Corporate sweet spot

Australian corporate borrowers have every reason to favour debt capital markets over bank loans for their funding needs in 2023. Risk events and the economic outlook mean caution remains the order of the day domestically, however, and while deal flow is likely to pick up market participants acknowledge that global options are providing strong competition.

Laurence Davison Head of Content KANGANEWS

Bond issuance by Australian companies was one of the numerous bits of collateral damage caused by the overhang of cheap liquidity from pandemic-era policy. While 2020 and 2021 were solid years for Australian dollar corporate issuance, by last year the glut of cheap cash in the banking sector made selection of refinancing options a virtual no-brainer for corporates: bank loans were available at unprecedented cheap pricing with which the bond market simply could not compete.

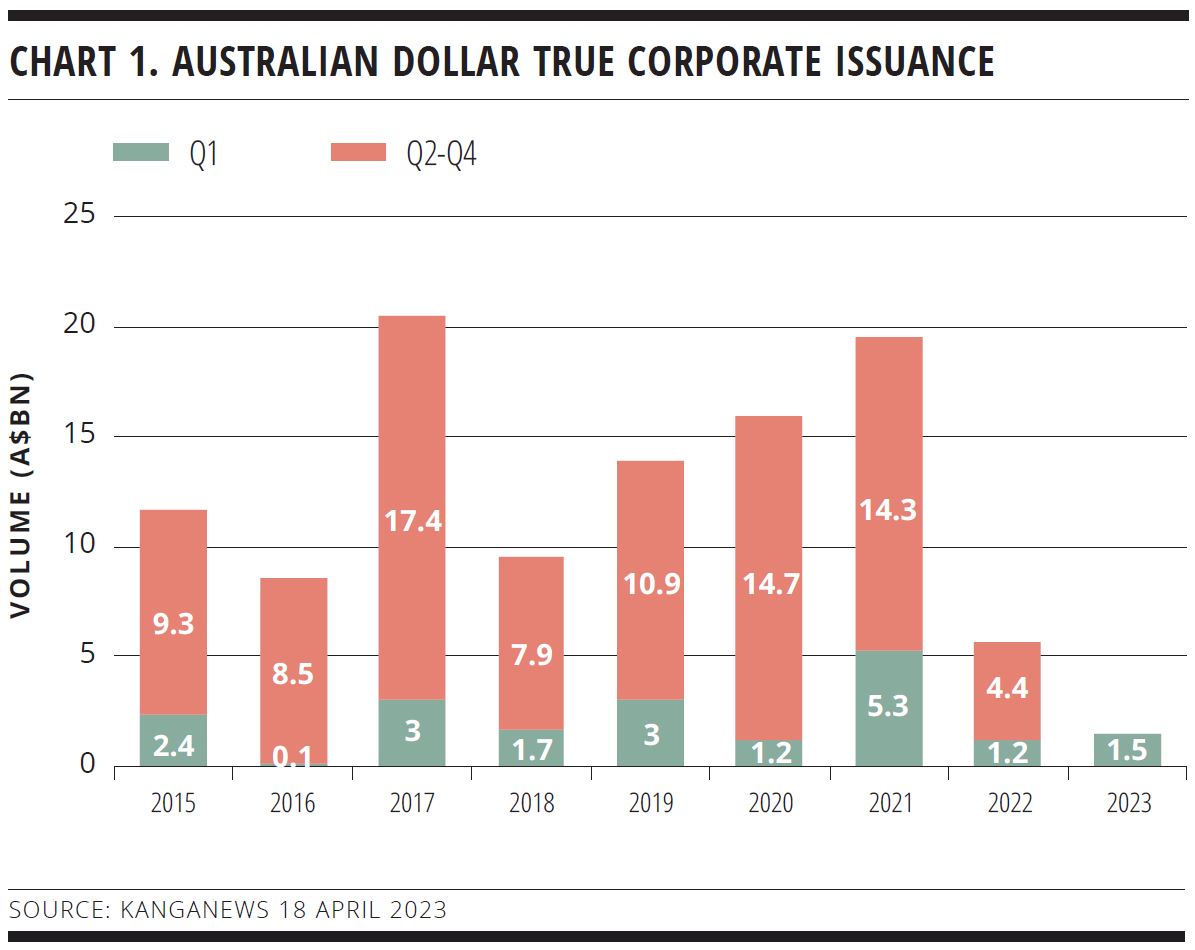

The impact on volume was stark. Domestic corporate issuance collapsed to barely A$5 billion (US$3.3 billion), the lowest for more than a decade (see chart 1). More than a quarter of the total came from a single issuer – NBN Co – with a substantial privatisation financing facility to term out and thus a clear motivation to come to market regardless of conditions.

