Demand factors drive Kangaroo and Kauri evolution

Nearly three decades after the birth of the supranational, sovereign and agency Kangaroo market, the sector has grown and evolved despite multiple changes of demand drivers. Meanwhile, Kauri market development has been impressive but it will have to work through a new challenge to reach its next phase.

Laurence Davison Head of Content KANGANEWS

The first-ever supranational, sovereign and agency (SSA) Kangaroo bond deal – in the strict sense of an Australian dollar transaction covered by local law but issued by an offshore-domiciled entity – priced in 1996, when Korea Development Bank printed A$150 million (US$100.1 million) of three-year notes.

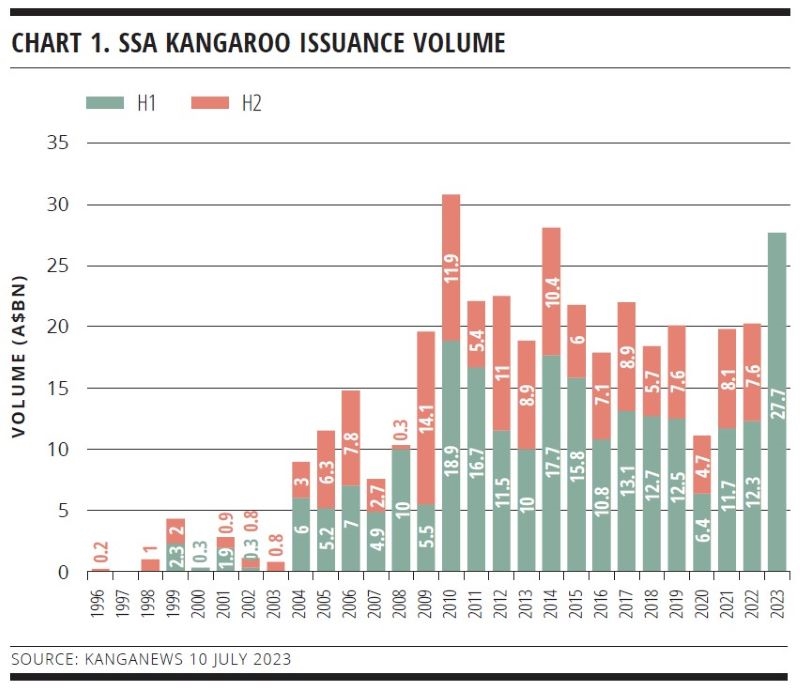

The last few years of the 1990s saw a clutch of names that would become familiar to Kangaroo investors making their debuts, including Asian Development Bank (ADB), European Investment Bank (EIB), KfW Bankengruppe and World Bank. But it was not until 2004 that the sector could truly be said to be a reliable, regular component of Australian domestic market issuance (see chart 1).

A steadily growing market took a significant hit in the wake of the global financial crisis. But annual SSA Kangaroo issuance volume passed A$15 billion for the first time in 2009 and only fell below that level once in the next decade and a half – in 2020, when COVID-19 and its associated fiscal response caused shockwaves throughout global markets.

Australia’s fortune in coming through a decade and a half of economic and market crises relatively unscathed has also helped its capital market grow, including by attracting international capital. Apoorva Tandon, head of Asia syndicate at TD Securities in Singapore, explains: “Fiscal and monetary stability has been helpful to the Australian dollar market over an extended period. While it has at times been a headwind, the growth engine of China has been pretty helpful overall through the fiscal linkage to commodities.”

The current year seems set to produce all-time record SSA Kangaroo volume. The A$27.7 billion issued in the first half is comfortably a year-to-date record and trails only two full years; just A$3.1 billion of second-half issuance will see 2023 pass the all-time record annual volume, printed in 2010.

The consistency of SSA supply in the Kangaroo market is all the more impressive because no buyer base is effectively mandated to buy this product, while the activity of investor groups that do buy Kangaroos has ebbed and flowed based on relative value, outright yield and a raft of other factors.

