Social bonds seek deeper roots in Australia

Social bonds took a step forward in prominence globally during the pandemic, but the product has never gained significant traction in Australia beyond global high-grade issuers and occasional specific-use cases. Sustainable finance experts say there is still growth potential but what these bonds should look like, what organisations should issue them and how impact is measured are all still works in progress.

Kathryn Lee Staff Writer KANGANEWS

The global green, social and sustainability (GSS) bond market has taken a step back in 2022. Climate Bonds Initiative (CBI) data show combined issuance of US$417.8 billion equivalent in H1, down 27 per cent year on year. Social bonds were the focus of the decline.

After enjoying a boom in 2020-21 as issuers – led by global supranational, sovereign and agency (SSA) names – used the social label to marshall pandemic relief funding, the vogue for social bonds appears to have passed. CBI reports a 57 per cent year-on-year decline in social-bond issuance in H1 2022 and a 13 per cent decline in supply of sustainability bonds – which combine social and green use of proceeds (UOP). Unlike green bonds, CBI reports, social issuance did not rebound in Q2.

In this case, the global experience is not reflected in Australia – largely because there was no pandemic-related boost to social-bond issuance in the first place. It is true that social-bond supply increased during the pandemic period and that SSAs provided the bulk of volume. But the step-up came in 2021 rather than 2020, and the biggest year for sustainability-bond issuance is 2019.

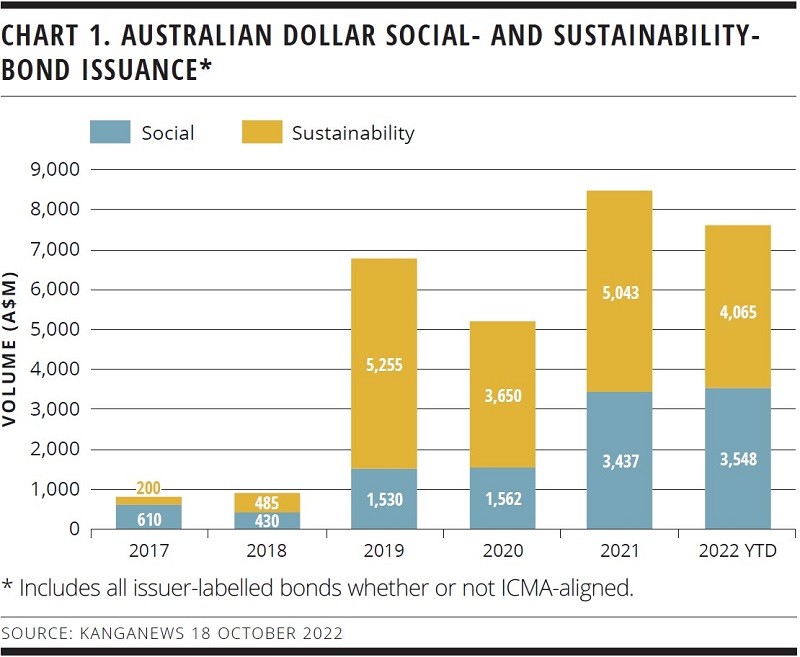

With no COVID-19 peak to match, social and sustainability bond issuance is close to a record in 2022. KangaNews data show more than A$7.6 billion (US$4.8 billion) of combined issuance in 2022 by mid-October, chasing a full-year record of just less than A$8.5 billion from the preceding year (see chart 1). Aggregate annual issuance has increased each year, even in 2022 when market conditions have been difficult.

One notable breakthrough is that the Australian securitisation market unlocked the social label in 2022. In June, Pepper Money priced its first all-social residential mortgage-backed securities (RMBS) transaction and industry peer Resimac also included a social tranche in an RMBS two weeks earlier.

But the fact remains that use of the social and sustainability labels remains relatively narrow in Australia. Global SSAs have been by far the biggest issuers, accounting for more than two-thirds of the A$30 billion of aggregate supply (see chart 2).