Australian corporate borrowers were not just absent from their home market. Only a handful of Australian-origin deals priced in the US dollar 144A or euro benchmark markets and it was also a notably quiet year for US private placement (USPP) issuance from Australia. On the other hand, if Australian dollar investors were clamouring for corporate supply their voices were not loud enough to attract global issuers: Australia has seen very little international corporate supply since 2019 and there was less than A$1 billion of such issuance in 2022.

CHANGING CONDITIONS

The fundamental drivers have shifted in 2023, however. Banks no longer have access to ultra-cheap funding from central banks – indeed, the events of March, when Silicon Valley Bank (SVB) and Credit Suisse headlined global banking sector woes, suggest that credit constraints are likely to be the story of the coming months. While market participants universally agree the Australian banking complex is in robust shape, the days of knockdown pricing in the loan market are likely a thing of the past.

“I don’t believe we are necessarily going to see anything like stress in the loan market but what we are experiencing is bank pricing moving out. This has already started and is likely to continue over the course of the year,” Sian Nagle, director, debt capital markets at ANZ in Sydney, told delegates at the KangaNews Debt Capital Market Summit on 20 March.

Nagle suggested the differential between loan and bond pricing had already reduced considerably, a clear contrast with last year when some companies found bank pricing 30-40 basis points tighter than the bond market could have offered.

Peter Block, Sydney-based head of debt capital markets, Australia at Westpac Institutional Bank, adds: “Availability of credit in the loan market is tightening and banks’ cost of capital is going up – the divergence in pricing between loans and bonds in 2022 has largely closed. Another thing we have noted is that the availability of bank liquidity from Asia has fallen.”

There are also obvious reasons for credit investors to support the return of true corporate supply. The first two-and-a-half months of 2023 were very positive for Australian dollar credit issuance in aggregate but supply was dominated by bank issuers.

While market conditions were more challenging in 2022, the volume outcome was largely the same: highly active banks, almost no corporates.

Will Manfield, head of credit trading at Westpac in Sydney, suggested at the KangaNews conference that investors that did not pursue an aggressive strategy of buying corporate paper in the secondary market would inevitably have significantly reduced their exposure to corporates in 2022 given the high volume of financial and lack of corporate supply. This trend would have continued into Q1 this year.

