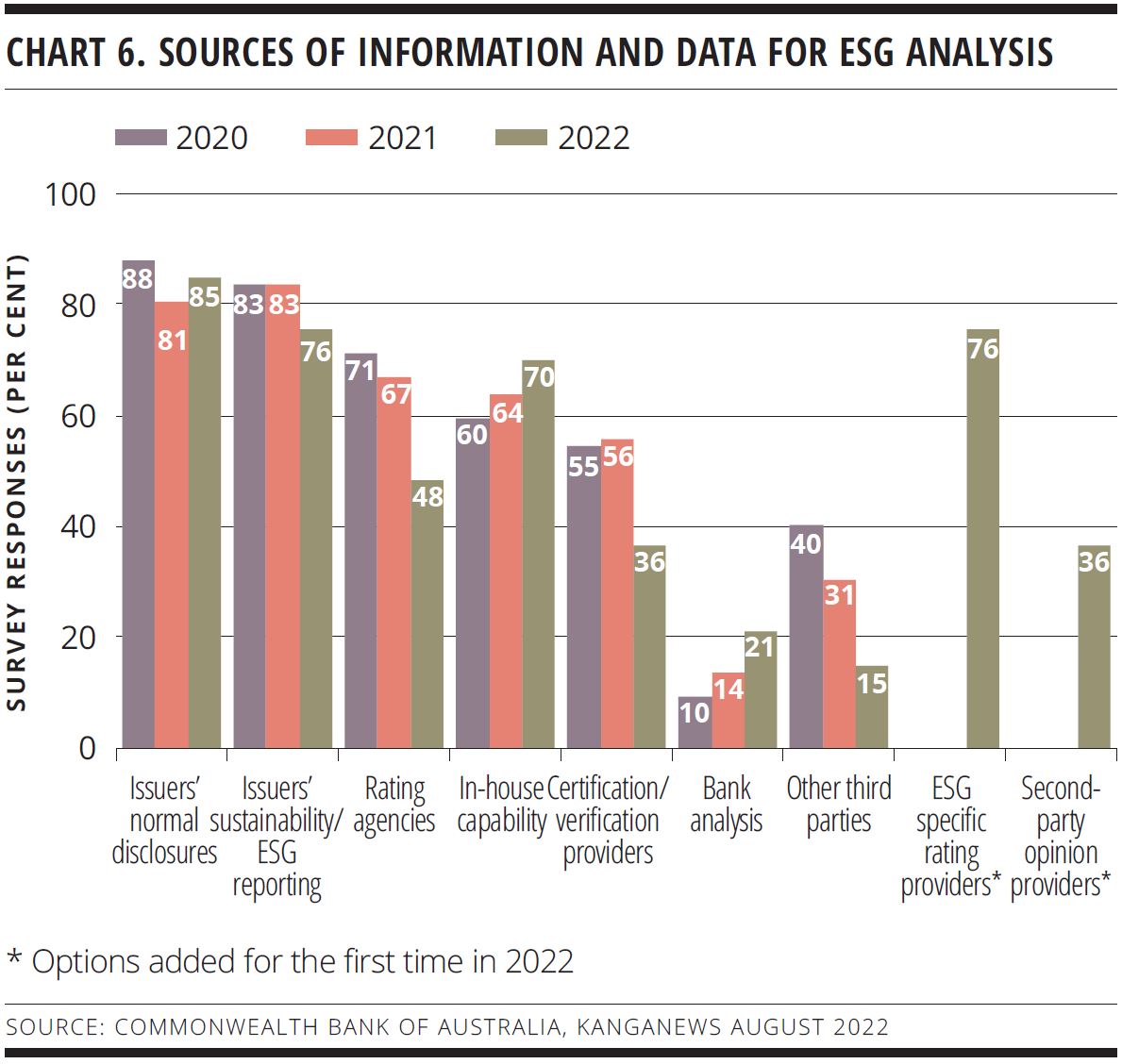

When asked where investors source information and data required for ESG analysis, 85 per cent of survey respondents say issuers’ normal disclosures and 76 per cent cite issuers’ specific sustainability or ESG reporting. In 2022, 70 per cent of respondents also nominated in-house capability as a source of information and data for ESG analysis (see chart 6). The buy side also reports leaning heavily on ESG-specific ratings – much more so than information from second-party opinion providers.

Another survey question asked investors which of a range of factors are the most significant barriers to GSS market growth. For the first time in the survey’s history, the most popular response was a lack of consistency in reporting requirements.

Davis argued: “The local market is at an interesting stage of evolution in the wake of the November 2021 release of CPG 229 and other regulatory requirements that are attempting to drive standardisation in reporting, while at the same time market participants have also developed their own processes and questionnaires.” All this could prove to be a prelude to a future mandatory reporting regime, which market participants increasingly believe to be an inevitable development (see p42).