“There is no ‘natural’ buyer base of SSA Kangaroos as there is in some other markets, like New Zealand or Canadian dollars, where the local banks buy for HQLA [high-quality liquid assets] purposes,” explains Yuriy Popovych, Singapore-based director, debt capital markets at TD. “What’s unique about the Kangaroo market is how internationalised it is: there are domestic buyers but also substantial participation from Asia and Europe.”

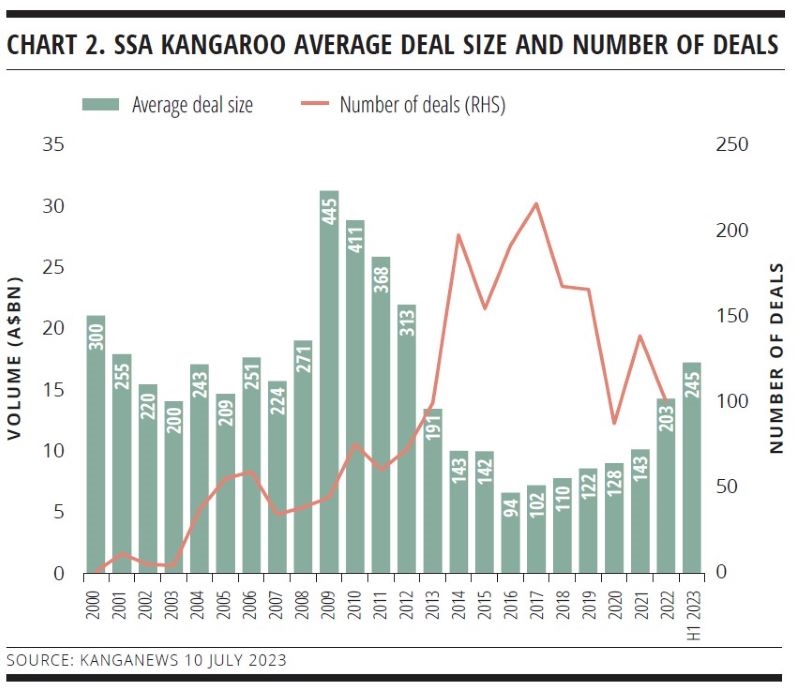

The dynamics of Japanese demand provide a good example of this. For an extended period in the late 2010s, SSA issuance was heavily concentrated in long-dated format – typically 10-year tenor – with flow coming in the form of very frequent, typically small-sized tap transactions.

