Securitisation flow bounces back – and keeps bouncing

Coming off the back of difficult issuance conditions and narrow demand in 2022, the Australian securitisation market that met the new year’s first wave of deals provided more positive transaction outcomes. Even more reassuringly for market participants, deal flow continued as volatility surged in late March.

Kathryn Lee Senior Staff Writer KANGANEWS

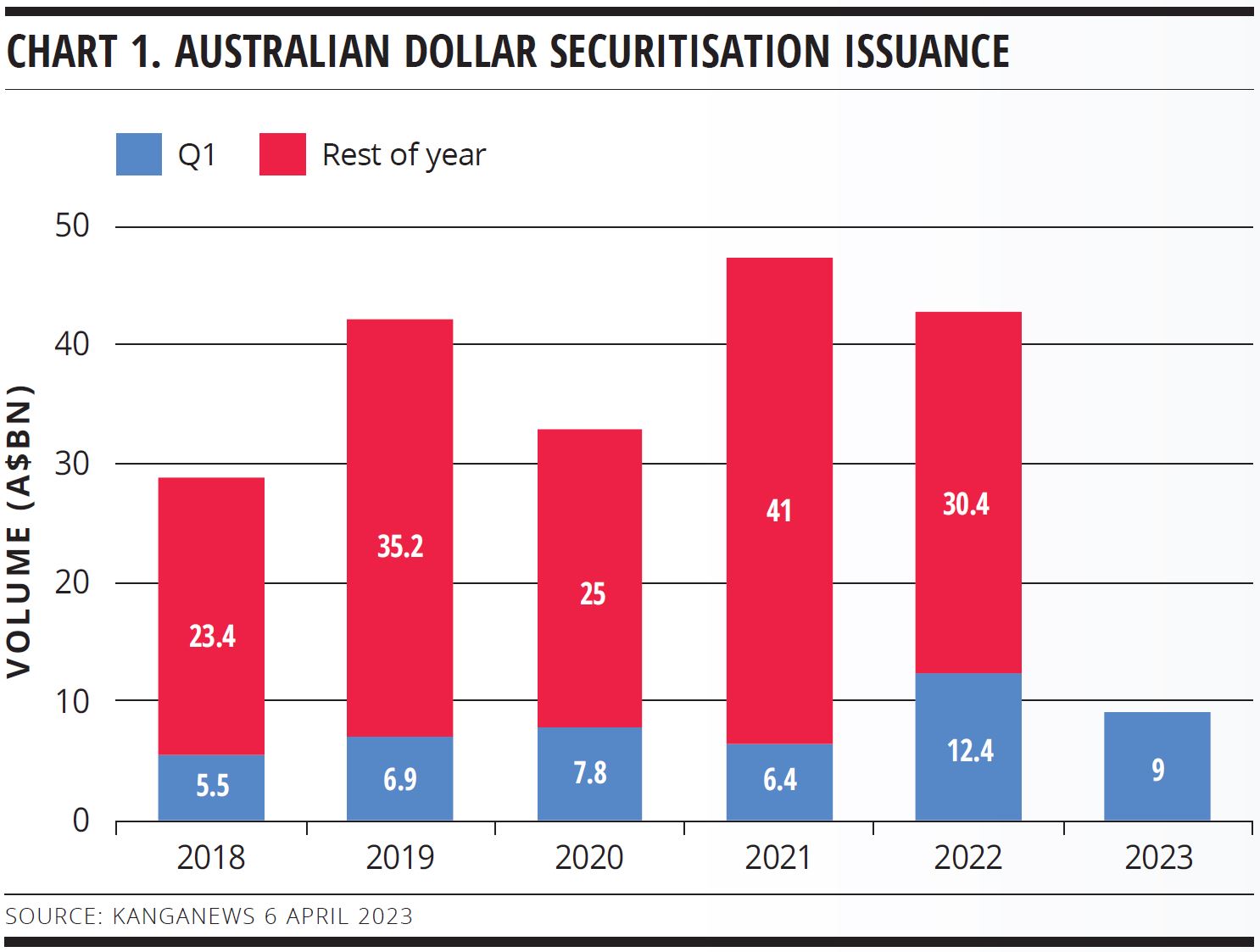

Taking a cue from the strong levels of oversubscription in the senior-unsecured space in January and February, Australian securitisation issuance sprang to life in mid-February. Nonbank issuers Columbus Capital, Liberty Financial and Pepper Money all managed upsized A$1 billion (US$666.2 million) prints over the course of barely 24 hours, contributing to a healthy quarter for securitisation supply (see chart 1).

