Securitisation finds its role in New Zealand despite near-term headwinds

Participants in the New Zealand securitisation market believe the asset class has an increasing role to play in the local credit landscape on the back of growing momentum in recent years. Economic and regulatory challenges are likely to put a ceiling on near-term growth but there is a baseline level of confidence in asset quality and the risk-return equation of structured finance.

Laurence Davison Head of Content KANGANEWS

On 10 May, market participants gathered for the first time under the banner of the Australian Securitisation Forum (ASF)’s New Zealand Securitisation Conference in Wellington. Delegates heard of a fragile economy in which the Reserve Bank of New Zealand (RBNZ) may feel obliged to kill any nascent recovery if it emerges before the inflation beast is defeated, but solid performance of loan assets and a robust value proposition for securitisation.

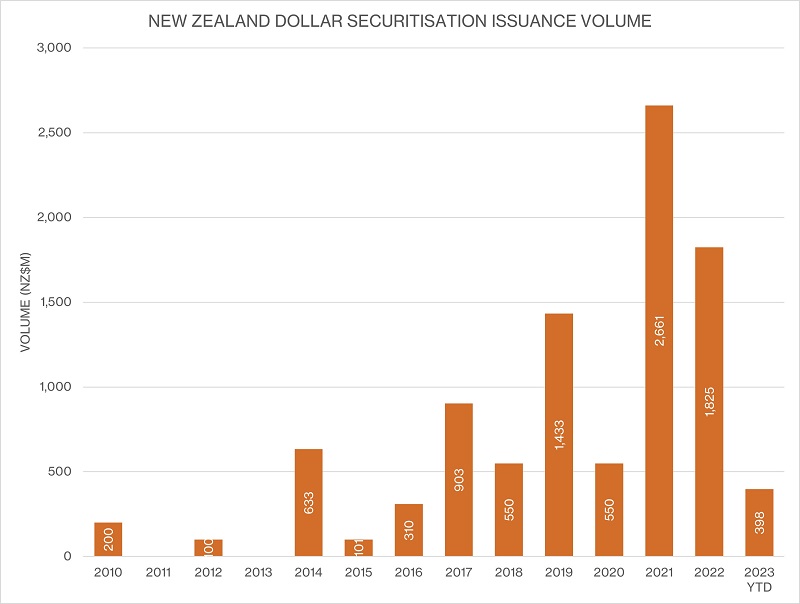

The first post-financial-crisis securitisation deal in New Zealand priced in 2010. Momentum was initially slow to build and easily stalled by market travails, but took a step forward in 2019 when more than NZ$1 billion (US$626.2 million) of public deal volume vale to market for the first time (see chart).

The pandemic led to another pause but issuance roared back with another record year in 2021. Global market volatility meant a step back last year but total issuance was still the second-highest on record.

The primary driver of issuance volume has been the growth of existing nonbank lenders and the emergence of some new names in the space – notably including a clutch of Australian firms – seeking to take advantage of the opportunity created by banks’ pull-back from certain types of lending. As in Australia, nonconforming mortgages and personal lending are the leading categories.

Source: KangaNews 17 May 2023

ECONOMIC CHALLENGES

The outlook is not dire despite challenging economic conditions in New Zealand. Inflation – and thus the pace of central bank rate hiking – has been particularly acute and some economic data make sobering reading. But consumption, employment and credit quality have to date shown a degree of resilience that many admit has been more persistent than expected.

“Consumer confidence levels are awful – as bad as they have been for decades,” commented Craig Ebert, senior economist at BNZ. “The cause is inflation, which people absolutely hate. But consumption remains solid, with the key variable here being the unemployment rate. The general expectation is that unemployment has to rise [for inflation to die down], but until that point it – and wages growth – is holding everything together.”

The pace at which the official cash rate has risen has been dizzying, as the RBNZ hiked by 4.75 basis points in 18 months to April 2023 – a full per cent more than the equivalent move by the Reserve Bank of Australia. The impact on households has been profound, but perhaps not catastrophic.

Miles Workman, senior economist at ANZ, noted that the share of household income devoted to debt servicing dropped to 5 per cent on aggregate at the peak of QE and ANZ expects it to grow to 11 per cent in the current cycle. This is still some way from the historical peak – it was 15 per cent just before the financial crisis – but that does not mean there is no reason for caution.

“The pace of change is the concern,” Workman explained. “It helps explain why households are so pessimistic – and if the pessimism becomes endemic it could mean a harder landing than we currently expect.”