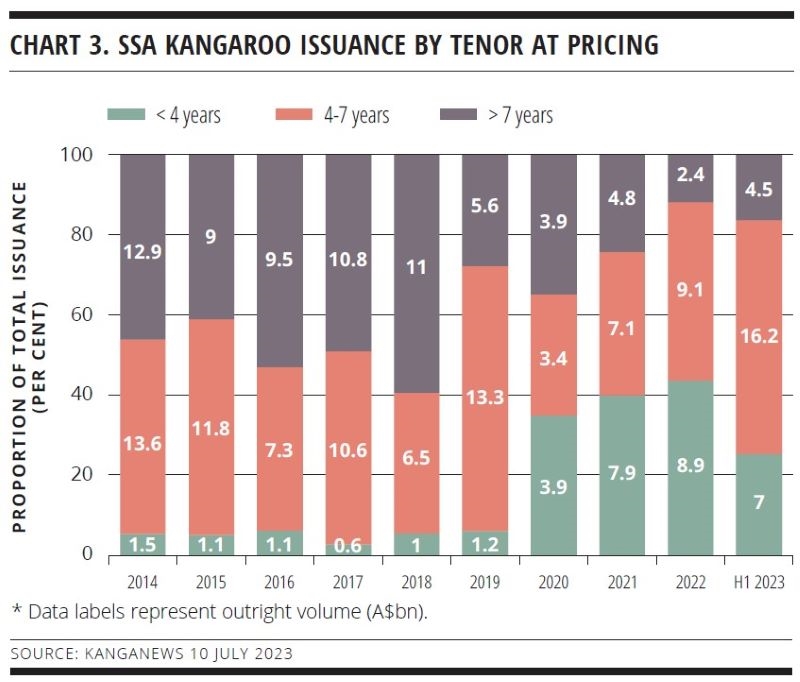

Average deal size fell to less than A$100 million in 2016 while the total number of deals peaked at 215 – approaching one for every working day – a year later (see chart 2). The realignment of Kangaroo buyers away from an investor segment with a specific long-dated bias also reshaped the tenor profile of SSA issuance from 2019 onward (see chart 3).

The value proposition for this specific bid started to unwind as the relative advantage of Australian dollar yield fell over the latter part of the decade. Popovych explains: “This demand was driven by insurance policies sold in Japan and the proceeds reinvested. But since the Australian-US yield differential has collapsed – with the US dollar yielding more – it was inevitable that some of this insurance money would reallocate to US from Australian dollars.”

While he does not anticipate this specific stream of Japanese demand returning to the Kangaroo market in the foreseeable future, Popovych suggests the way the market has moved on demonstrates its fundamental resilience.

“It is a very diverse market by investor type,” he explains. “There are bank buyers and also central banks, asset managers and others. Without a natural buyer base, it is important for one or more investor groups to be aligned with SSAs – whether it be on relative value or another factor – but, equally, such alignment is usually in evidence.”

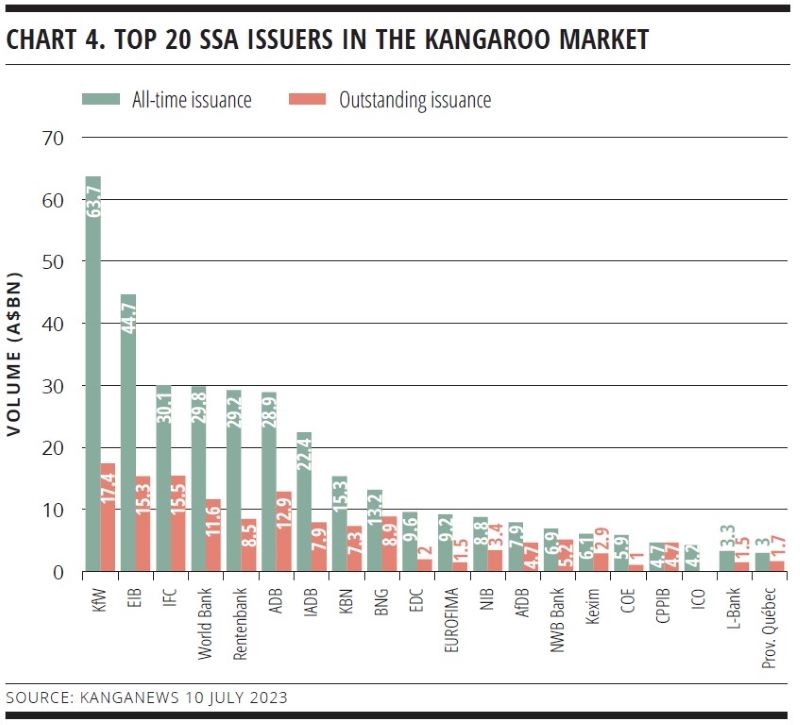

Investor diversity has also promoted issuer breadth in the Kangaroo market. According to KangaNews data, no fewer than 48 SSA issuers have priced Kangaroo bonds in the market’s history, all but eight of them having bonds outstanding as at 30 June 2023.

KfW Bankengruppe is by some distance the largest borrower by total issued, at A$63.7 billion, though six more SSAs have printed more than A$20 billion in total: EIB is the second-largest followed by International Finance Corporation, World Bank, Rentenbank, ADB and Inter-American Development Bank (see chart 4).