Two local semi-government names – National Housing Finance and Investment Corporation (NHFIC) and TCorp (New South Wales Treasury Corporation) – add another sixth of the market, leaving just A$4 billion of supply, all time, from all other issuers including the entire local bank and corporate sectors. Of the nine issuers that have raised more than A$1 billion, all but one comes from the domestic or global high-grade sector (see table).

Top 10 Australian dollar social and sustainability bond isuers by volume

| Issuer | Debut deal pricing date | Social bond issuance (A$m) | Sustainability bond issuance (A$m) | Total issued (A$m) | Total outstanding (A$m) | Total lines issued | Lines outstanding |

|---|---|---|---|---|---|---|---|

| World Bank | 23 Aug 18 | None | 5,760 | 5,760 | 5,600 | 6 | 5 |

| TCorp | 14 Nov 19 | None | 3,300 | 3,300 | 3,300 | 2 | 2 |

| Asian Development Bank | 22 Apr 21 | 2,600 | None | 2,600 | 2,600 | 3 | 3 |

| Treasury Corporation of Victoria | 16 Sep 21 | None | 2,500 | 2,500 | 2,500 | 1 | 1 |

| National Housing Finance and Investment Corporation | 21 Mar 19 | 1,787 | 408 | 2,195 | 2,195 | 5 | 5 |

| European Investment Bank | 12 May 20 | None | 1,950 | 1,950 | 1,950 | 2 | 2 |

| International Finance Corporation | 6 Mar 18 | 1,700 | None | 1,700 | 1,700 | 2 | 2 |

| ANZ Banking Group | 18 Aug 20 | None | 1,250 | 1,250 | 1,250 | 1 | 1 |

| Asian Infrastructure Investment Bank | 28 Apr 21 | None | 1,250 | 1,250 | 1,250 | 3 | 3 |

| African Development Bank | 20 Sep 17 | 995 | None | 995 | 995 | 4 | 4 |

Source: KangaNews 18 October 2022

SOCIAL ASSETS

Part of the reason why adoption has not been wider is that the market still does not appear to have a fully-formed consensus on what makes an asset or project worthy of inclusion in a social UOP transaction. Green bonds, by contrast, generally have well-established metrics. These are inherently harder to deliver in a social context.

In the case of Pepper Money’s transaction, even a second-party opinion (SPO) from ISS ESG to show alignment between the deal and the International Capital Market Association (ICMA) Social Bond Principles (SPBs) was not enough to convince some investors of the transaction’s credibility.

The central reservation for investors sceptical of Pepper Money’s transaction was the concept of additionality – the idea that social bonds should provide financing that leads to outcomes that would not have happened otherwise.

At the heart of the Pepper Money social RMBS’s rationale is the idea that the company is lending to borrowers who would not otherwise have access to housing finance, and therefore making home ownership available to a cohort that would not otherwise have this option. The objection some investors raised was that – as Pepper Money is proud to acknowledge – this type of lending is its business model. The suggestion is that labelled social funding does not promote superior outcomes.

On the other hand, some investors were prepared to back the deal on the basis that it provides a step on the path of asset-class evolution. Following the transaction, for example, Victoria Gao, then a Sydney-based fixed-income portfolio manager at CIP Asset Management, told KangaNews: “We hope this transaction starts a market discussion about how we want social-bond frameworks to look. There needs to be market consistency, and we are in the early stages of developing it.”

Additionality is just one of a clutch of challenges for the social-bond label. For one thing, the SBPs include several eligible project categories, each of which is open to a variety of possible social indicators. This can put investors into unfamiliar territory. Not only do green bonds have more precedents to follow, but their metrics are also tied to obvious quantitative data points – such as science-backed carbon emission reduction targets.

“Investors can understand environmental impacts and outcomes from green UOP and how they avoid or reduce emissions,” says David Jenkins, global head of sustainable finance at National Australia Bank (NAB) in Sydney. “Social UOP and outcomes are more subjective, unless we are talking about public-sector investment in specific social infrastructure and projects with clear social impacts – such as education, hospitals, and subsidised or affordable housing.”