Loan arrears have increased as rates have climbed. However, lenders – especially the nonbanks that provide all New Zealand’s securitisation supply – are yet to see arrears rise above historical norms.

“There has been an uptick in mortgage arrears but not a dramatic one,” said Caroline Dunlop, head of funding at Avanti Finance. “Our borrowers are not on fixed rates so there is less sticker shock from rate hikes – each one comes through directly, giving borrowers more opportunity to adapt over a period of months.”

There are some grounds for optimism. Several speakers at the ASF event expressed surprise at just how well consumption has held up in New Zealand, despite household confidence surveys that repeatedly suggest it should be in freefall. The main reason is that unemployment remains low, underpinning a baseline of loan performance and economic activity even in the face of aggressive tightening.

ANZ’s analysts recently upgraded their forecast for the New Zealand housing market, to an 18 per cent peak-to-trough fall from their previous expectation of 22 per cent. This may seem like a marginal revision, Workman suggested, but in the context of a market that has already fallen by 16 per cent it represents a significant bring-forward of the bottom.

“We believe there is a consistent growth opportunity in Australia and New Zealand, based on the service proposition offered by nonbanks. We are actively diversifying our asset base in New Zealand, pushing in particular into secured lending, through the broker market, across transport and construction equipment.”

On the other hand, the RBNZ may not be willing to countenance a recovery just yet. Inflation has eased somewhat – CPI was 6.7 per cent in Q1 2023, down from a peak of 7.3 per cent in June 2022 – but has yet to decline significantly and is still well above the target band. There is a widespread expectation that the RBNZ will not ease of the tightening action if it feels it remains necessary.

“The RBNZ may make a recession happen even if one doesn’t happen naturally,” Workman said. “Ultimately, inflation is still at risk of becoming unanchored so the reserve bank will believe – rightly – that it still has work to do.”

NONBANK GROWTH

There are obvious grounds for caution, but securitisation issuers and investors suggest these do not add up to the necessary conditions for a major reversal in their asset class. The bottom line is that while employment numbers stay solid most debtors will continue to make payments.

“New Zealand, like Australia, does not have the clustering of risks that would be necessary to prompt a mortgage cliff. As a result, it presents an interesting risk-return profile,” argued Rob Camilleri, partner at Realm Investment House.

Nonbank lenders are cautiously optimistic about their own growth prospects even in a more challenging market. Dunlop acknowledged that mortgage origination has been slow this year but added that Avanti’s auto business has been very strong – in fact the challenge in the auto space remains supply of vehicles. There is also ongoing appetite for small business and consumer lending.

Fraser Wilson, head of treasury and funding at MTF Finance, echoed the positive tone from the auto sector. “A year ago, I expected our volume would slow significantly off the back of reduced transaction activity in the auto market. There has indeed been less activity in car sales and imports are down, which has kept prices high – but MTF Finance has been originating record volumes nonetheless. Anecdotally, it seems to be getting harder for borrowers to top up their mortgages to buy a car, and the difference between the rates we charge on car loans and rates for a mortgage has reduced.”

The New Zealand nonbank lender sector has perhaps not proliferated to the same extent as its Australian equivalent but there are certainly more active players now than there were even a few years ago. Growth in the market as a whole and individual players’ books has brought a growing number of issuers to the securitisation market (see table).

NEW ISSUERS IN THE NEW ZEALAND SECURITISATION MARKET SINCE 2010

| Year | Issuer | Number of deals completed, Jan 2010 – May 2023 |

|---|---|---|

| 2010 | NZF Group PSIS |

1 1 |

| 2011 | None | N/A |

| 2012 | MTF Finance | 7 |

| 2013 | None | N/A |

| 2014 | Fisher & Paykel Finance Resimac |

4* 6 |

| 2015 | None | N/A |

| 2016 | None | N/A |

| 2017 | Eclipx Group** Flexi Cards |

3 5* |

| 2018 | Avanti Finance Latitude Financial Services |

5 2 |

| 2019 | None | N/A |

| 2020 | None | N/A |

| 2021 | Basecorp Finance Hummgroup Bluestone Mortgages UDC Finance |

3 5 3 2 |

| 2022 | None | N/A |

* Programme now owned and operated by hummgroup.

** Now FleetPartners

Source: KangaNews 17 May 2023

The opportunities are not universal but nonbanks believe there is growth to be found in the New Zealand market. For instance, while Bianca Spata, group treasurer at hummgroup, acknowledged that the local credit card market shrank during the pandemic – as customers consolidated debts and increased repayment of credit card balances – volumes are now increasing and this should support growth in this portfolio.