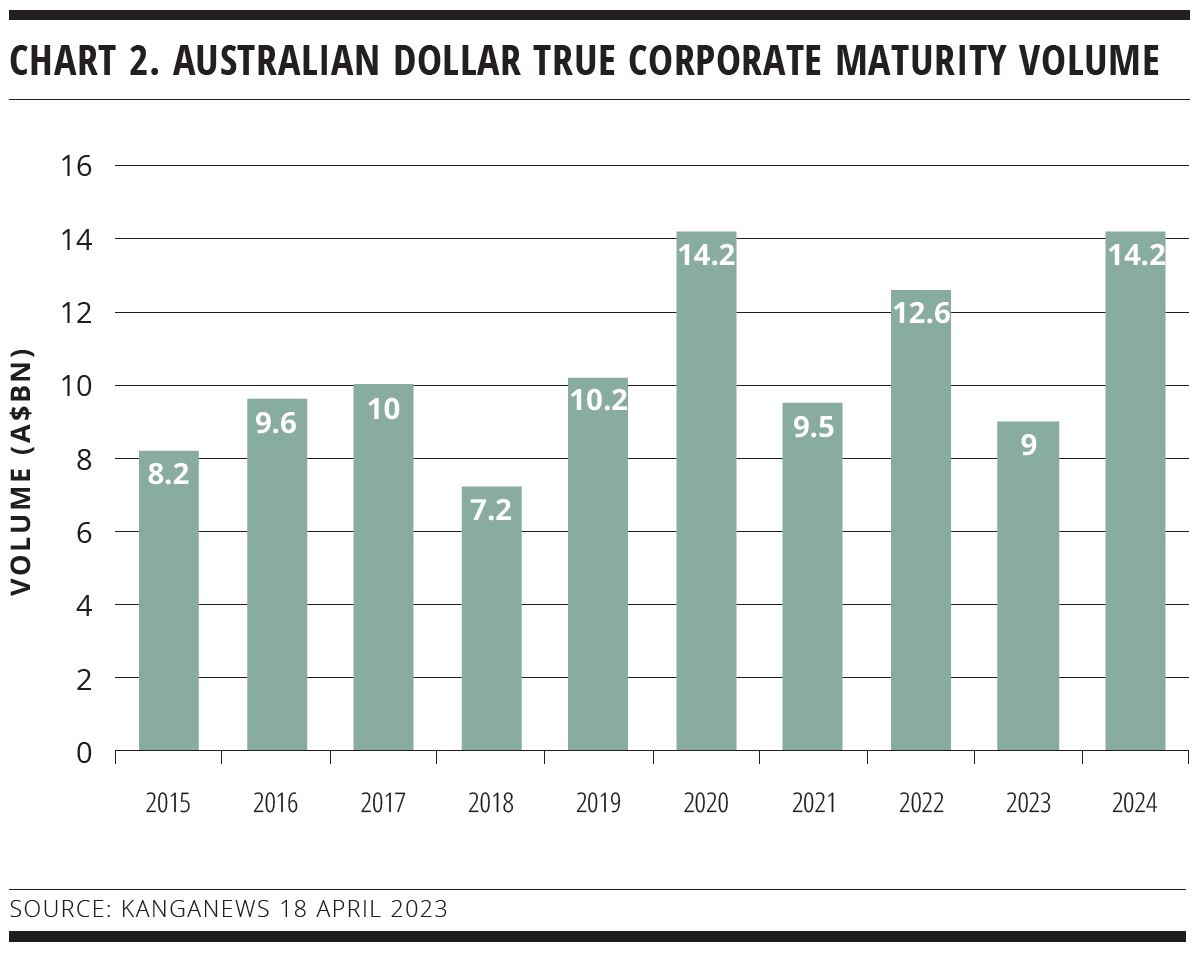

Coincidentally but exacerbating the impact, 2022 was close to a record year for Australian dollar corporate maturities (see chart 2). This year is closer to the long-run average but maturities take another step up in 2024.

The early signs from new deals in 2023 were that demand was keenly chasing corporate issuance. The first landmark issue of the year came from Telstra Group on 1 March. Pricing on the five-year deal was 93 basis points over swap benchmarks – 5 basis points tighter than a Westpac Banking Corporation five-year senior-unsecured print two weeks earlier and 12 basis points inside the margin achieved by HSBC Sydney Branch on its five-year priced on 24 February.

Manfield suggests the relatively unusual outcome of high-quality corporate names pricing through the bank curve can be justified by technical factors.

“Corporate maturities have not been replaced with new supply, while bank issuance has been elevated. I agree that corporate pricing looked tight on a relative basis in Q1, but it is the product of diversification and portfolio construction dynamics,” he said at the KangaNews conference.

On the other hand, the more promising new-issuance environment at the start of 2023 did not cause a rush of corporate supply. Telstra brought the only benchmark deal before the failure of SVB in mid-March sparked a wave of volatility, wider spreads and execution risk. Toyota Finance Australia and Volkswagen Financial Services Australia returned for three-year prints at the end of March, then Worley revived a deal it put on hold late last year – a five-year sustainability-linked bond – for pricing on 4 April.

“Corporate borrowers want to lengthen duration beyond what is available in the bank market, and this means we can’t expect them to come to market regularly for less than seven-year tenor. If we want to consider ourselves an international capital market, we need to be able to offer 7-10 years reliably.”

Having opened the market for 2023, Telstra’s Melbourne-based head of corporate finance and treasurer, Guy Wylie, said at the KangaNews conference that there are compelling reasons for other corporate borrowers not to wait on the sidelines in anticipation of further improvement in new-issuance conditions that might never come.

