Steps up in Worley’s SLB ambition and Australian corporate reopening

Worley revived a deal process it initiated in 2022 to debut in the Australian dollar market with a sustainability-linked bond. Issuer and leads say the transaction – which attracted a primarily domestic investor base – demonstrates the underlying robustness of risk appetite in the local credit market, while also allowing the issuer to enhance its own sustainability targets.

Worley first engaged investors on a potential first transaction in the Australian dollar primary market in September last year, when the it began sounding buy-side interest in a sustainability-linked bond (SLB). This issuer elected not to green-light a deal at that time, however – and suggests its confidence to execute in April 2023 points to a more conducive market despite recent risk events.

The feedback last year was that investors were reluctant to add more risk to portfolios than they needed to, which, given its sound liquidity position, gave Worley reason to pause.

“We weren’t comfortable with the level of market volatility at the time so chose to put down our pens down and re-engage with the investor community after our half-year results,” says Craig Busch, global treasurer and head of property at Worley in Sydney. “We wanted to let markets settle and wait for a window to open. I wouldn’t say conditions have [fully] stabilised but they are certainly more stable than they have been.”

Having restarted the deal process, Worley’s A$350 million (US$234.3 million) SLB priced on 4 April – less than two hours before the Reserve Bank of Australia elected to leave the cash rate unchanged at 3.6 per cent. The deal also priced just a week after ANZ Banking Group reopened the Australian dollar credit market after the forced takeover of Credit Suisse.

But Worley’s lead managers – BNP Paribas, BofA Securities, Commonwealth Bank of Australia and HSBC took top-line position – say they were confident there had been enough improvement to achieve a successful outcome.

Simon Rutz, director, Australia debt capital markets and syndicate at BofA Securities in Sydney, says sensitivities about spread and yield mean volatility peaked in October and November – when the market was almost at its peak for interest rate expectations, too.

“Investors were being very conservative: they didn’t want to extend duration and they wanted to be compensated for risk, especially when it looked like conditions could worsen,” Rutz comments. “There has been a material shift in sentiment this year. Investors changed their stance and began extending duration from three to five years. They also began looking at credit across the rating band, not just high-quality names.”

This led Worley to reconsider a transaction, as did the flood of Australian dollar financial and high-grade issuance in Q1. “This was a good barometer of investor willingness to participate in new transactions,” Rutz continues.

Lewis Karanicolas, director, debt capital markets at BNP Paribas in Sydney, agrees it was clear markets had recovered sufficiently since the banking sector wobbles to support a deal like Worley’s. “Over the past couple of weeks, we have seen markets stabilise and investors re-engage in credit. We took comfort from the good volume of primary supply we were seeing in offshore markets – US dollars and euros particular,” he says.

These deals were generally well subscribed, he adds – which demonstrated that investors remained liquid and willing to engage. “Notably, after a pause in Australian dollar primary supply, we saw well supported transactions from ANZ and Tascorp [Tasmanian Public Finance Corporation], which again provided useful data points that Australian dollar investors were re-engaged in primary supply.”

Investor engagement after Worley published its half-year results on 22 February ultimately cemented the decision to issue. Rutz notes that there was a routine investor update shortly after which made it clear that there was plenty of interest in a Worley trade. Even after announcing the mandate on 29 March, he says there was plenty of investor feedback despite the formal marketing process not having started.

FAIR VALUE

Nonetheless, the lack of comparable corporate issuance and Worley’s status as a debut local borrower made price discovery challenging. The deal is the first triple-B rated corporate transaction to price in the Australian dollar market since May 2022.

Rutz says the deal team used Worley’s 2026 euro SLB for guidance. Karanicolas adds that the team also considered similarly rated entities, such as Downer, Origin and Incitec Pivot in the Australian dollar market, and Brambles and Arcadis in the euro market.

