Orange is the new green: latest ESG label aims to spearhead gender-focused investment

Impact Investment Exchange (IIX)’s most recent issue, a US$50 million orange bond, is a first for the global debt capital markets. IIX and ANZ – a lead on the transaction – hope the new label will help spearhead intentional and robust investment with a gender lens.

Sustainability-aligned debt has embraced gender-based targets and projects for some time, but orange bonds – a newly launched asset class – are a unique spin. In the same way as blue bonds support and bring focus to marine and ocean-based projects, but could technically be labelled green, deal participants hope orange bonds will do the same for gender equality.

The bond is the asset class’s first use-case and follows the launch of the Orange Bond Principles (OBPs) in October 2022. The OBPs are named after the colour of UN’s fifth sustainable development goal (SDG) – to achieve gender equality and empower all women and girls – and were created by the Orange Bond Initiative, which is a global coalition formed to help mobilise new sources of capital for women’s empowerment.

The initiative’s steering committee includes the issuer of the orange bond – Singapore-based Impact Investment Exchange (IIX) – ANZ, the Australian Department of Foreign Affairs and Trade, the US International Development Finance Corporation, the United Nations Capital Development Fund, Water.org, Shearman & Sterling and Nuveen.

The US$50 million deal is IIX’s fifth issue in its Women’s Livelihood Bond (WLB) series and is structured as a securitisation, with the underlying collateral a portfolio of loans IIX has made to high-impact enterprises based in Kenya, India, Indonesia, Cambodia and the Philippines that qualify and are deemed to have a positive impact on women’s livelihoods. The loans span five sectors: sustainable agriculture, affordable housing, water and sanitation, clean energy and SME-lending and microfinance institutions.

"The transaction takes a traditional finance structure – with a first-loss, subordinated tranche as well as credit enhancement in the form of guarantees from development agencies – and directly applies this to the underserved population itself. Rather than microfinance companies individually going investors to try and get a small amount of money at a time, it allows us to scale up and mobilise capital in a meaningful way.”

The loans also carry a 50 per cent credit guarantee from the US International Development Finance Corporation and the Swedish International Development Cooperation Agency. This adds an extra layer of protection for investors in addition to the securitised structure.

Of the two tranches, only the US$45 million senior tranche was available to investors while IIX’s Women’s Catalyst Fund covered the US$5 million subordinated first-loss piece. Investors will earn a 6.5 per cent semi-annual return on the notes across a four-year tenor, with the principal repaid as a bullet repayment.

Sarah Ng, director, debt capital markets at ANZ in Singapore, says the aim of the transaction was to create a way to give high-impact enterprises access to international capital markets. “The transaction takes a traditional finance structure – with a first-loss, subordinated tranche as well as credit enhancement in the form of guarantees from development agencies – and directly applies this to the underserved population itself,” she comments. “Rather than microfinance companies individually going investors to try and get a small amount of money at a time, it allows us to scale up and mobilise capital in a meaningful way.”

Alongside this, the orange label brings an additional layer of rigour to gender-focused investment. Mara Chiorean, sustainable finance director at ANZ in Singapore, explains that the intention of the initiative is not to reinvent the social asset class, but to give it focus when tackling gender issues specifically. The steering committee hopes the increased attention and clearer standards the OBPs convey will help attract US$10 billion to the sector by 2030.

“The green bond market started with a handful of pioneers who decided to look at how to do climate-related bonds in a more structured way,” she says. “Many social bonds list gender as one of the objectives, whether or not it is the sole purpose of the bond. As the market continues to develop, we wanted to give transactions targeting gender projects more rigour and structure. The aim is to give investors confidence that if a bond is labelled orange, it is tackling gender issues at its core.”

This issue is particularly pressing, Chiorean continues, given how far off the world is in achieving the 2030 milestone for the fifth SDG. “We are running out of time, so it makes sense to pick gender as an issue to really get behind and support over the next seven years,” she comments. “According to the UN’s latest report, women only have a 20 per cent representation in national governments and as of 2019 women’s representation in the workforce is only around 35 per cent.”

But this is not to say financing should be pulled away from climate. Those involved in the Orange Bond Initiative say it is possible to work on these issues concurrently, and they can even complement each other. “If you leave women out of the equation, you are literally cutting out half of humanity, and to solve for climate mitigation and adaptation, I think it’s imperative to have the full force of humanity,” notes Natasha Garcha, senior director, innovative finance and gender-lens investing specialist at IIX in Singapore.