“I suspect conditions might settle down over the coming months, and with fixed rates falling local deals could well be more conducive,” Wylie commented. “I don’t expect the local market to be on hold for months. What I do anticipate is that the next couple of years are going to be choppy, so my advice would be: if a deal is there, take it – don’t sit back waiting to hit a price target or for another 5 basis points.”

The signs are that at least some borrowers are following this advice. Stockland Trust Management priced A$250 million on 18 April in the first seven-year Australian dollar corporate deal of 2023, and market sources say May was always the most likely month for deal flow to emerge pending supportive market conditions.

On the other hand, rather more corporate issuers are seeing the best opportunities to return to capital markets offshore. Late April saw CIMIC, Sydney Airport, Telstra and Transurban print euro deals, while KangaNews understands names like AGL Energy, Aurizon, Dalrymple Bay Infrastructure and Orica were preparing USPP transactions at the same time.

DOMESTIC SELECTION

The question, therefore, is what proportion of supply will be attracted to the Australian dollar market. USPP investors remain hungry for the type of corporate name that is common in Australia – asset-heavy, especially infrastructure and regulated utility credits – while euro new-issue premia have been tight for Australian-origin deals.

On the other hand, corporate borrowers continue to say they have a natural bias toward issuance at home if the domestic market can provide reliable liquidity, pricing and tenor. Endeavour Energy has issued every other year since its 2017 debut, on each occasion for A$350 million and at seven-year duration.

Endeavour’s Sydney-based treasurer, Alex Pritchard, said at the KangaNews event: “We have always considered the AMTN market to be a stable option because investors here understand our asset, that it is regulated and the nature of the regulation. We don’t need to go through an education process. Even though we are unlisted, local investors know they can always pick up the phone, and of course we are in the same time zone.”

The size of deal Endeavour is seeking and the overall scale of its debt book also fit well with the Australian dollar market. But even credits with financing requirements sufficient to make global benchmark options relevant say home-currency issuance has a natural advantage.

Telstra has issued a substantial volume of euro deals over the years, although maturities mean its outstanding volume has eased of late. The company takes no currency or rate risk – issuance is all swapped back to Australian dollars – but it does have credit risk from the banks that provide its swaps.

“The Credit Suisse situation shows us how careful we need to be, because when bank risk events happen our exposure to that bank can affect our ability to draw a revolver or mark our swap book to market. When we are talking about €6-7 billion [US$6.5-7.6 billion] of euro debt, this can mean quite big numbers,” Wylie explained at the DCM Summit.

For Telstra, issuing Australian dollar debt relieves some of this risk and reduces its exposure to various banks. “We are an Australian dollar company and we would love to have a large, liquid local market,” Wylie continued. “If we did, we would move from where we are now – about 70 per cent euro bond funded – to Australian dollars straight away.”

TENOR HUNT

As well as the general atmosphere of caution domestically, availability of tenor could be a key factor in determining how much of 2023’s deal flow lands in the domestic market. The Australian market often lags global options in reviving positive tone after risk events and 2023 appears to be no exception.