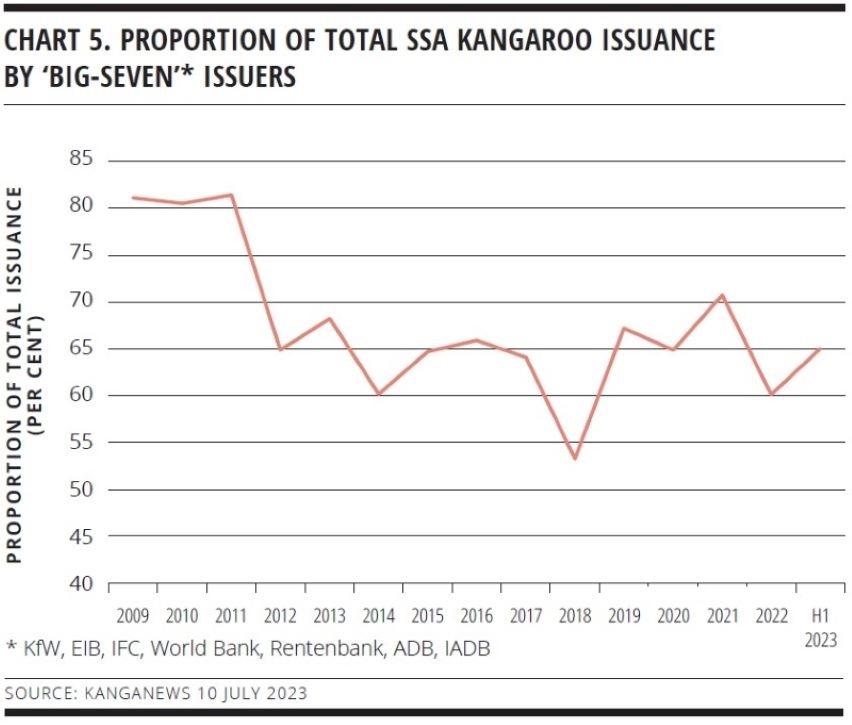

There have been consistent opportunities for other names over the years, however. For the past decade, SSAs outside the top seven have typically provided around one-third of total sector Kangaroo volume (see chart 5), while some issuers have been able to build outstandings quickly. Canadian Pension Plan Investment Board, for instance, priced its debut Kangaroo in August 2022 and increased its outstandings to A$4.7 billion within a year.