“Additionally, gender and climate are emerging as ways to stabilise and de-risk a portfolio. When you look at the microfinance industry, women also tend to be better borrowers: this gives orange bonds an edge.”

Garcha adds that solving gender issues can also have positive effects on the social and political fabric of a community and can help repair some of the economic damage from the pandemic, adding to the relevance of the asset class in today’s world.

“Women may not be the main combatants of wars, but they are often the main victims. On the other side of this, research shows that peace agreements have a 35 per cent better chance of lasting for at least 15 years when women are involved,” she says. “There is also so much research to show that one of the greatest predictors of the peacefulness of a state is the gender equality of its leadership: Australia and New Zealand are great examples. Additionally, during the pandemic, women were 1.8 times more likely to drop out of the workforce to do unpaid care. Reintegrating them could add US$13 billion to global GDP.”

IMPACT DEMAND

The orange bond is IIX’s largest-volume transaction in the WLB series. Garcha says this helped it to garner more institutional involvement compared with earlier issues, which were smaller and dominated by family offices and private banks.

“It has been so wonderful to see the growth in our investor base,” she tells KangaNews. “Nuveen is one of the largest sustainable debt investors in the world and has anchored our last four bonds. It’s nice to see very large institutional investors looking through the gender lens and investing in an asset class like orange bonds, which we hope will help cut through green and impact washing concerns in the social bond space.”