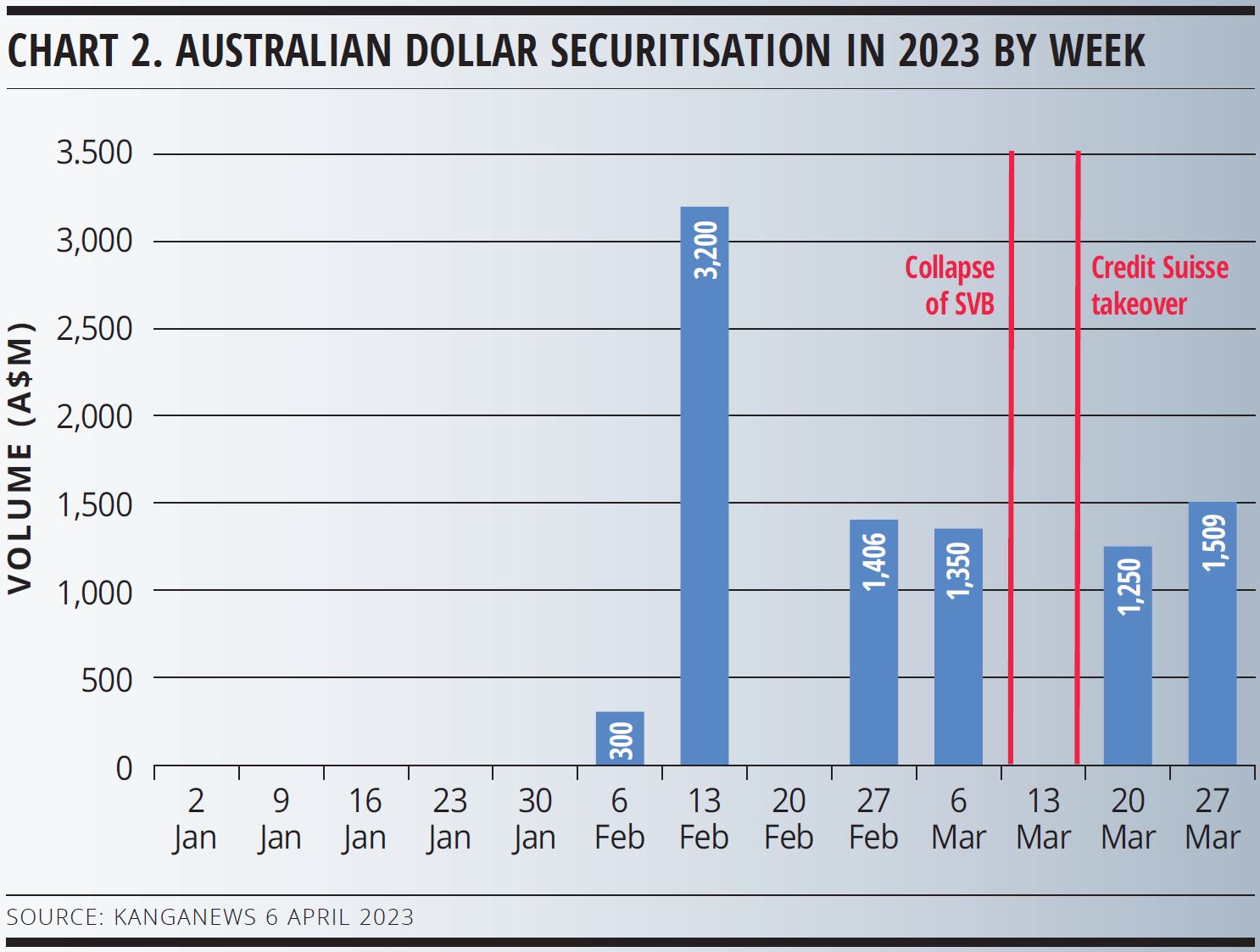

The new-issuance market took a breath in mid-March to digest the collapse of Silicon Valley Bank and the forced takeover of Credit Suisse. But deal flow returned with a vengeance at the end of the month (see chart 2): five securitisation deals priced between 23 March and the end of the month, for total volume of more than A$2.75 billion, while Angle Auto Finance proved there is still appetite for new issuers with an upsized A$900 million print on 5 April.

Issuance volume does not tell the full story of improving market tone, either. While headline supply was relatively robust in 2022, issuers and arrangers acknowledge that demand tended to be narrow and deals often relied on supporting bids from joint lead managers. The tone improved in the new year.

Craig Stevens, director, securitisation origination at National Australia Bank in Melbourne, says early-year transactions demonstrated the risk-on tone among investors. “This is very much contrary to the market sentiment that was prevalent for most of 2022, which made it challenging to build a transaction,” he comments.

The robust bid came through first for senior-unsecured deals in the Australian dollar market in 2023, with bank transactions typically enjoying strong bookbuilds and post-issuance tightening. Commonwealth Bank of Australia’s A$5 billion senior-unsecured deal on 9 January was the market’s largest-ever credit deal while Westpac Banking Corporation’s A$4.25 billion transaction, priced on 10 February, recorded the largest-ever final orderbook for an Australian dollar bank deal, at A$7.5 billion.

Stevens says this momentum continued into the residential mortgage-backed securities (RMBS) market. “Investors that did not participate last year, or did so at reduced volume, are more active and are allocating in larger size,” he notes.

PRICING TRENDS

David Carroll, Columbus’s Sydney-based treasurer, says the difference between the issuer’s 2023 execution experience and its previous deal, which priced in mid-November last year, is considerable. The trades had slightly different collateral – with the 2022 deal comprised entirely of investment loans – but demand was an entirely different story.