“There are so many things that can be mapped and targeted – for instance poverty, zero hunger or basic infrastructure. But because there are so many, we have to ask what issuers are actually reporting on and what data they are able to produce. It is one thing to develop a social-bond structure, but the reporting is key.”

There are geographic differences, too: what counts as social in one jurisdiction might not do so in another. During an ICMA podcast in July, Begum Gursoy, Amsterdam-based technical head of debt capital markets and sustainable finance EMEA at Sustainalytics, explained the extra complication this causes for social bonds.

“On the green-bond side there are well-accepted standards that can be applied globally, mainly due to the presence of global decarbonisation trajectories and climate change commitments,” she said. “However, the credibility and impact of social bonds relies on where the projects are being financed. All jurisdictions come with different social challenges and realities. What is socially impactful in South East Asia might not be in the Nordic region. The nature of social bonds makes the market very dynamic; the context changes and is affected by socioeconomic conditions on a day-to-day basis.”

Not only does a lack of standardisation make social bonds more difficult to compare, but it is also holding back reporting outcomes. Gavin Goodhand, senior portfolio manager at Altius Asset Management in Sydney, says every fund manager, particularly in the institutional market, wants to see a tangible outcome from any investment that claims to be social. But the amount of data to work through to make this critical assessment makes it difficult.

He tells KangaNews: “There are so many things that can be mapped and targeted – for instance poverty, zero hunger or basic infrastructure. But because there are so many, we have to ask what issuers are actually reporting on and what data they are able to produce. It is one thing to develop a social-bond structure, but the reporting is key. At the moment, I know of no standardised metrics for reporting in the space, though firms do try to align to frameworks such as the UN Sustainable Development Goals [SDGs].”

Goodhand regards NHFIC as a leader in the Australian social-bond market because of its line-by-line approach to reporting what community housing providers the agency has funded (see box). But affordable housing is just one SBP project category, and even in this case there is still room for more data and impact assessment. “Housing has been provided – but what are the longer-term benefits? Has it led to reduced unemployment or improved educational outcomes for families? These are all longitudinal studies that need to be done, but it is probably a little too early to be able to derive them,” Goodhand explains. “Over time, we want to see a deeper level of reporting: not just case studies but a further dive into the outcomes for the community or society as a result of [the social UOP] borrowing.”

Greg Thong, director, sustainable finance solutions a Sustainalytics in Sydney, agrees quantifiable metrics are the gold standard, adding that they also help reduce the risk of socialwashing. “We like measurements because they clearly demonstrate what the proceeds are going toward and the impact of this,” he says. “Social issuance may be more exposed to socialwashing than green bonds are to greenwashing, and it is a greater risk to investors.”

Community housing’s growth potential

Market users say National Housing Finance and Investment Corporation (NHFIC) provides a benchmark for social use-of-proceeds (UOP) issuance in Australia. Mark Russell-Jones, NHFIC’s Sydney-based director, treasury and capital markets, explains the agency’s mission, its drive to increase reporting standards and the government’s plans to scale up the community housing sector.