Murray Ackman, ESG credit analyst at Pendal Group in Sydney, said standardisation of reporting is not the biggest problem, though. “We look at things like gender equality or emissions because they are relatively easy to compare. However, they often do not provide us with the information our clients really care about,” he suggested.

Deciding whether a company is on the right or wrong side of the ledger with its climate transition strategy is hard, and anticipating end-investor response even harder. Ackman continued: “We can look at a company’s emissions profile but it will not tell us whether our clients would want us to exit a position, to challenge a company – either privately or publicly – or trust its transition plans. Standardised reporting is not going to solve this challenge.”

Deeper disclosure of information would help. Ackman said: “With fixed income, we try to persuade private issuers to disclose information they don’t necessarily have to report. For our vanilla funds, we talk with issuers for greater disclosure. However, our sustainable strategies have specific outcomes we want to achieve through engagement. Our assessment of impact requires bespoke information tied to the specific objectives and philosophy of our funds.”

“As our debt is illiquid we have a further complication: we have refinancing risk at the end of the loan term. Some of this is already reflected in pricing but it is less so within certain sectors. Over the next few years, I believe the market will mature to reflect this nuance.”

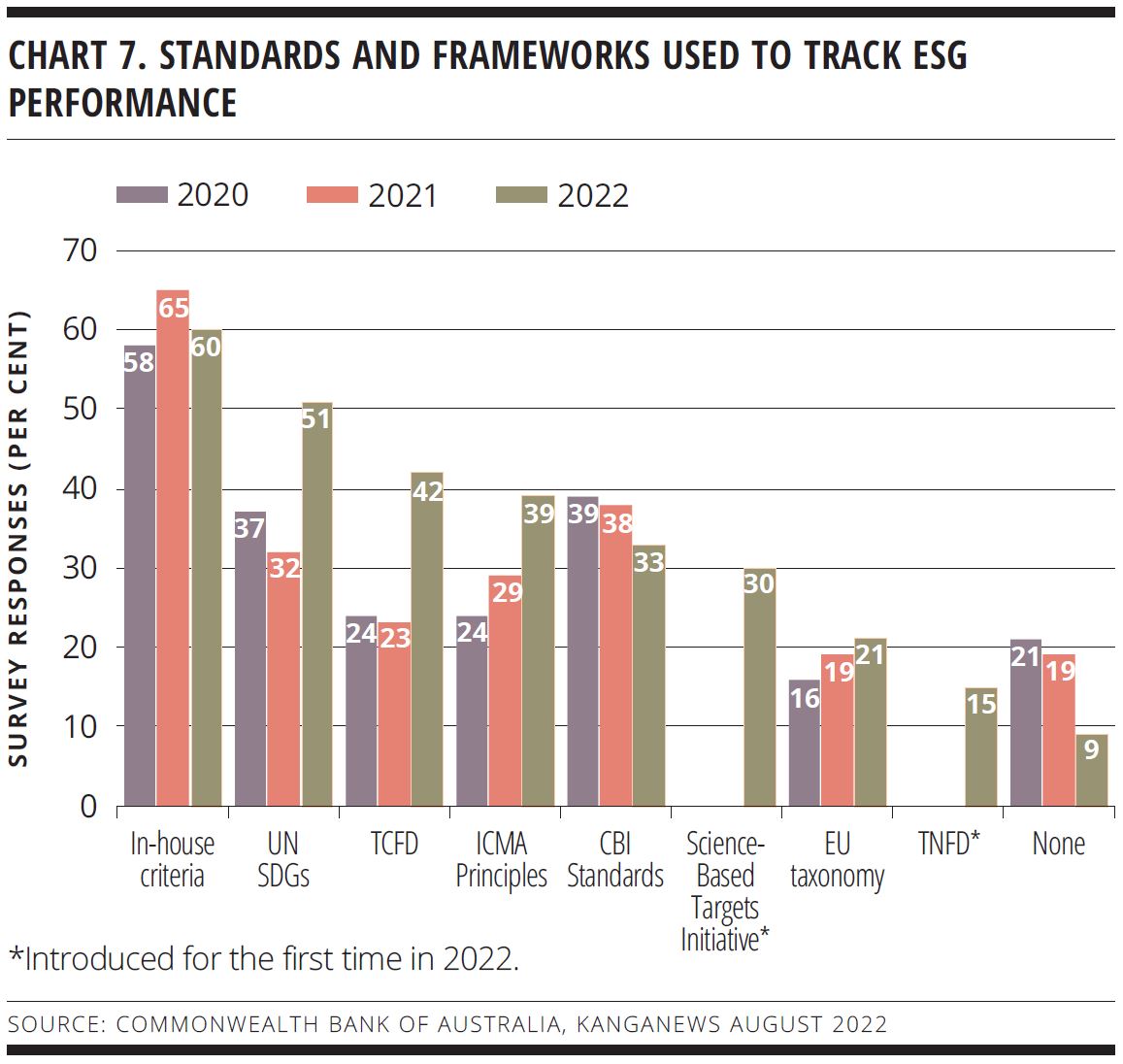

Button TextIn public markets, more types of data are becoming available. While in-house criteria remain the main source for tracking ESG performance, the 2022 survey shows, for the first time, a surge in respondents saying they use external frameworks (see chart 7).

Ward revealed that QIC has been focused on encouraging unlisted issuers to disclose data since 2016, and this work is now starting to come to fruition. “In most cases, we have found unlisted issuers have the data but they want to understand why we want to see it. Talking them through the kind of reporting our clients require has led to a notable maturity in disclosure,” she revealed.

Ward believes the next step for engagement in the domestic market is growth in collaboration and thematic behaviour. “An example is picking themes associated with climate change and talking to companies that have not set targets. In this sense, we will be moving from disclosure to much more thematic engagement.”

In the private space, lack of data availability continues to be an issue. Bielczykova said: “It is definitely our biggest struggle that there are such limited data among our universe of companies – which are private, unlisted and mid-market.”

Smaller companies can lack the resources and bandwidth to provide detailed information and are yet to be subject to the same kind of public push as larger, listed companies. As a strategically important partner to these types of companies, Revolution is also using engagement to seek what it requires.

Bielczykova explained: “There is often just a handful of lenders in a syndicate compared with hundreds of bond owners. We can therefore engage with borrowers directly and shape loan terms. If we want an issuer to start reporting certain data, we can push to incorporate them into loan documentation. Typically, we have found borrowers are open to this.”

