ASIC turns the screws on greenwashing in enforcement push

Increased engagement with sustainability is leading to growing awareness of greenwashing risk – the potential for environmental credentials to be overstated or misrepresented. The Australian Securities and Investments Commission is prioritising greenwashing surveillance and enforcement, supported for the first time by a more coherent policy backdrop.

Laurence Davison Head of Content KANGANEWS

Dan O'Leary Deputy Editor KANGANEWS

While market participants acknowledge the need for sustainability claims to be policed, there is also some concern that added scrutiny could increase reputational risk and make entities less willing to pursue ambitious sustainability goals.

The Australian Securities and Investments Commission (ASIC) has stepped up enforcement of misconduct related to greenwashing following a pledge to crackdown on the practice in 2022. Most recently, the regulator took Mercer Superannuation to court in late February, accusing the company of misleading its members on the sustainability of its investments.

This is the first time ASIC has used the courts to pursue alleged greenwashing misconduct. The court action follows the publication of several enforcement notices in late 2022 and early 2023 aimed at a range of financial and energy companies. Vanguard and superannuation trustee Diversa were among those fined for alleged greenwashing, but there has only been one legal claim so far.

On 10 May this year, ASIC published a report providing information about 35 “interventions” it made as part of its greenwashing surveillance activities between 1 July 2022 and 31 March 2023. These interventions resulted in 23 corrective disclosure outcomes, 11 infringement notices and, in one case, the commencement of civil penalty proceedings: the Mercer case.

At the heart of ASIC’s enforcements is a simple notion: that the alleged perpetrators had overpromised and underdelivered on their environmental, social and governance (ESG) commitments. The main problems identified by the 35 interventions are net zero statements with no reasonable basis or that are factually incorrect, terms like “carbon neutral”, “clean” and “green” being used without reasonable grounds to do so, overstated or inconsistently applied scope of sustainability investment screens and inaccurate or vague labelling.

Marita Hogan, senior executive leader and leader of greenwashing enforcement actions at ASIC in Melbourne, tells KangaNews the regulator intends greater scrutiny of ESG financial products to enhance the market’s conduct and credibility by “actively raising the profile of this area”.

In a May speech at Responsible Investment Association Australasia (RIAA)’s annual conference, ASIC’s deputy chair, Karen Chester, laid out a three-part “antidote” to greenwashing. This comprises transparency – through “disclosures that comply with today’s law and ultimately a quality, global baseline for sustainability-related disclosure standards”, policy-installed “bright lines” to support disclosure, and the work of regulators.

“Unless product issuers are true to their word regarding their green credentials, we are not going to achieve the climate change targets government and others are setting. This is an overarching principle, so having some rigour and accountability by taking enforcement action is important for the sector.”

Enhanced reporting standards will be a key plank of ASIC’s approach. In her RIAA speech, Chester endorsed the proposed shift to mandatory climate change-related disclosure in Australia and the development of international disclosure best practice under the International Sustainability Standards Board. She also highlighted the new federal government’s policy platform, including the promised comprehensive sustainable finance strategy.

“Taken collectively, these policy initiatives will provide the ‘bright lines’ to afford greater comparability in climate-related financial disclosure and, over time, sustainability issues more generally,” Chester said. “Taken collectively they will also, over time, prove to be a broad antidote to greenwashing.”

ASIC’s role is to provide the monitoring and enforcement function of the evolving regime. Hogan comments: “Unless product issuers are true to their word regarding their green credentials, we are not going to achieve the climate change targets government and others are setting. This is an overarching principle, so having some rigour and accountability by taking enforcement action is important for the sector.”

Having a joined-up policy backdrop is critical, however. While emphasising that ASIC’s regulatory action will continue, Chester added: “Over the long term, case-by-case intervention is not a cost-effective nor comprehensive antidote to greenwashing. We are therefore active in supporting Treasury in these policy developments to support increased transparency and trust across the system.”

INDUSTRY RESPONSE

David Gallagher, head of Australian fixed income at Artesian Capital Management in Sydney, agrees that added scrutiny is good for the market and in particular for firms, like Artesian, that are confident of being “rock solid on our processes”. On the other hand, Gallagher suggests, across the industry “there is some dead weight that needs to be shaken out.”