Columbus’s February deal opened for indications of interest with indicative volume of A$500 million and price guidance of 145-150 basis points over BBSW on its triple-A rated A1-AU tranche. By pricing, the margin tightened to 140 basis points over BBSW and total transaction volume doubled. By contrast, Columbus Capital Triton 2022-4 managed a slight upsize – to A$550 million from A$500 million – and its senior margin was the wide end of guidance, at 170 basis points over BBSW.

“The market was subdued in November and December with year-end approaching,” explains Carroll. “By contrast, we launched the new deal at A$500 million with the hope of reaching A$1 billion, and in the end we received A$2.4 billion in bids. There was very healthy demand across all tranches – much more than expected.”

It was a similar story for Liberty, according to Peter Riedel, the borrower’s Melbourne-based chief financial officer. The issuer expected a transaction would do well in the early-year environment, noting the senior-unsecured market’s success this calendar year as well as secondary performance. But Riedel says the exact level of engagement was a surprise to the upside. The deal garnered strong coverage ratios across all notes, he adds.

“The long-dated triple-A rated tranche was 2.1 times oversubscribed at the final issue size, while the A2 tranche was 2.2 times oversubscribed,” Riedel reveals. “Most of the lower-rated notes were more than three times oversubscribed – though this is not unusual for mezzanine tranches.”

Liberty’s RMBS has a pool of prime and nonconforming mortgages, whereas Columbus offered a prime mortgage pool. The former did not tighten by as much during the execution process: its biggest tranche printed at 165 basis points over BBSW, the tighter end of its price guidance at launch. The difference between the two pools may explain the slightly different outcomes but Riedel also says Liberty did not want to squeeze pricing.

“We did not feel it was appropriate to test the price tighter,” he confirms. “Rather, we wanted to support our partnerships with the investors that drove the transaction from the outset. We are very much partnership-based and do not treat each issue as a transaction to optimise. We approach the market with a long-term mindset.”

While deal flow resumed swiftly after risk events in late March, there was an impact on pricing. For instance, La Trobe Financial printed A$1 billion of prime and nonconforming RMBS on 28 March with a margin of 175 basis points over BBSW on the longer-tenor senior notes.

DEAL DISTRIBUTION

Perhaps the best news for securitisation issuers is that investor engagement has widened in 2023. RMBS deals received a greater bid from offshore than was typical in 2022, though market users say there is still some way to go for this bid to return to its peak.

Thinktank priced an upsized A$750 million RMBS on 9 March and Ernest Biasi, the issuer’s Sydney-based treasurer, says: “Similar to the experience on our 2022-3 CMBS [commercial mortgage-backed securities] deal in early December, on this latest occasion we saw a number of investors return that had been less active last year. This was most evident in the senior and junior triple-A notes, which returned strong coverage ratios.”

Specifically, there were five more investors in Thinktank’s latest book than its previous RMBS – a A$500 million deal priced in August last year. This brought the total number of participating accounts to 20, with a relatively even split between domestic and offshore, and balance sheet and real-money accounts.

Nonmortgage securitisation has also seen revived offshore demand. Angle Asset Finance priced A$400 million of auto- and equipment-backed notes on 10 March, with nearly one-third of the book sold to international investors. Debbie Long, head of treasury at Angle Asset in Sydney, says: “We were very pleased with the degree and diversity of investor interest after we took the opportunity to market our transaction via an offshore roadshow. The successful presentations attracted more offshore interest.”

Riedel believes offshore interest could inch higher if economic uncertainty in Europe begins to ease. “Geographic distribution is getting closer to a more traditional 50/50 split. Whereas last year was principally domestic, there is definitely more interest and demand from northern hemisphere investors, which is terrific,” he says.

In addition to improving offshore participation, Stevens adds that the return of domestic balance sheets is an important development. “They were less prominent last year but balance sheet support helped deliver a strong senior tranche in Columbus’s transaction,” he says. “The mezzanine triple-A notes also saw a strong return, and were multiple times oversubscribed. This reflects the relative value available in the market.”

Stronger investor participation has also paved the way for less joint lead manager dependence – a positive development after the difficult conditions of 2022. Lead managers still play a role but appear less critical to deal outcomes.

“The leads obviously played a large part in allowing transactions to move forward to execution last year,” Stevens tells KangaNews. “It was a much more difficult market. This year, once mandates were announced investor feedback was readily available so the lead manager requirement to progress to execution wasn’t as important. There was a lot more confidence in moving to launch and subsequently upsizing – as reflected in the multiple levels of oversubscription.”

Despite positive deal outcomes, the funding and lending markets remain challenging. Biasi says Thinktank remains committed to its organic growth strategy of secured residential and commercial property lending to self-employed, self-managed superannuation fund and small business borrowers.

On the other hand, he adds: “While term market pricing has improved from last year, funding costs remain elevated and there is intense competition from banks and nonbanks in the lending market, placing persistent pressure on net interest margins. The impact of 10 or so consecutive official interest rate rises has also softened demand for new credit, with more refinancing activity across the market as borrowers become increasingly focused on getting the best possible interest rate on their loans.”

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news