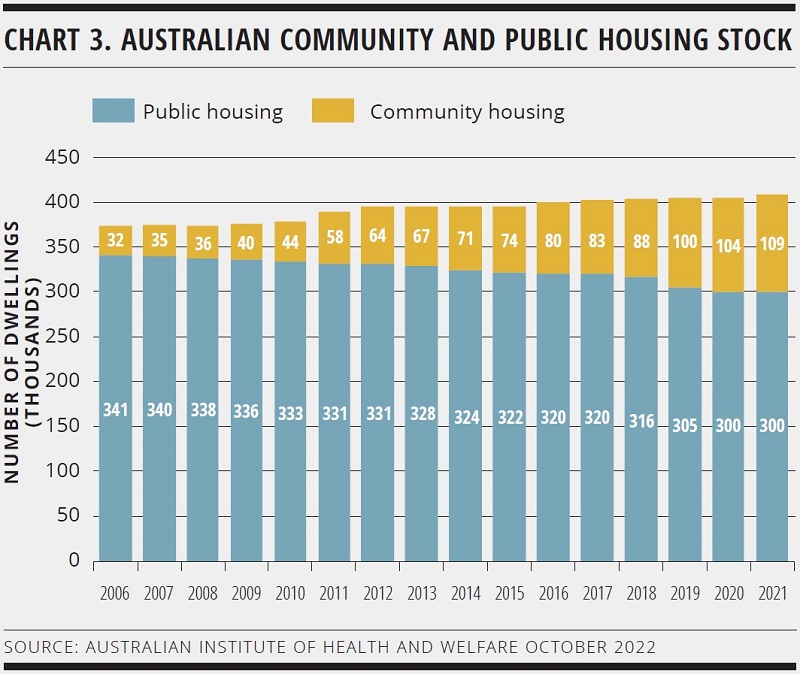

Community housing in Australia is undergoing a rapid growth drive. In June 2021, community housing providers (CHPs) owned one-quarter of the dwellings in the public housing sector – up from less than one-tenth 15 years previously (see chart 3).

While the number of community housing dwellings more than tripled between 2006 and 2021, public housing stock reduced by more than 40,000 dwellings during the same period.

Russell-Jones says the shortfall of social and affordable housing in Australia is creating an opportunity for CHPs to play a larger role in the residential housing market. This is also the case in certain European countries, such as the UK and the Netherlands. Housing associations in the Netherlands manage approximately 2.3 million rental homes or around 29 per cent of Dutch housing stock.

SETTING STANDARDS

The complications of defining and measuring social impact are sufficiently great that the EU – generally the pace setter in sustainable finance – appears to have put its social taxonomy plans on hold. Many market users had hoped the development of the taxonomy would help give clarity to the sector and thus drive growth.

The European Commission has not made an official statement on the move. However, on 31 July, Bloomberg reported it had been “shelved indefinitely”. The commission had previously intended to begin its debate on what the social taxonomy could look like before the end of its term in 2024, but this now seems unlikely.

The EC had also been due to publish an outline of the social taxonomy roadmap by the end of 2021 but it was never delivered, further fuelling the belief that the whole project has been parked. Jenkins explains: “It was meant to be the next cab off the rank and there has been a significant focus on implementing the EU taxonomy. But the situation in Ukraine and the energy crisis mean the EC has not been able to get sufficient support and agreement on priority areas.”

An EU social taxonomy would sit within the wider EU legislative environment on sustainable finance and governance, which includes the existing green taxonomy. Jenkins points out that the first taxonomy took several years to work out but was eventually delivered, despite disagreements on the way and ongoing debate about the inclusion of nuclear and gas as transition fuels.

Marie-Bénédicte Beaudoin, head of second-party opinion operations at ISS ESG in Paris, says not seeing the EU taxonomy develop as planned will to some extent hinder social issuance by denying it potentially useful infrastructure. But she believes the sector should continue to develop even in its absence.

“While the EU social taxonomy could have been an additional driver and a means to structure and qualify supply, issuers have embarked on this journey for some time already,” Beaudoin tells KangaNews. “With social challenges emerging across geographies – for example the cost of living, access to finance, cost of education and potential job cuts as consequences of the current inflation and increase of interest rates – there could be further developments in the social-bond market in the coming year.”

However, Jenkins adds it is not inconceivable that some European investors may choose to stay out of or limit exposure to social bonds until an EU taxonomy is in place. “One could argue the uncertainty on what will and what won’t be included is one reason investors haven’t flocked to social bonds,” he says.

The Australian Institute of Sustainable Finance (ASFI) will have to grapple with the same issue as it embarks on its own taxonomy. On 17 October, however, ASFI strongly hinted that the local taxonomy will stay clear of social aspects in its early iterations. Having studied a dozen international taxonomies, the institute concluded: “There were many challenges associated with attempting to apply social and governance criteria. Fundamental difficulties of usability, compliance costs, lack of available data and incomparability across jurisdictions were identified as key barriers to effective implementation.”