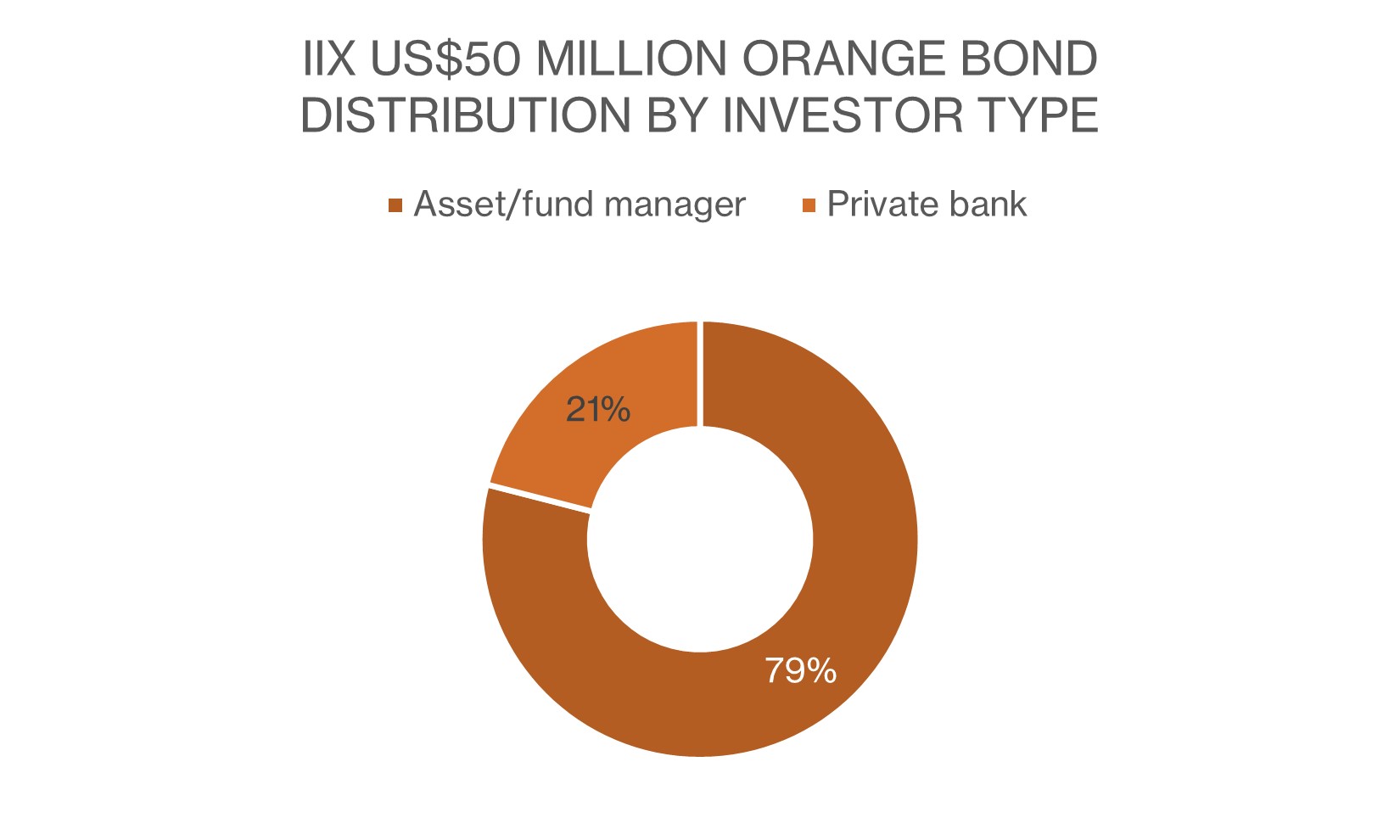

Fund and asset managers dominated the deal, with the remainder bought by private banks (see chart). While IIX has not disclosed the geographic distribution, KangaNews understands the deal included accounts from Europe, the US, Australia, New Zealand, Norway, Singapore and Hong Kong, among other locations.

Source: ANZ 22 December 2022

Ng highlights that Australian and New Zealand impact-focused investors showed particularly strong interest. “Australian and New Zealand investors were the first movers to focus on ESG across the Asia Pacific. For example, we have worked with Pathfinder from New Zealand in a number of IIX’s women’s livelihood transactions, and they have been very receptive,” she says. “We’re finding that impact funds are becoming increasingly willing to look at transactions like this, and to spend the time needed to get to grips with the structure. They understand the real impact this type of bond makes.”

Garcha adds that investors are also impressed with the geographic and sector diversity of the WLB series. She says this influenced some European-based microfinance investors to join the programme. “They like the gender angle but don’t want to be limited to just one space, which makes our transaction appealing” she comments.

Being the fifth issue in the programme also added some influence, Garcha continues. The bonds have a good track record, with no cases of default or delays to the coupon payment. “Even during the COVID-19 pandemic, our loans were to priority sectors that were protected by the government. The companies continued to perform in a relatively stable way,” she says.

"The green bond market started with a handful of pioneers who decided to look at how to do climate-related bonds in a more structured way. Many social bonds list gender as one of the objectives, whether or not it is the sole purpose of the bond. As the market continues to develop, we wanted to give transactions targeting gender projects more rigour and structure. The aim is to give investors confidence that if a bond is labelled orange, it is tackling gender issues at its core.”

ORANGE STANDARDS

To be considered an orange bond, a transaction must align with all three OBPs (see table). For principles one and two, the issuer must also outline the subpoints the deal aligns with, whereas for principle three – which advocates for transparency in the investment process and reporting – they need to demonstrate alignment with all three subpoints.

Orange Bond Principles

| Principle | Description | Subpoints |

|---|---|---|

| Gender-positive capital allocation | Issuers (including governments, quasi-governments, corporates, financial institutions, and impact investing firms) are expected to use the proceeds of the orange bonds to advance gender equality in one or more of the following ways [outlined in the subpoints], taking into account the needs of the region or target population. |

1a. Financing the development and/or provision of products and/or services that substantially and disproportionately benefit women, girls, or gender minorities including the LGBTQI+ community and other groups facing gender-based and intersectional discrimination. |

| 1b. Financing projects or enterprises with a substantially gender diverse and equitable workforce, and/or gender-inclusive value chains, that ensure gender-pay equity and equal workplace and employment-related rights to all regardless of gender identity. | ||

| 1c. Financing enterprises or organisations that are founded by, are majority (i.e. >50%) owned by or whose senior leadership (e.g., C-suite executives, key decision makers, and/or heads of departments) have >30% women or gender minorities. | ||

| 1d. Financing other ESG or SDG-aligned projects or initiatives that are intentionally designed to substantially and disproportionately have a positive net impact on women, girls or gender minorities. | ||

| Gender-lens capacity and diversity in leadership | In order to demonstrate they have capacity within their own organisations to integrate a gender-lens into the investment decision-making process, as well as to align with Orange Bond Initiative’s commitment to diversity and inclusion, issuers of orange bonds are expected to satisfy one or more of the [subpoints]. | 2a. Over 30% of the leadership team (e.g., the board, the officers, and/or the investment committee) are women and/or gender minorities. |

| 2b. Over 30% of the team working on the core functions of the orange bond (e.g., structuring, due diligence, portfolio management, investor relations, and/or reporting) are women and/or gender minorities. | ||

| 2c. The leadership team and/or team working on the core functions of the orange bond includes women and/or gender minorities from the same ethnicity as the target population in one or more regions where proceeds of the orange bonds will be allocated. | ||

| Transparency in the investment process and reporting | Issuers are expected to take a data-driven, bottom-up and verifiable approach to ensure gender-transformative impact is adequately measured, managed, and magnified, by adopting each of the [subpoints]. |

