SSA Kangaroo market changes shape again as demand shifts

The supranational, sovereign and agency Kangaroo market kicked off 2022 with a near-record first quarter but then slipped into the doldrums as fundamental and technical challenges slowed deal flow to a crawl. The sector has been through difficult times before, however, and dealers say the longer-term outlook remains healthy.

Lisa Uhlman Senior Staff Writer KANGANEWS

Since Russia invaded Ukraine in late February, global debt markets have faced challenging circumstances including accelerating inflationary pressure and rapid central bank rate hikes. The effects have been felt across markets, but the most noticeable impact on the sovereign, supranational and agency (SSA) Kangaroo sector was a draining of demand starting with a significant selloff from the Japanese investors that have been one of its key pillars of support over recent years.

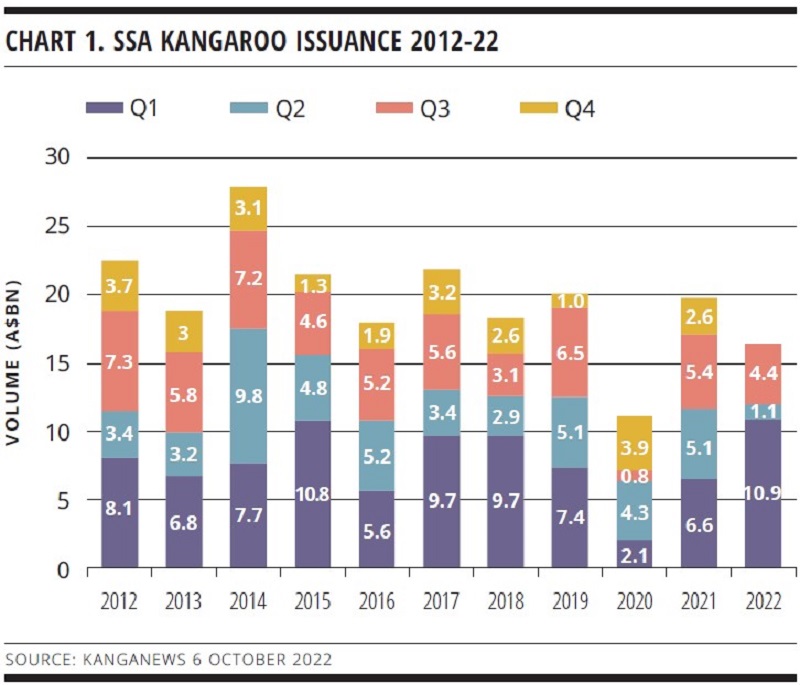

After nearly A$11 billion (US$6.9 billion) of issuance volume in the first quarter of 2022, the SSA market barely topped A$1 billion in Q2 as the macro deterioration took hold and the Japanese selloff affected technicals (see chart 1).

It is certainly not unusual for Kangaroo issuance dynamics to follow this pattern as most SSAs typically start the calendar year with a flurry of issuance before settling into a slower pace. But 2022 saw the busiest first quarter since 2015 and the quietest second for more than a decade – an extreme example of the usual pattern.

Issuance picked up in the third quarter to be roughly in line with the historical average: A$4.4 billion priced in 2022 compared with A$5.2 billion on average over the preceding decade.

Market sources say numerous factors, including the elevated yields and wide swap spreads available in Australia, provided tailwinds at the start of the third quarter.

SWITCHBACK RIDE

However, the global market backdrop shifted again from late September, with a much more negative tone pervading and investors returning to a strongly risk-off approach. SSA Kangaroo issuance slowed again into the end of Q3 leaving an uncertain near-term outlook.

The SSA recovery in the early part of Q3 flew under the radar to some extent, coming as it did in the traditionally quiet northern hemisphere summer. But dealers say fundamentals had clearly changed since the dire Q2. “There was a period of relative stability, prompting a reasonably strong rally in risk assets globally,” explains Yuriy Popovych, Singapore-based director, fixed income at TD Securities. “Risk tone improved across markets and sentiment improved across every asset class, which gave investors confidence to put their money back to work.”

Whether this signifies much for the medium-term outlook is hard to say as the global battle with inflation reared again late in Q3, delivering a serious knock to the green shoots of market confidence. The SSA Kangaroo market once again fell silent, with no trades at all pricing between a A$500 million European Investment Bank tap on 13 September and mid-October, according to KangaNews data.