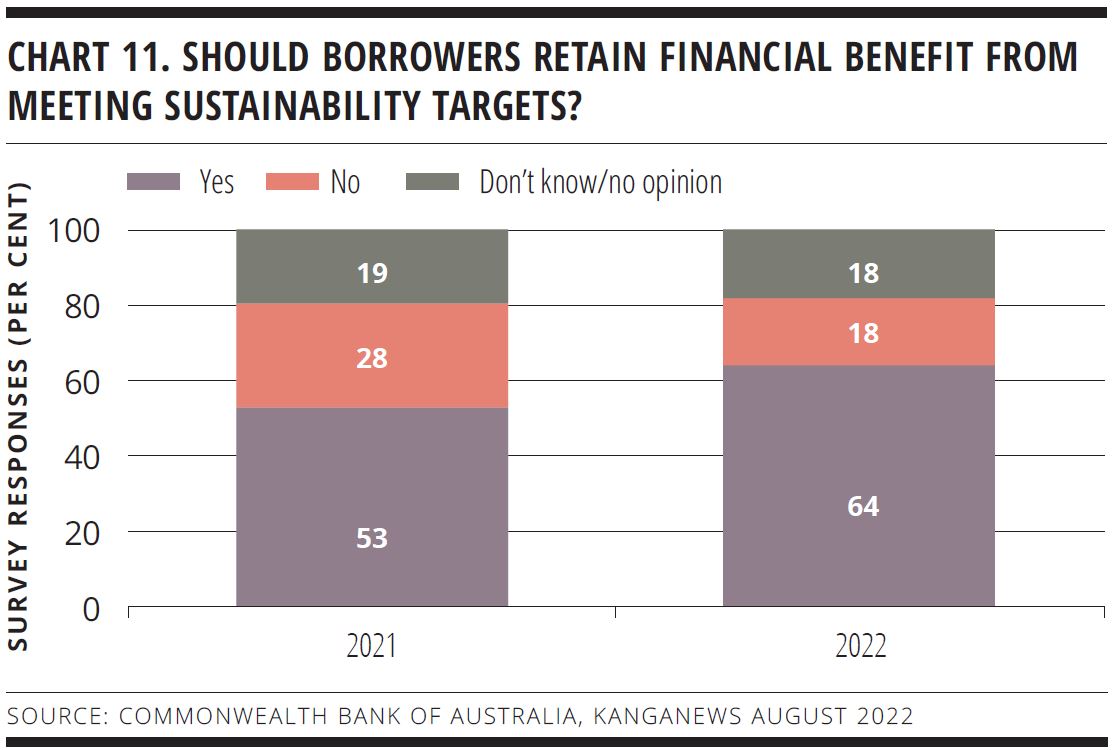

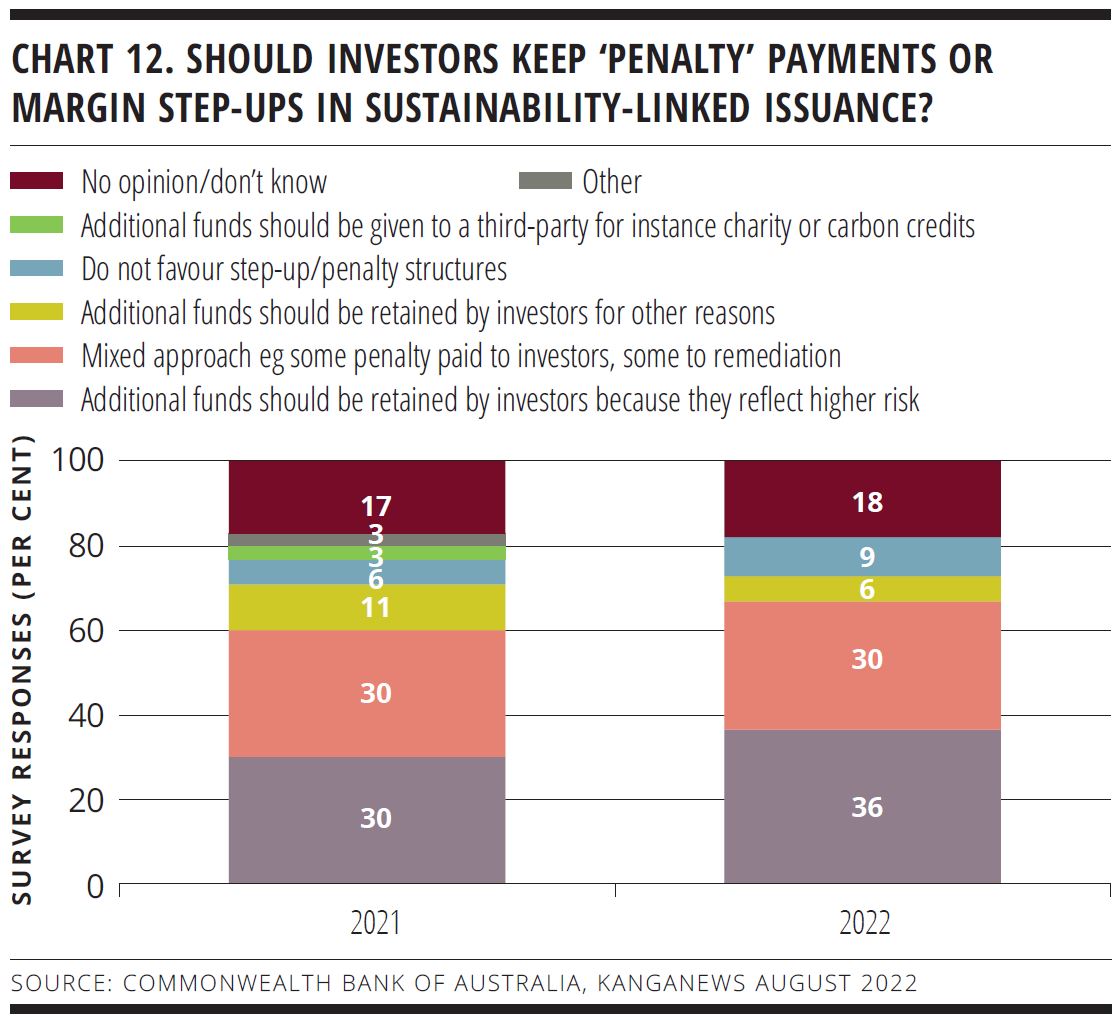

Financial benefits from sustainability targets

The Commonwealth Bank of Australia- KangaNews Sustainable Finance survey asked for investor views on the treatment of incentives for missed and met sustainability targets, for investors and issuers.

The 2022 results suggest the argument for borrowers to benefit from met targets is more straightforward than investors benefiting from missed targets. Almost two-thirds of respondents in 2022 believe borrowers should retain financial benefit if they meet targets, up from just more than 50 per cent in 2021 (see chart 11).

As for investors, 42 per cent of survey respondents believe investors should keep ‘penalty’ payments, while another 30 per cent favour a mixed approach that combines payment to investors and payment to remediation (see chart 12).

The difference between the responses is not difficult to explain. The idea of investors receiving a financial benefit from borrowers missing performance targets does not sit right with some market participants.