3a. Transparency in investment process – to ensure a continued gender-lens approach is adopted in line with Principles 1 and 2, providing investors with an upfront framework at the time of the issuance of the orange bonds on: |

| 3b. Transparency in impact measurement – during the life of the orange bonds, conducting an annual confirmation of the impact (output, outcomes, impact) achieved by the bonds through interviews, surveys, or other means of collecting data directly from a sample size of the target population of the bond’s proceeds (i.e., women, girls, gender minorities, or other individuals experiencing gender equality related outcomes or impact). | ||

|

3c. Transparency in reporting – during the life of the orange bonds, providing investors with annual reports on: |

Source: Orange Bond Principles October 2022

The principles also encourage issuers to seek an external review or second party opinion (SPO) and to report on alignment with other industry standards, such as the International Capital Market Association’s Social or Green Bond Principles, though it is not mandatory.

In IIX’s case, the transaction has an Impact Framework and SPO from IIX Global Charitable Limited – a separately registered Singapore-based charity – that confirms alignment with the Orange Bond Principles. The SPO also notes alignment with ICMA’s Sustainability Bond Guidelines, the ASEAN Capital Market Forum’s Social Bond Standards, the Sustainable Development Goal Impact Standards for Bond Issuers, and the 2X Challenge Criteria.

Garcha acknowledges that securing an SPO from a sister entity may raise concerns, but says it was the best candidate for the job based on its experience in impact reporting and is truly independent from the borrower.

“When we spoke to other organisations that do SPOs, we found no-one was interviewing the women themselves,” she says. “IIX Charitable had the technology and track record of interviewing women. Our investors would rather hear from the women who benefit from the transaction than have us pay a third-party consultant.”

Additionally, Garcha says IIX’s historic partnership with the UN for previous transactions under the WLB series adds an extra layer of credibility, as well as the fact that the loans include a credit guarantee from development agencies. She adds that these organisations have all conducted third-party assessments against their own standards.

An interesting aspect of the OBPs is that the second principle shines a light on the issuer of the bond itself. This is unlike the ICMA Social Bond Principles, for example – where the 2021 edition recommends “heightened transparency for issuer-level sustainability strategies and commitments,” but does not include it as a requirement within the four core components.

“The Orange Bond Principles look at who is making the investment decisions,” Garcha explains. “Are there women there who can bring their own gender lens to the transaction? So many gender bonds have no women on the investment committee, structuring team, or involved in the reporting.”

For IIX, this meant considering the target population of the project and including women who represent these regions. “Having women involved is great, but also having women from these regions brings a different perspective,” Garcha continues. “Women of colour look at things differently because they have experienced different forms of gender-based discrimination. We made sure to have a woman from Kenya involved in the Kenyan entities. Equally, women from Southeast Asia looked at the Southeast Asia entities.”

BUILDING MOMENTUM

Growing the orange bond market to US$10 billion by 2030 might seem like a lofty ambition considering there has only been one transaction, but Garcha is confident it will happen.

“In 2021, the sustainable debt market crossed the US$1 trillion mark, so in this context I think the goal is very achievable. But it will require clear parameters and careful distinction about what this asset class is trying to do – something green bonds did very effectively,” she says. “We expect more orange bonds will come, that’s why we put the principles out there. Anyone can issue an orange bond, so long as they comply.”

Ng agrees there is huge potential for an orange bond market. She hopes to see the asset class as an industry-wide initiative, rather than something specific to the WLB series.

“This transaction was a good example, because we knew we could present it as best practice for what an orange bond can look like,” she tells KangaNews. “But we are also speaking to other issuers about how they can apply the Orange Bond Principles to their own transactions.”

Ng would also like to see multisector participation, rather than the asset class being confined to financial institutions and development banks – the usual territory for gender bonds. “With this in mind, the Orange Bond Principles have been developed to allow for broad applicability, but also rigorous criteria to ensure the market maintains best practice,” she comments.