The shape of the SSA Kangaroo sector has likely changed in a way that will persist at least into the new year. Investor dynamics have shifted to a significant degree and, with the end of the year looming, there is as yet no clear picture of what a consistent future buyer base for Australian dollar SSA product will look like. Intermediaries say they have a degree of confidence that the sector retains its raison d’etre but exactly how this will be expressed in issuance patterns remains to be seen.

Some of the challenging conditions characterising 2022 threaten to become structural elements that require issuers and investors alike to approach the market differently. For instance, issuers have been forced to focus less on pricing than on securing liquidity, according to Craig Johnston, Sydney-based director and head of DCM syndicate at Deutsche Bank. “Successful transactions issue to where demand is and where investors are looking to pick up paper,” Johnston tells KangaNews. “Historically, Kangaroo SSA issuance typically came with margins very close to secondary marks. But there has been a slight shift away from this as issuers prioritise good volume.”

New-issue concessions are becoming a necessity, agrees Daniel Wilson, vice president, DCM Asia Pacific at RBC Capital Markets in Sydney. “A main contributing factor for the lack of recent supply was that Australian SSAs were priced so far inside global curves,” he says. “The issue here is that, while small parcels of bonds can transact in the secondary market, anything of volume needs to offer a form of new-issue concession. But this is similar to what is happening in other currencies and other markets.”

GOING SHORTER

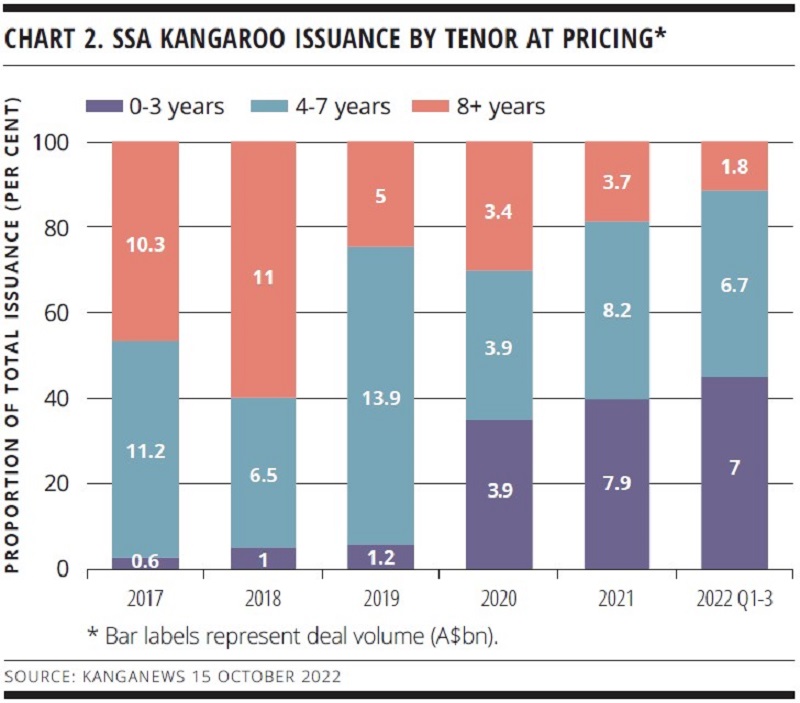

An even more significant structural change might be the tenor available to SSAs in Australian dollars. In recent years, the Kangaroo market has been able to support regular issuance at long tenor – of 10 years or more – supported in particular by the Japanese bid.

Markets globally have shortened up in 2022 and the SSA Kangaroo sector has felt the impact more than most. The trend for less duration has been simmering for several years but it has really come to the fore in 2022, when nearly half of all issuance has been in the short end (see chart 2).

Of the A$1.8 billion of long-dated paper that has priced, just A$50 million came to market after the end of May and A$1.1 billion printed in January.

“Japanese demand that was the bedrock of our 10-year demand is not there any more,” says Harald Eikeland, director, syndicate at ANZ in Sydney. “There is still a significant amount of money in Japan invested in Australian dollars and SSAs will take some of it, but not to the extent of three or four years ago.”