“Worley’s euro SLB was trading at a swapped-back margin of around 185-190 basis points over swap. Most investors would point to a 30-basis point curve between a three- and five-year issue, so this brought fair value to around 215-220 basis points over swap for a straight five year,” Rutz reveals.

Adding an extra six months of tenor took fair value to around 230 basis points, Rutz continues. The final margin of 250 basis points over swap equated to a new-issue concession of approximately 20 basis points, which Rutz says is “broadly in line with concessions paid on corporate transactions over 2022”.

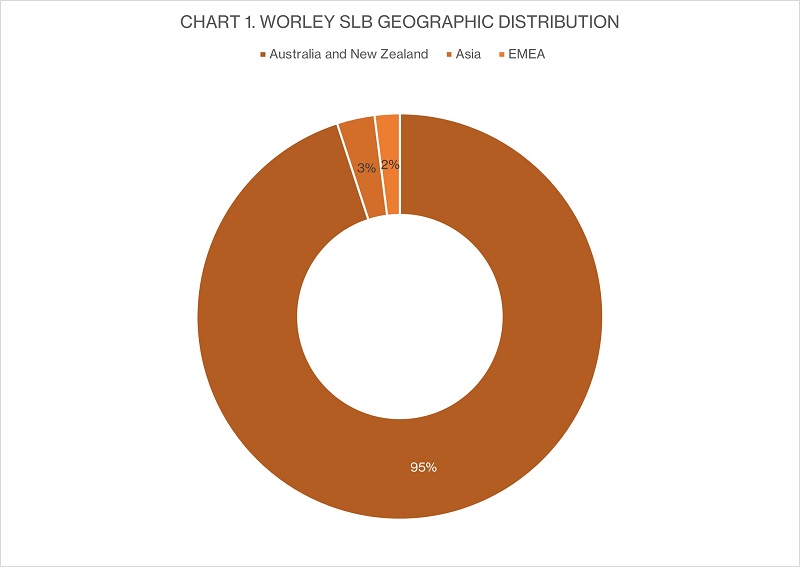

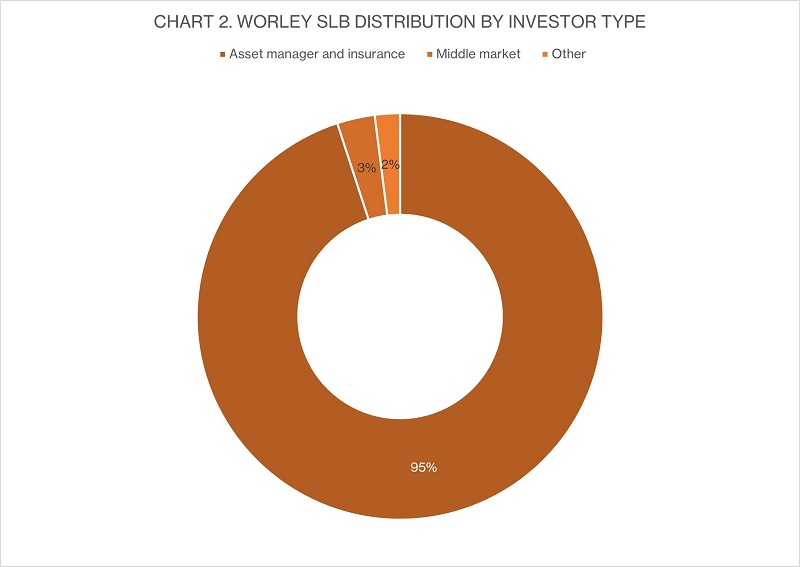

Deal sources say it received a strong response. The book – which included more than 25 accounts – was almost solely domestic-based real money (see charts 1 and 2) and peaked at A$500 million.

The sustainability-linked label may have helped. Rutz says none of the investors in the book had specific environmental, social and governance (ESG) mandates, but suggests the label assisted distribution, in particular to investors that embed ESG into allocation decisions.