The context for this challenging environment for top-down guidance on social finance is growing concern about greenwashing risk in the environmental finance space. It could be argued that enhanced greenwashing risk goes hand in hand with a more formalised market – that the existence of things like the EU taxonomy in effect provide clearer guidelines that entities can fall foul of. In this case, the social sector’s lack of taxonomies and the like might actually reduce socialwashing risk.

However, most market users suggest the rising green tide is lifting all boats – including social. This seems to chime with the Pepper Money experience, where at least some investors were willing to make judgement calls on the UOP even in the absence of established scoring practices.

It also implies a dual challenge for potential social issuers: the market is more watchful than ever for perceived greenwashing and socialwashing, but unlike in the green sector there are few parameters that can be used to allay the risk. “A number of European funds are finding they can’t deliver on the EU Sustainable Finance Disclosure Regulation reporting requirements for Article 9 funds,” says Jenkins. “In this context, what has happened with the social taxonomy creates more challenges.”

FUTURE GROWTH

Even so, Australian sustainable finance experts have some confidence that social UOP issuance will continue to deliver at least steady growth. No Australian true corporate issuer has executed a social-bond deal, but this year there have been two Australian dollar social loans. This suggests there is an asset base that can be applied to social UOP debt.

In July, APM Human Services International executed Australia’s first social loan, an A$840 million facility. Opal Healthcare followed in September, with its A$800 million social loan becoming the first in the Australian aged care sector.

NBN Co has issued green bonds and laid the groundwork for social use of proceeds in its sustainability financing framework. The framework states the company would issue under the SBP categories of access to essential services, and socioeconomic advancement and empowerment. The project itself would help connect under-served regional and remote communities to the broadband network.

The quietest sector for GSS issuance in Australia has been financial institutions. The local major banks made some of the first strides in green-bond issuance and also printed some of the first social bonds locally, but momentum and consistent supply have not eventuated. NAB printed Australia’s first social bond, in 2017, while ANZ Banking Group priced a tier-two bond aligned with the SDGs – which included social assets – in 2020. Neither bank has returned to the domestic social-bond market, though ANZ has issued SDG bonds in Europe. Virtually all the balance of financial institution social- and sustainability-bond issuance in Australian dollars has come from Korean banks in the Kangaroo market.

Jenkins says NAB’s focus has been environmentally focused lending, given the size of its balance sheet exposure and commitments. However, he adds that the internal systems and processes work the bank has completed to adequately tag green assets also carries over to the social space. “It was previously quite a manual process but we have been able to streamline, automate and simplify it.”

There is also potential for more issuance in the securitisation sector as Jenkins believes other nonbanks will pursue social RMBS. “There is a lot of opportunity in securitisation: it is about identifying eligible collateral, ensuring the tagging is in place and robust, getting comfortable with the ability to identify social outcomes and impacts and then being able to track and report on them for investors – with the awareness that global investor reporting and disclosure expectations are rising over time.”

The most natural growth channel is probably domestic semi-governments, though market participants say social assets are most likely to be used in combined sustainability UOP instruments rather than pure social bonds. Treasury Corporation of Victoria (TCV) and TCorp (NSW Treasury Corporation) have issued sustainability bonds while, in early October, Western Australia Treasury Corporation announced plans for a debut green or sustainability bond. Queensland Treasury Corporation’s sustainability-aligned debt has all been in green format so far, but Jenkins sees no reason why any semi-government issuer could not join TCV and TCorp by issuing sustainability bonds.

“Combining green and social provides the maximum issuance opportunity and the best possible liquidity,” he says. “Investors also understand UOP and impact metrics, and can make assessments very easily. Social bonds are still more subjective in comparison, in the sense of how an investor assesses and measures positive social outcomes to get comfortable.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.