In particular, Eikeland does not expect 10-year demand from Japanese life insurers to return in force absent a further structural shift. On a more positive note, dealers say the offshore bid has migrated from an outright selldown to maintenance mode, which at least provides a level of underlying demand.

Some international asset managers have been active across the curve and their demand is typically longer than the three-year spot that was the focus of issuance in Q2-3, intermediaries say. The Japanese bid has not evaporated, though it is smaller and thus requires a more opportunistic issuance approach.

Nikolaus Romuld, head of high-grade origination and syndicate at Commonwealth Bank of Australia (CBA) in Sydney, tells KangaNews the Japanese selldown was almost exclusively driven by currency realignment. It meant the rest of the market needed to digest the outflows, with a consequent widening effect. But Romuld says conditions stabilised through the mid-part of the year and demand had started to creep back into the market.

On the other hand, the new shape of the curve means a return to the old normal seems unlikely. Johnston explains: “The curve has been very flat for a number of years because Japanese investors targeting longer tenor were not looking at an asset swap basis – they were buying outright yield and at times buying on what appeared a very flat curve,” he says. “We need to see the steepness of the curve normalise to incentivise investors to go longer.”

Tenor will likely remain in the 3-5 year range for the meantime. “With Japan on the sidelines, it does not feel like we are going to be looking at large 10-year transactions in the near term,” Johnston says. “Investors elsewhere will put money to work but are more cautious and are therefore being more defensive with tenor.”

One positive for the Kangaroo market is that issuers have adapted their expectations to demand. Wilson says issuers are generally happy to print where pricing and liquidity make sense. “Pre-pandemic, we would hardly have seen any three-year supply in this market; it was all 5-10 year deals,” he comments. “But issuers have adjusted their expectations to the extent that they have been willing to do three-year issuance.”

FILLING THE GAP

Dealers’ primary hope is that, as and when near-term market turmoil settles down, the SSA Kangaroo sector will adjust to the revised fundamentals with new or returning investors – and issuers – taking advantage of emerging value. There were signs of this happening in Q3. For instance, Romuld says: “Central bank investors have also been coming back into the market, although somewhat more intermittently and in more cautious sizes.”

The appeal of the asset class has re-established itself, at least. Eikeland says: “Central banks and asset managers still have plenty of reasons to buy Australian dollar SSAs, as long as domestic semi-government securities remain extremely well bid. We expect ongoing demand from high-grade buyers around the world, just maybe not at the same level.”

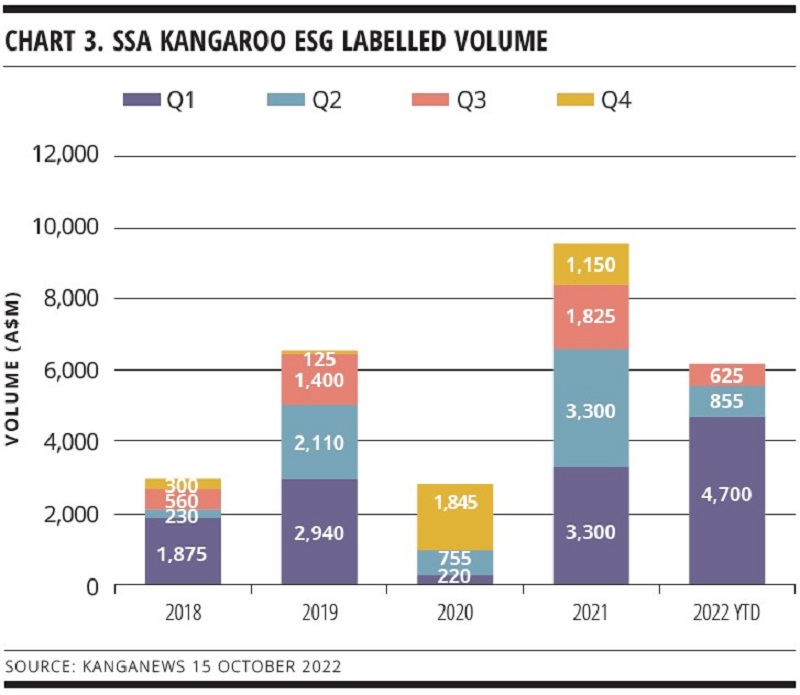

Another factor in 2022 has been the limited nature of Australian domestic demand for SSAs – which, while typically a smaller component of the total bid, might have been expected to emerge as a relative value play against local high-grade issuance. Environmental, social and governance (ESG) issuance has sparked incremental domestic demand in recent years (see chart 3).