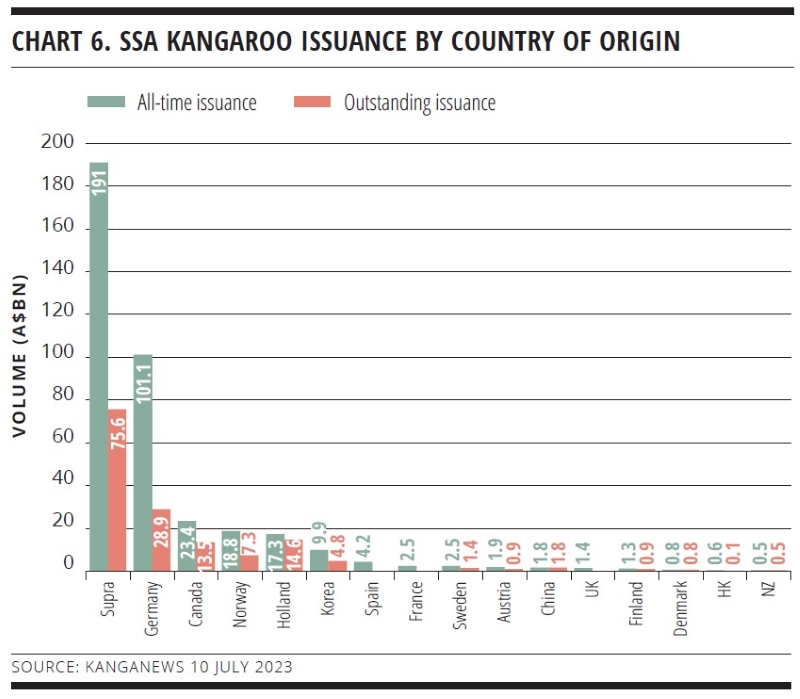

Issuance diversity is also shown by the destination of funds raised in the Kangaroo market. At A$191 billion, supranational issuers represent almost exactly half of all-time SSA Kangaroo issuance while the prominence of KfW and Rentenbank help make Germany by some distance the most active single jurisdiction (see chart 6). But issuers from a further 14 countries have tapped Kangaroo investors, primarily in Europe but also with a prominent Asian and North American flavour.

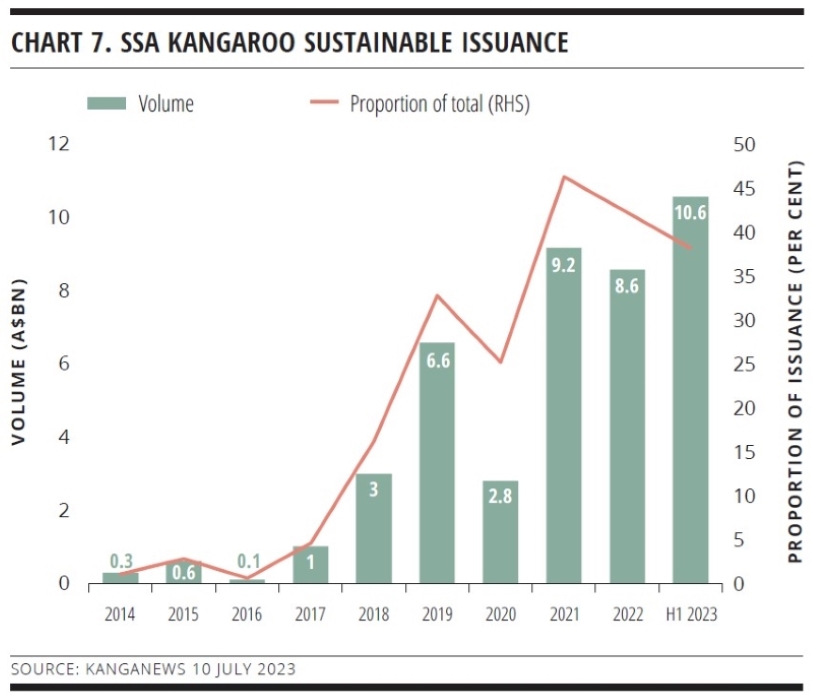

Most recently, the emergence of green, social and sustainability (GSS) bonds has given the SSA Kangaroo market another boost – especially with domestic Australian investors. These accounts are particularly coveted by SSA borrowers because they typically do not appear in the issuers’ deal books elsewhere in the world, thus providing the purest form of diversification.

As with the SSA Kangaroo market overall, it took some time from the pricing of the first GSS deals for the asset class to become a regular fixture of the market. In this case, World Bank printed the first Kangaroo green bond – a A$300 million transaction in 2014 – and, allowing for a pandemic-related slowdown in 2020, issuance started to reach its potential from 2019 (see chart 7).

“It’s apparent to us from every investor conversation we have with the real-money community in Australia just how significant the resources being deployed in ESG [environmental, social and governance] are,” Tandon comments. “Effectively, every meeting has scope to become an ESG meeting. In the absence of a vibrant local corporate market and with limited local government-sector ESG issuance, SSAs have been a big beneficiary of ESG demand.”

Tandon says TD has observed a similar phenomenon with Japanese investors, and signs of it emerging even in areas of the market where ESG has not historically been a major factor. “Some of the Asian official institution accounts – central banks and sovereign wealth funds – have tended to be slow movers in this space but have really evolved over the last 6-12 months,” he reveals. “They may not yet be material investors in Kangaroo GSS transactions, but it is certainly interesting to see what might be the

last part of the market to move in this space starting to catch up.”