There is more to the story, however. For instance, Murray Ackman, ESG credit analyst at Pendal Group, thinks it is fair to compensate investors if targets are missed. “If targets are not met, it will no longer be viewed as an ESG security from our perspective. It is a vanilla bond and, given we may have bought it for our dedicated ESG funds, we may need to sell it.”

STRANDED FINANCING

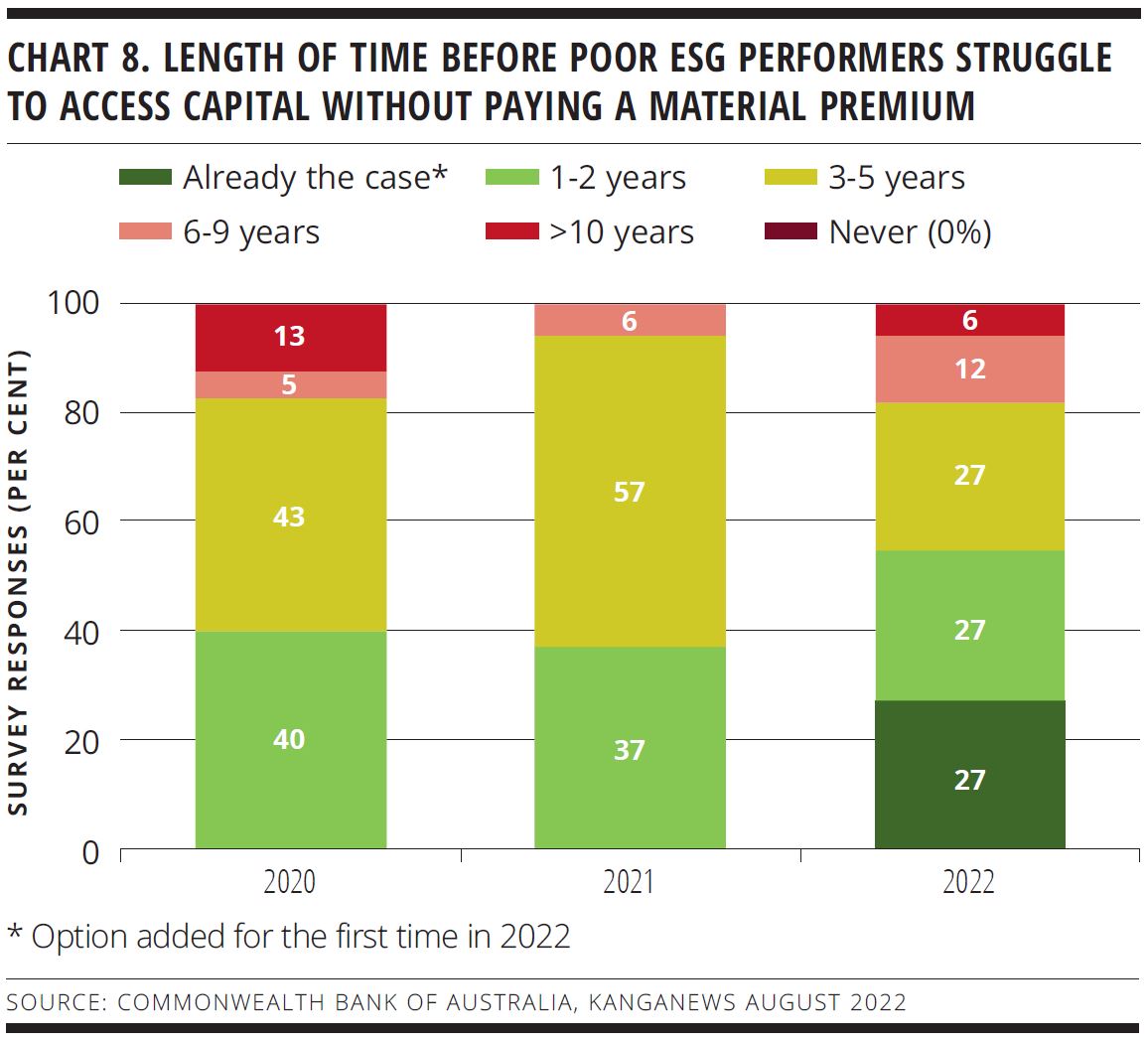

Investors appear to believe the window in which issuers will be able to access capital without paying a material premium for poor ESG performance is narrowing, though opinions differ. For the first time, more than half of survey respondents believe poor performers will be paying more for capital within two years (see chart 8). On the other hand, as many investors as ever – 18 per cent – believe this premium will not emerge in the next half decade.

Bielczykova noted that reputation events relating to ESG play heavily in certain industries in the private-debt space, and that this can cause companies to lose access to capital. “Loan pricing for a transport company servicing the mining sector is very wide compared with other types of transportation,” she said. “No-one wants to touch anything to do with heavy emitters.”