Romuld comments: “The deals that have been coming in ESG format have definitely had wider domestic take-up, which has been quite beneficial for domestic investor engagement.”

Because issuers in the SSA sector tend to have a social purpose they also have a specific, ongoing capacity for ESG issuance, says Eikeland. “SSAs are probably the asset class that has the biggest capacity to issue ESG products, and we will see more of this in Australia as new issuers come to market,” he says.

Johnston tells KangaNews the domestic preference for sustainability-related issuance is borne out in transactions executed this year, where “deals with an ESG label were skewed more to domestic accounts than was the case for non-ESG issuance”.

The issue is that the label is not sufficient in and of itself to attract the domestic bid if other factors do not line up. Wilson describes ESG as a draw for domestic buyers but not necessarily a game changer, particularly in the context of a challenging year. “Pricing is probably the most relevant factor at the moment,” he points out. “ESG provides a fantastic label for a transaction, but it is not necessarily going to shift overall demand significantly right now.”

It is worth noting that the proportion of deals coming to market with a green, social and sustainability (GSS) label has remained robust. The A$855 million of GSS deals from SSAs in Q2 might look skinny, but it represents a large majority of the total issuance of A$1.1 billion in this period. Nonetheless, the GSS component of total SSA issuance has fallen from roughly half the total in 2021 to around one-third in Q1-3 this year.

ISSUER LANDSCAPE

The shifting dynamics that appear to have become bedded into the Kangaroo market in 2022 may also open up opportunities in Australia for a new range of borrowers from the SSA sector and beyond. In August, for example, CPP Investments – the investment arm of the Canada Pension Plan – executed its inaugural Kangaroo deal, encountering good demand for what ended up being a A$1 billion, five-year print.

“There is a market for less frequent issuers because a large driver of demand is offshore accounts that are active in other currencies,” Johnston says. “Some issuers will have books that skew more to offshore investors. They may still be able to get deals done at good size, albeit potentially with less diversification than for some of the more frequent, larger borrowers.”

Romuld agrees: “If offshore spreads remain elevated and the basis remains constructive, there is an opportunity for the smaller names to come back to this market.”

This was a phenomenon in the more conducive market conditions of the start of the year. Wilson, for instance, highlights early-year benchmark transactions from BNG Bank, Kommunalbanken Norway, NRW.BANK and L-Bank.

The lull should not spell the end of such opportunities in the longer term. Wilson says: “Demand is definitely there – it is more of a strategic decision for issuers involving how they approach the end of their funding programmes, what markets they look at and their future funding plans.”

With volatility and uncertainty remaining governing themes, market participants say the outlook for 2023 depends largely on how rate hiking cycles by the Reserve Bank of Australia (RBA) and other central banks play out. “When we get a little more clarity, particularly around what the RBA is doing and what the inflation picture looks like, we will have more confidence that the market has sufficiently priced everything in,” Romuld says. “But I do not think we are there yet.”

The terminal interest rates reached by central banks, and consequently where Australia stacks up against offshore markets, is another relevant factor. “If we peak at, say, 3 per cent while offshore rates go higher, we could end up in a situation where our spreads do not look particularly attractive,” Romuld continues. “Global investors are used to categorising Australia as a higher-yielding market but this may not continue to be the case.”

Nevertheless, there is a degree of confidence that the SSA Kangaroo market is sufficiently mature and diverse to support annual issuance ultimately to return to the A$20 million average range, and for the Australian dollar market to remain important for SSA issuers. Dealers note that the remainder of 2022 may be quiet on the issuance front as many issuers reach the end of their funding calendars, but they say there is little reason not to expect the usual pickup in issuance in Q1 2023.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

Quantum leap for Canadian provinces as Québec smashes Kangaroo record

Investor diversity, relative value and the growing status of the Australian dollar market lined up for Province of Québec as it shattered the record volume for a Canadian province Kangaroo transaction. The A$1.35 billion, 10-year print was nearly four times larger than any previous deal from the sector – a record that had stood for a decade.