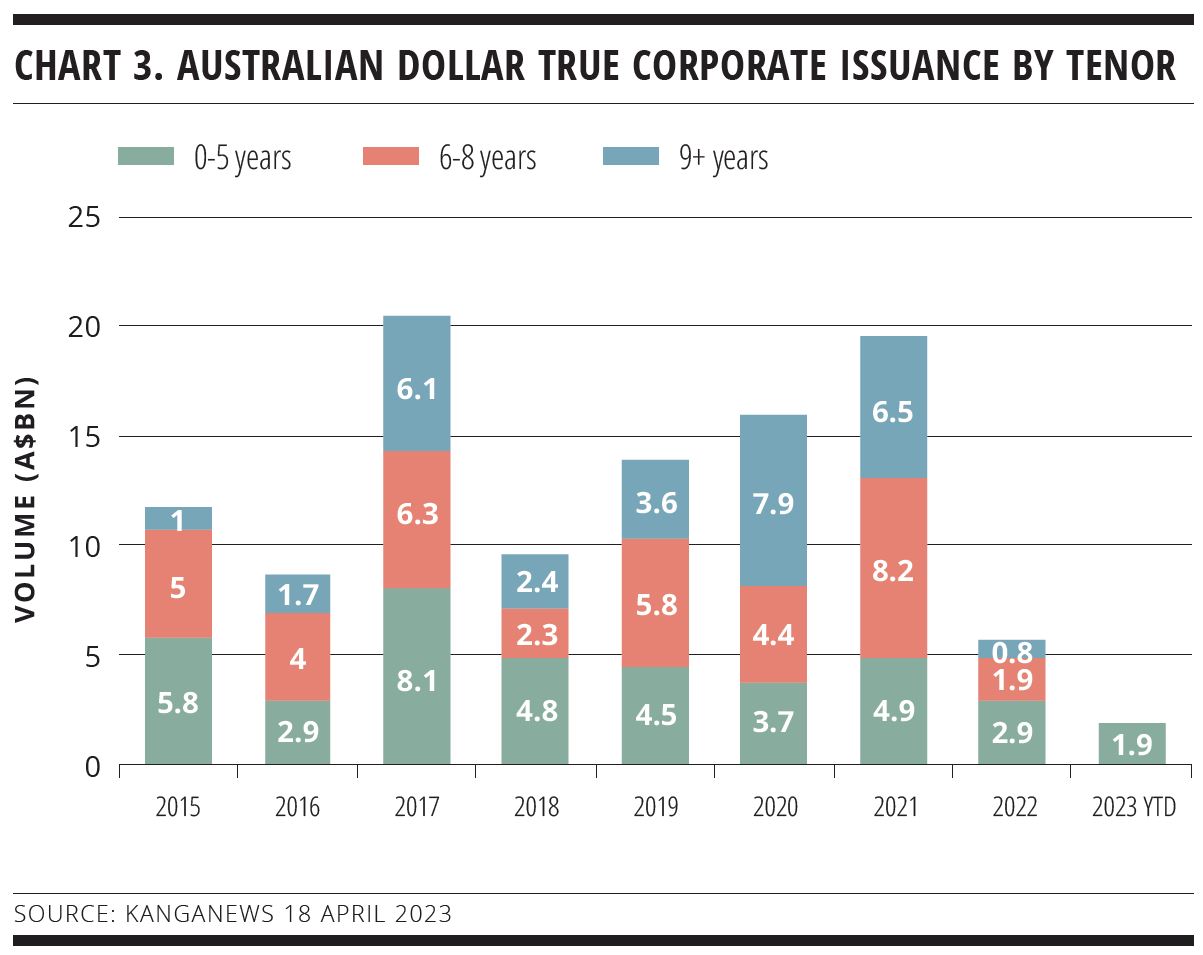

Meanwhile, when the Australian dollar market has a good year for corporate issuance volume the differentiating factor is the amount of longer-duration deals completed. This was certainly the case in the three most recent years of A$15 billion or more issuance: 2017, 2020 and 2021 (see chart 3).

The impetus is clear for borrowers – and it has not escaped the notice of rating agencies. Paul Draffin, analytical manager, corporate ratings at S&P Global Ratings in Melbourne, pointed out at the KangaNews conference that a year of leaning on banks for refinancing has had an impact on the relatively long weighted-average maturity profiles corporate borrowers took into 2022.

“The bank market is typically 3-5 year funding. It made sense as an easily accessible option last year, but the problem borrowers are facing is that their maturity profiles are shortening with every passing month. We anticipate more longer-dated issuance this year,” Draffin said.

Some longer-duration deals have been possible in the Australian dollar credit market in 2023, even before the widescale return of corporate borrowers: ANZ Banking Group and Commonwealth Bank of Australia printed a combined A$2.75 billion of 15-year non-call 10 tier-two paper in February and March, in deals that market sources say were well supported by real-money investors.

Nonetheless, one challenge with tenor extension is that there is far from universal investor support for it. Relatively tight corporate spreads and the shape of the curve are acting as a disincentive for some funds. Adrian David, division director at Macquarie Asset Management in Sydney, says the firm is cautious given the macroeconomic backdrop and the long and variable lags that apply to monetary policy. The asset manager expects credit spreads to widen over the next 6-12 months.