This could be a factor of private debt’s long-term view. Bielczykova added: “As our debt is illiquid we have a further complication: we have refinancing risk at the end of the loan term. Some of this is already reflected in pricing but it is less so within certain sectors. Over the next few years, I believe the market will mature to reflect this nuance.”

In the public market, investors report examples where the pricing of a primary deal compared with the same issuer’s curve implies a cost for certain sectors to access capital. Meanwhile, traditional credit rating agencies are increasing their focus on and scrutiny of stranded financing risk.

“We all like to say we support the financing of transition stories and we would like to see transition bonds, but client appetite makes it extremely difficult. Clients have publicly committed to net zero targets and visibly do not wish to finance poor emitters. It is easy to add names and sectors to an exclusions list and it is incredibly difficult to convince a superannuation board that a company is no longer a risk.”

Button TextFor Ward, stranded financing risk will likely start to become a real issue for the bond market later this decade. She commented: “Now more clients are interested in ESG and ESG reporting, we risk moving back toward exclusions to some extent. This is because some clients are looking at this space for the first time for their fixed-income portfolios and the natural reaction is, for example, to get rid of the top 10 emitters.”

Other roundtable participants acknowledged the extent to which stranded financing risk applies to hard-to-abate industries. “There is idiosyncratic ESG risk that wasn’t there yesterday but is in today’s headlines – and this is not necessarily specific to one industry. This risk starts to get priced in when we start to see a rap sheet of ESG misdemeanours,” Gallagher explained at the roundtable.