Taken together, demand factors highlight a positive environment for SSAs in the Kangaroo space. Popovych points to the market’s flexibility to produce relatively customised solutions for issuers and investors, whereby dealers and investors will work together to find a suitable solution for a particular need on tenor, credit or ESG.

Reliability of demand from one source or another also allows issuers to view the Kangaroo market as close to a strategic issuance option; not, perhaps, on a par with US dollars or euros but definitely a jurisdiction that rewards engagement and a constructive view over the longer term.

Popovych adds: “Issuers have funding targets, of course. But if they can be confident of doing good volume in relatively regular trades, it certainly increases their willingness to meet the market on price. It is harder to do this if the size of the trade is marginal or if the issuer cannot be confident even that an extra 2-5 basis points is going to get volume into a deal.”

The current year has been particularly rewarding, supported by robust secondary turnover – which, Tandon says, provides good foundations for new issuance. “Dealers can show relative value to secondary pricing with a good deal of confidence about getting a transaction away, while still offering competitive funding to the issuer,” he explains. “It’s a win-win, because investors see more value in a new issue when there is a 2-4 basis point concession over buying in secondary.”

KAURI QUESTION

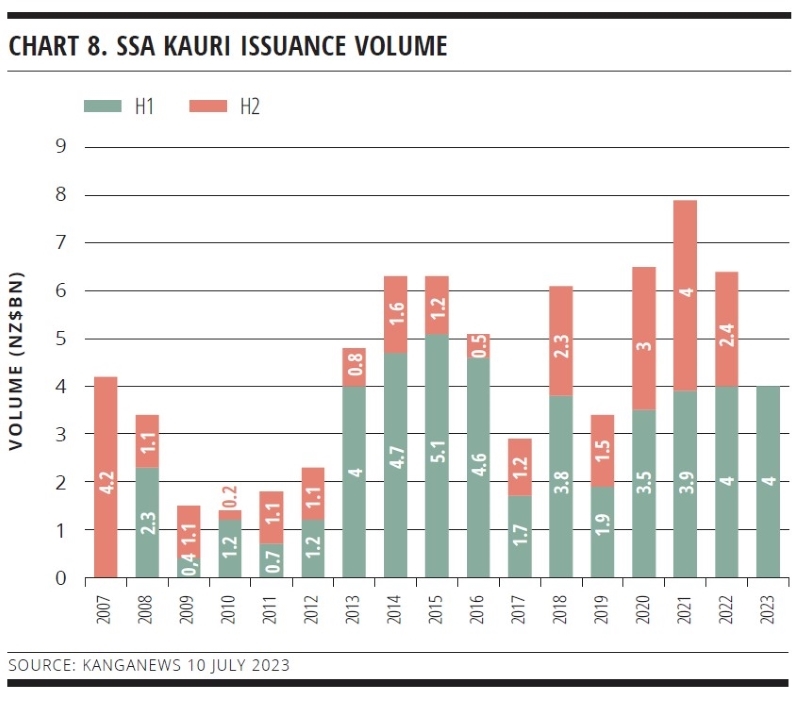

On the other side of the Tasman Sea, the SSA Kauri market is confronting a specifically domestic challenge. The sector’s first deals came about after a change in local liquidity rules encouraged New Zealand’s banks to diversify their holdings – a development that was driven in part by excessive tightness in the New Zealand government bond market. Issuance popped in 2013 and, with just two exceptions, has been greater than NZ$5 billion (US$3.1 billion) every year for the past decade (see chart 8).