“It is not that we have no appetite for a corporate borrower seeking to access seven-or 10-year funding. But we would need to have a high conviction on the stability of the issuer’s business and its approach to ESG as well as a favourable view on relative pricing,” David reveals. “Our ability to rotate out of existing longer-dated maturities would also be a factor.”

This view is not universal, however; some market users point to curve steepening during April while others believe corporate spreads already offer good value. Other buy-side sources suggest the long-term value of supporting the type of issuance corporate borrowers favour may outweigh any current relative-value concerns.

“Corporate borrowers want to lengthen duration beyond what is available in the bank market and this means we can’t expect them to come to market regularly for less than seven-year tenor,” argues Phil Strano, senior portfolio manager at Yarra Capital Management in Melbourne. “If we want to consider ourselves an international capital market, we need to be able to offer 7-10 years reliably.”

Strano says he would be “flabbergasted” if the Australian dollar market was not able to offer good-quality corporate borrowers seven-year tenor. He suggests a steeper curve may make the question whether issuers are willing to engage on price.

The connotations of divided investor views may not be as negative as they appear. One market source tells KangaNews Telstra achieved a substantially oversubscribed book and tight pricing despite some accounts not participating – which, the source says, demonstrates the capacity of the Australian dollar market to satisfy issuer needs without requiring across-the-board buy-side support to do so.

Issuer pricing expectations are a real issue, however. But not all corporate borrowers are created the same and tenor extension is not equally valuable to all of them or to an infinite extent. Some issuers – auto-related financials and some property developers, for instance – actually favour mid-tenor issuance. Even those with long-term assets may not need to push duration deep into the long end.

For instance, Pritchard said at the DCM Summit: “Seven years has worked well for us domestically. We have considered 10 years in the past, but we have never had the sense of sufficient interest. This is from the perspective of liquidity: we want there to be a secondary market in our bonds with ample trading. This has led us to aggregate our issuance into seven-year tenor, which has been our sweet spot.”

Nagle commented: “Corporate treasurers are cost sensitive and in most cases the next deal they do will be their first experience of the debt capital market in the newly higher interest rate environment. Even if the curve from seven to 10 years is not particularly steep, many borrowers are saying they are happy to stay a little shorter in these conditions.”

Duration cannot be considered in isolation, either. Wylie says one of Telstra’s main concerns when transacting domestically is the time it takes to execute. Volatile conditions exacerbate this problem, making it hard for an issuer to be in and out of the market inside a day – an outcome that is typical in benchmark markets like euros and US 144A.

“The advantage of the five-year deal we did, other than that it sat in a tenor sweet spot, was that we believed the duration would maximise liquidity and therefore develop enough momentum to complete in a couple of days,” Wylie suggests.

Taking all factors into consideration, by mid-April Australian market participants had a degree of confidence about the pipeline of new corporate issuance for the rest of the first half. The turmoil of late March does not appear to have dissuaded issuers from pushing ahead with planned transactions. In fact the timing of risk events may have been somewhat fortunate – falling before most corporates planned to issue but at the back end of a hectic period of financial supply, meaning few deals of any type were actually derailed.

“From a fundamental perspective, we feel the domestic market is still in quite a strong position,” Penny Schubach, executive director and head of corporate DCM originations at CBA, said at the KangaNews event. “In this instance it is actually beneficial for corporates that it takes quite a few weeks to get ready for a transaction. Many issuers are buoyed by the financial issuance and the Telstra deal earlier this year. This gave them confidence to recommence a capital markets work stream, and it is fair to say there are a lot of issuers out there looking at the market.”

It may be more realistic to expect five-and seven-year tenor to provide the best opportunities, which may enhance the appeal of offshore markets to some issuers. Block adds: “Lots of borrowers are actively doing diligence on the state of the market and its availability as an option for them. Some will be happy with 5-7 year funding, others would like to go longer – and it has to be acknowledged that the tone remains cautious.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Vicinity’s domestic print shows ongoing appetite for real estate

Vicinity Centres’ Australian dollar return provides another example of investor support for a wider range of corporate sectors – in this case, an oversubscribed book coming in for an issuer in the retail real estate sector as it seeks to move on from the pains of the pandemic. The issuer says domestic market conditions proved attractive for pricing and tenor.

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.