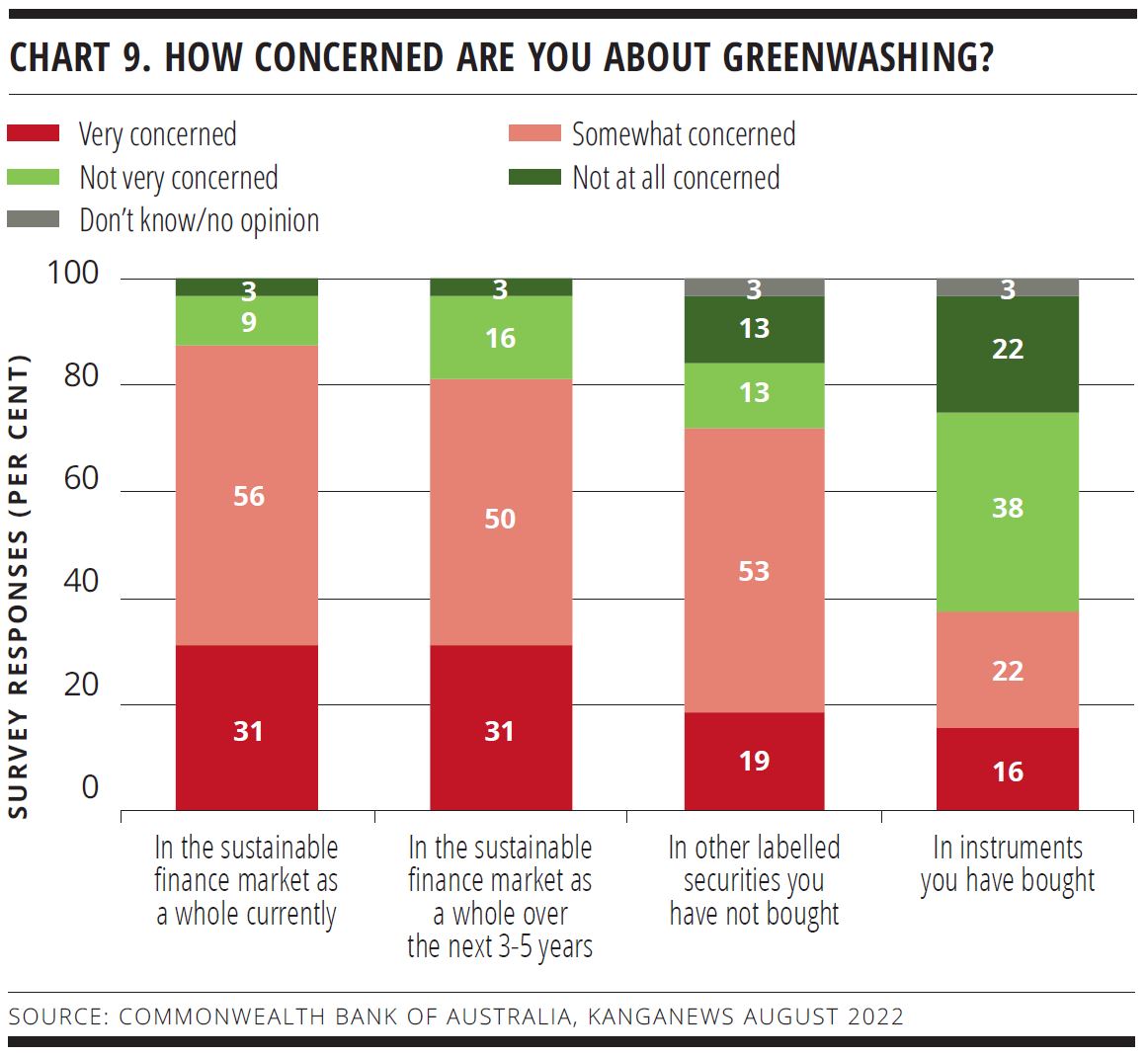

Greenwashing concerns – from regulators, investors and commentators – have escalated in 2022. A new question in the 2022 survey shows Australian investors are aligned with this trend, with 31 per cent saying they are very concerned about greenwashing currently, while 56 per cent are somewhat concerned (see chart 9).

“The local market is at an interesting stage of evolution in the wake of the November 2021 release of CPG 229 and other regulatory requirements that are attempting to drive standardisation in reporting, while at the same time market participants have also developed their own processes and questionnaires.”

“We can look at a company’s emissions profile but it will not tell us whether our clients would want us to exit a position, to challenge a company – either privately or publicly – or trust its transition plans. Standardised reporting is not going to solve this challenge.”