“Of the investors that participated, there were some larger ones that did so with a more material bid than usual since the deal fit more of their global mandates,” Rutz continues. “Some ESG-only investors looked at the transaction, too, but they couldn’t make the timing work.”

Busch says he is pleased with the result and would consider another Australian dollar transaction. “The backdrop made us a little anxious but investors are sitting on a lot of cash. We also had good advice from our leads and a promising level of enquiries from investors. Overall, we believe we have a good transaction that was fairly priced.”

Worley has a A$2 billion issuance programme and has now issued in euros and Australian dollars, having printed its €500 million (US$544.9 million) SLB in June 2021. “We were happy with the execution and if the opportunity arises we will come back to the Australian market,” Busch tells KangaNews.

Source: BofA Securities 5 April 2023

Source: BofA Securities 5 April 2023

TENOR OF DOUBT

On the other hand, Worley was not tempted to push for longer tenor. Its deal and first landmark corporate trade in the Australian market so far this year – Telstra Group’s A$650 million print in early March – have 2028 maturities, and both issuers say their sense was that the mid-curve is the best match for demand.

Rutz tells KangaNews: “We always encourage inaugural issuers to focus on hitting the deepest pool of liquidity, which tends to be the five-year part of the curve. Ultimately, the tenor worked for everyone. Worley was keen on getting this into financial year 2029 from a maturity profile perspective, and it suited investors too.”

Busch confirms that the short-to-medium end of the curve suits Worley’s liability management and contract structures. A five-and-a-half-year deal is at the longer end compared with the issuer’s bank debt and its euro SLB was a five-year deal that matures in 2026.

As to whether longer tenor would be available for other corporate issuers, Karanicolas says: “The Australian dollar market is becoming much more flexible on tenors with good pools of liquidity through the curve. Given recent volatility and ongoing price action in rates, though, we still are generally seeing investors prefer to shorten up duration for credit transactions.”

Rutz says there were indications that some investors might be open to exploring longer duration prior to March’s risk events. But they have begun erring on the side of being more conservative.

ENHANCED SPT

From a sustainability perspective, the transaction is very similar to Worley’s euro SLB. The key difference is that it includes an enhanced scope-one and scope-two emissions target. To avoid a coupon step-up in the Australian deal, Worley must reduce its absolute scope-one and scope-two emissions by at least 65 per cent by its 2025 financial year, against a 2020 baseline. This represents an uplift on the euro sustainability performance target, which Worley has already achieved.

Sources familiar with the deal say that Worley’s emissions are largely stem from its office operations. With a lot of these sites closed or unused during the pandemic, the borrower’s emissions decreased quicker than expected – leading Worley to seek an increased SPT for its Australian dollar transaction.

Karanicolas notes that the Sustainalytics SPO for the most recent transaction refers to the SPT as “highly ambitious”. This is the same assessment the SPO provider made for the 2021 SPT.

“The SLB label is a useful way for issuers to demonstrate their commitment to ESG and Worley’s sustainability strategy is very well received by investors. The company has a very well-articulated sustainability strategy with net zero targets across scope-one and scope-two by 2023 and scope-three by 2050,” Karanicolas continues.

Rutz adds that the updated SPT was received well by the investor community. “When we announced the mandate in September, investors asked why the KPI and SPT were different from the euro line. It was a very easy and positive message to articulate – that it was because Worley performed better than expected during COVID-19 and formed better efficiencies and processes. Worley wants to be a leader in the space and continue to have ambitious targets. The change was very well-received by investors.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Vicinity’s domestic print shows ongoing appetite for real estate

Vicinity Centres’ Australian dollar return provides another example of investor support for a wider range of corporate sectors – in this case, an oversubscribed book coming in for an issuer in the retail real estate sector as it seeks to move on from the pains of the pandemic. The issuer says domestic market conditions proved attractive for pricing and tenor.

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.