Gallagher says greenwashing hurts the market as a whole, though he also notes that many funds and issuers are now working to ensure their goals are in line with marketing material. “This is not just a local issue. The same is also happening internationally – regulation was behind and now it is playing catch up and flushing out the weeds,” he continues. “The legitimate players will be left and the market will be stronger for it.”

Gallagher believes, however, that extra scrutiny and reputational risk could dissuade borrowers from using instruments like use-of-proceeds (UOP) bonds. “Even some of the legitimate issuers may just decide a vanilla deal is fine – though I hope this is a short-term negative for a long-term positive.”

Charlotte Plaisant Millecamps, director, sustainable capital markets at Westpac Institutional Bank in Sydney, is more optimistic about the corporate response. She says: “Investors have also increased their scrutiny and this might have a more immediate impact on issuance than the actions taken by regulators so far. Borrowers have slowed their green, social and sustainability (GSS) issuance due to the added scrutiny, but this is a good thing. I believe deals will be stronger thanks to the extra consideration and the market overall will evolve further.”

Plaisant Millecamps is hopeful that corporate UOP and sustainability-linked issuance will rebound to the 2021 level this year should overall issuance pick up. She tells KangaNews that while borrowers are more cautious, they are still interested in GSS issuance.

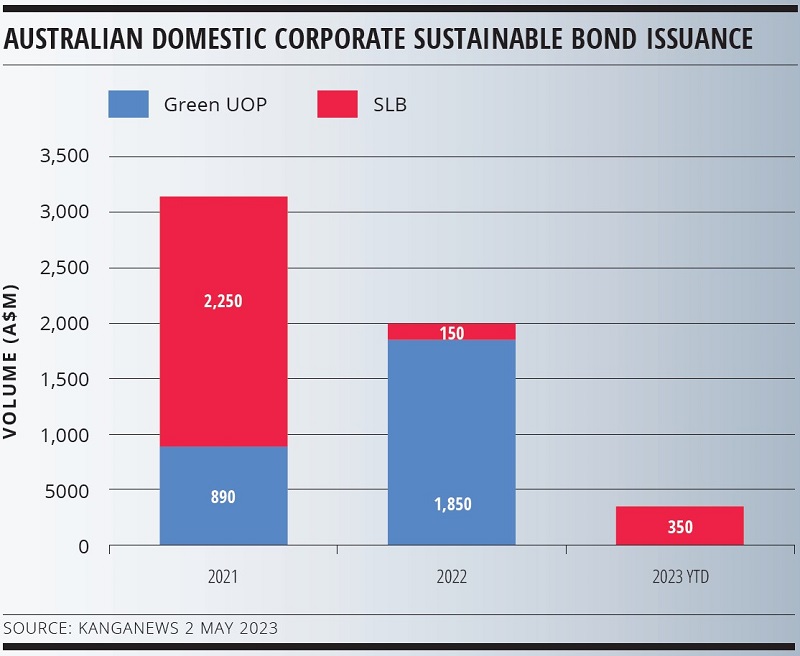

About A$3.1 billion (US$2.1 billion) of Australian corporate sustainability-labelled deals came to market in 2021 including a mix of UOP and linked structures (see chart). While 2022 started strong, a general slump in corporate issuance negatively affected GSS volume with only A$2 billion priced. Supply has yet to rebound in 2023.

It is clear, though, that at least some issuers are questioning whether the benefit of labelled issuance outweighs the potential for added compliance burdens and regulatory scrutiny.

“UOP issuance is likely to remain attractive among borrowers, particularly for those with a solid pipeline of green investment,” says Michael Momdjian, general manager, treasury, tax and insurance at Sydney Airport. “It is difficult to say the same for sustainability-linked issuance, as the continued evolution of standards and investor expectations is generating headwinds that will likely slow activity.”

Sydney Airport executed a US dollar denominated sustainability-linked bond in the US private placement market in February 2020 and has also issued in the sustainability-linked loan market. Momdjian notes product evolution, though. “The bar for borrowers is now much higher. Execution risk at the time of issuance and reputation risk post issuance may have elevated to unappetising heights for some.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.