“We believe there is a consistent growth opportunity in Australia and New Zealand, based on the service proposition offered by nonbanks,” Spata explained. “We are actively diversifying our asset base in New Zealand, pushing in particular into secured lending, through the broker market, across transport and construction equipment.”

EMERGING DEMAND

Demand has kept up with growing supply of New Zealand securitisation and issuers report relatively robust outcomes for their public deals. MTF Finance last issued in February this year and Wilson reported that the issuer was very happy with the investor response, which led to a healthy coverage ratio. He also suggested familiarity with the asset class and the MTF Finance brand is growing.

“Our last securitisation deal was very well supported by repeat investors – some of which did not require pre-deal meetings,” Wilson revealed. “We also met some potential new names, a couple of which participated. Our origination and ownership model is not easy to understand but when investors get it they typically find it very powerful.”

Simon O’Connell, executive director and head of structured finance at Westpac New Zealand, added: “Growth was slow for several years after 2010. But investors have gradually attuned to the strength of New Zealand assets and the product has garnered greater acceptance. It has always had a good cash-flow profile and the securities are not heavily structured or synthetic, which adds to confidence.”

“Retail investors cannot get direct access to securitisation, and pricing on the asset class is typically good – which means it offers value in two important areas. In fact, retail – and also bank – investors not generally being active in securitisation means there is less competition and thus particularly attractive pricing.”

Harbour Asset Management is one local firm that has taken securitisation exposures, which Mark Brown, the firm’s head of fixed income portfolio management, say typically provide a compelling risk-reward outcome.

He explained: “We are required to report on whether we are providing value for money to our investors. Retail investors cannot get direct access to securitisation, and pricing on the asset class is typically good – which means it offers value in two important areas. In fact, retail – and also bank – investors not generally being active in securitisation means there is less competition and thus particularly attractive pricing.”

On the other hand, investors are wary of securitisation’s reputation for illiquidity. Brown suggested that the combination of lack of retail sell-down options, relatively thin dealer coverage and a less diverse institutional investor base is enough to convince Harbour the prudent course of action is to treat asset-backed securities as an illiquid asset class – which limits demand to some extent, especially for funds that offer near-term liquidity.

There is also lingering wariness of securitisation in some quarters of the New Zealand market. “The reality is that part of our client base does not want to buy RMBS at all because of memories from the financial crisis, even though New Zealand assets have performed well over many years,” Brown said. “We will always discuss what types of securities make sense with investors but the reality is some just don’t want securitisation.”

MARKET DEVELOPMENT

In a maturing market, New Zealand securitisation issuers suggest investor support across the transaction capital structure is relatively well developed. “We have witnessed growth in the New Zealand mezzanine investment sector, including the emergence of credit funds with specialist expertise,” said Dom Di Gori, group treasurer at FleetPartners. “This is encouraging: senior growth is great, of course, but without mezzanine funding we cannot accelerate overall market growth.”

Spata added: “More mezzanine investors would help grow the market – and it is happening. For instance, we brought our first mezzanine investor into the New Zealand commercial warehouse recently – a local New Zealand fund – following the experience we have had in our Australian warehouses. This type of investment allows us to recycle capital more quickly and therefore grow the book with confidence.”

On the other hand, hopes for the development of a bank securitisation market – and, perhaps even more helpfully, bank asset-liability management book investment in securitisation term deals – have faded in recent years.

Half a decade ago, the RBNZ – in its capacity as prudential regulator – was actively exploring a bespoke securitisation instrument, the residential mortgage obligation (RMO), that banks could use for repo and sell in the open market for funding purposes. However, it put plans on hold when more urgent priorities arose at the start of the pandemic and recently confirmed that the RMO would not be revived at all.

Meanwhile, much of the New Zealand capital market is living under the shadow of another RBNZ initiative: its liquidity review. While this is expected to take a matter of years to complete, it could reshape bank demand for various asset classes and thus fundamentally shift the local issuance landscape.

Wilson said: “The impact of the liquidity review likely will not be material to MTF Finance compared with today’s position because I don’t believe repo-eligibility is a material consideration for our current investors. But market growth has to start somewhere and the proposals in the liquidity review seem to be going in the opposite direction. This is really disappointing, as it could end up being a missed opportunity to stimulate the securitisation market – and indeed the New Zealand capital market as a whole.”

Even so, Dunlop suggested: “We are experiencing something of a virtuous circle, with a number of consistent issuers and supportive investors promoting regular deal flow. We may need to grow the market within the group, though – because we can’t change what we can’t control.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news