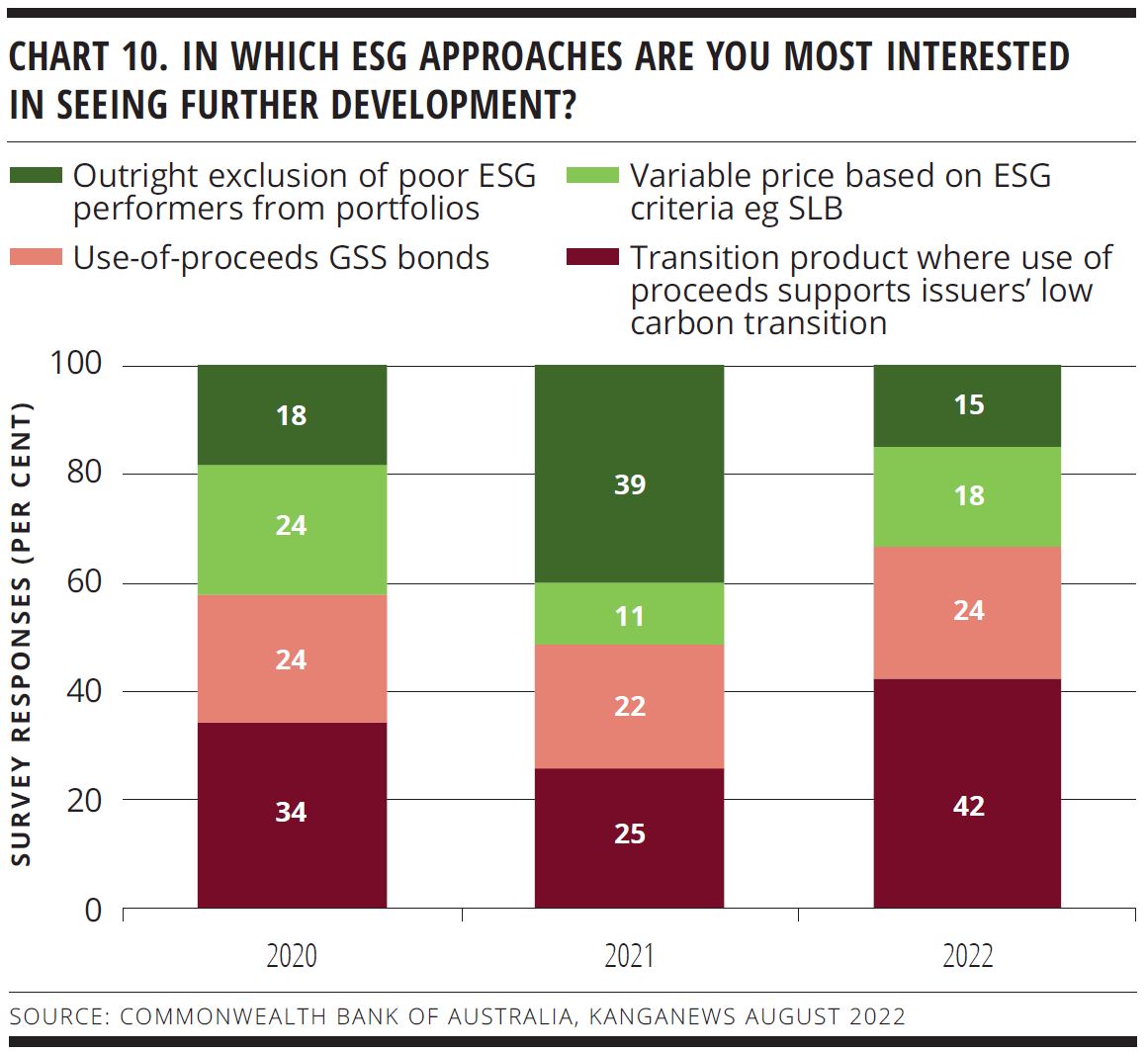

Button TextFUTURE DIRECTION

Survey respondents reveal a strong preference for further development of transition product – where use of proceeds (UOP) supports issuers’ low-carbon transition (see chart 10). In 2022, 42 per cent of respondents voted this their top choice for further development, compared with 25 per cent in 2021 and 34 per cent in 2020.

However, it can be complex for end investors to understand the nuances of transition product, including SLBs. Ackman said: “There are examples of green bonds that incorporate renewable energy and which therefore provide good bang for our buck for emissions avoided. However, there can be deep concerns at issuer level because the same companies have not said they will not finance fossil fuels. The bond is doing good but investors have to ask if they are supporting an issuer that is not.”

Ward agreed, saying: “We all like to say we support the financing of transition stories and we would like to see transition bonds, but client appetite makes it extremely difficult. Clients have publicly committed to net zero targets and visibly do not wish to finance poor emitters. It is easy to add names and sectors to an exclusions list and it is incredibly difficult to convince a superannuation board that a company is no longer a risk.”

This problem is particularly acute when it comes to investor clients that are newer to the ESG sector. Ward explained: “We have clients that are very sophisticated and with which we have been having appropriate discussions for a number of years. But we also have clients newer to the space that need educating about what can be measured and achieved in a fixed-income portfolio. They will get up to speed over time but are not there yet. These clients are dominating what we are able to do at the moment.”

Richards agreed that a step-up in education on transition is needed. “It can’t just be a case of electing not to invest in fossil fuels. There is a simplistic view about exclusion lists that is not always the best approach, particularly given the requirement of green mining in the likes of aluminium, copper, cobalt and lithium that are critical for transition economies.”

Survey data point to SLBs as the crucial bridging instrument between UOP labelled bonds and transition financing. Close to one-fifth of 2022 survey respondents say they are interested in the further development of the SLB asset class, compared with around 10 per cent in 2021.

Ward said her preference for SLBs over UOP bonds revolves around the greater potential impact SLBs have in incentivising portfolios and companies to transition. “I will buy either product – and it is true that UOP bonds can be much easier to explain to clients. But when we think about where we need our portfolios to transition to – including things like setting climate targets in portfolios – the style of security that could have the most potential impact is the SLB.”

Bielczykova agreed. “What gets us excited about sustainability-linked product – in our case sustainability-linked loans [SLLs] – is the greater potential for any corporate to take up an SLL. There has to be rigour in KPIs and measurement, but they have much broader application and greater potential for more companies.”

Demand for GSS issuance has remained relatively consistent over the three years of the CBA-KangaNews Sustainable Finance survey, with 20-25 per cent of investors saying they would like to see further development of labelled product in every year to date.

Gallagher said Artesian, which has a dedicated green and sustainable bond fund, prefers the UOP instrument because it is easier for clients to understand owing to the ringfenced nature of the asset pool. However, despite the additional due diligence required for SLBs, he said linked product would pique greater interest if it came with deeper KPIs.

“The SLB targets that have been set in Australia, which are generally just mapping to net zero goals, are not sufficiently aspirational,” Gallagher argued. “Big corporates have these goals anyway so I am not convinced they create a lot of impact – internally or externally.”

Ackman added: “There are much better stories for clients directly funding assets through a UOP bond. For us to get excited about SLBs, they need to be ambitious and different from business as usual – and we haven’t seen this yet in Australia. Almost every issuer can say its biggest emissions are through electricity usage so it is highly unambitious to aim for an percentage reduction by a point in time. We want more ambition than this.”

“While we avoided further outflows in the recent run of volatility, index players have not. Essentially, fund managers sell vanilla bonds before labelled securities – but if the selling keeps coming they have to hit the bid eventually. I think it got to that point: there were huge flows out of bond funds and even the coveted labelled securities hit the streets.”

Button TextSponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.