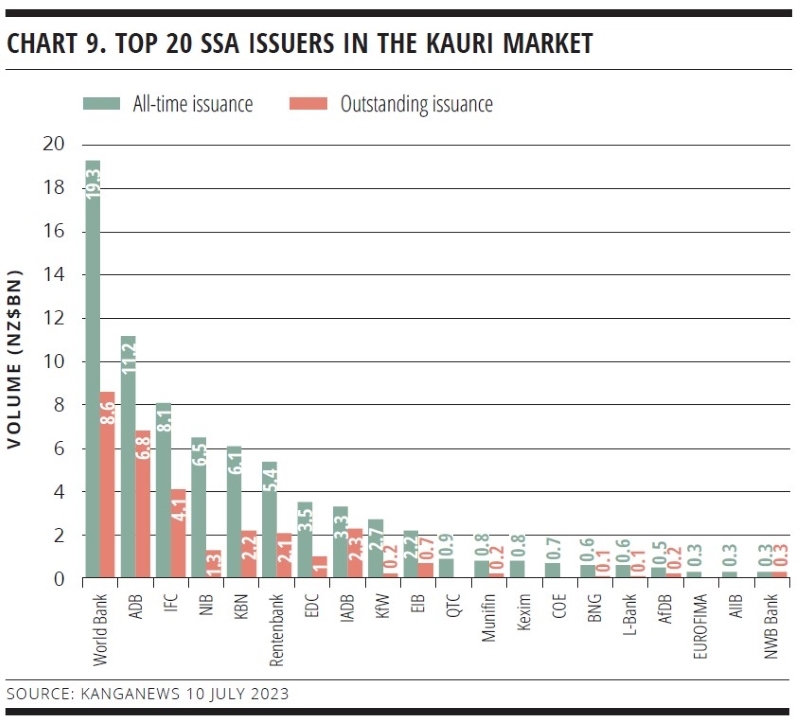

The opportunity set has been a little narrower in the Kauri market than for SSAs in Australia. Six issuers have printed more than NZ$5 billion of Kauris apiece, and these names account for more than three-quarters of total market supply (see chart 9). Even so, 22 SSAs have issued Kauri deals since 2007 and 15 of them had bonds outstanding by mid-2023.

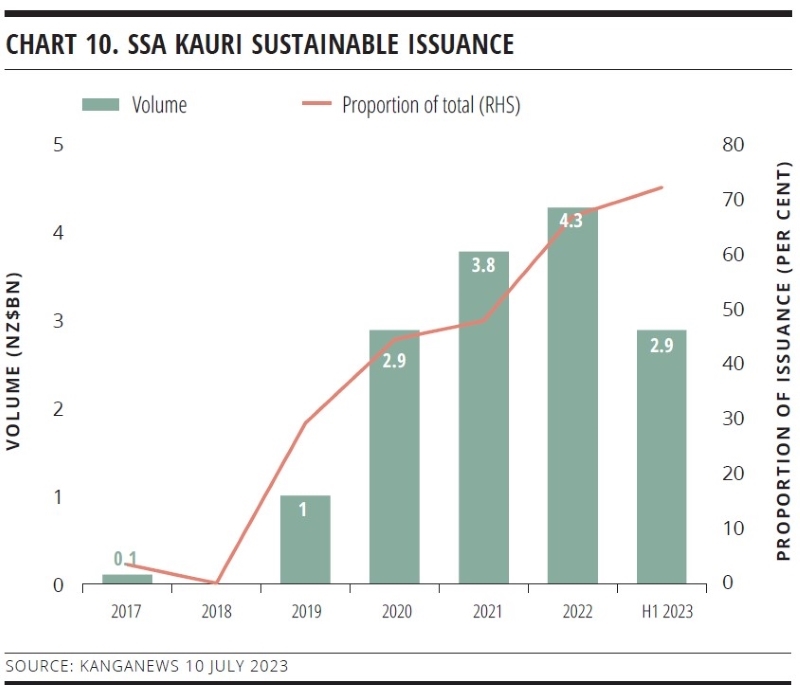

If anything, the role of GSS bonds is even greater in the Kauri market than it is in the Kangaroo. Labelled bonds formed their greatest-ever share of issuance – two-thirds of the total – in 2022 and the level remained stable in H1 2023 (see chart 10).

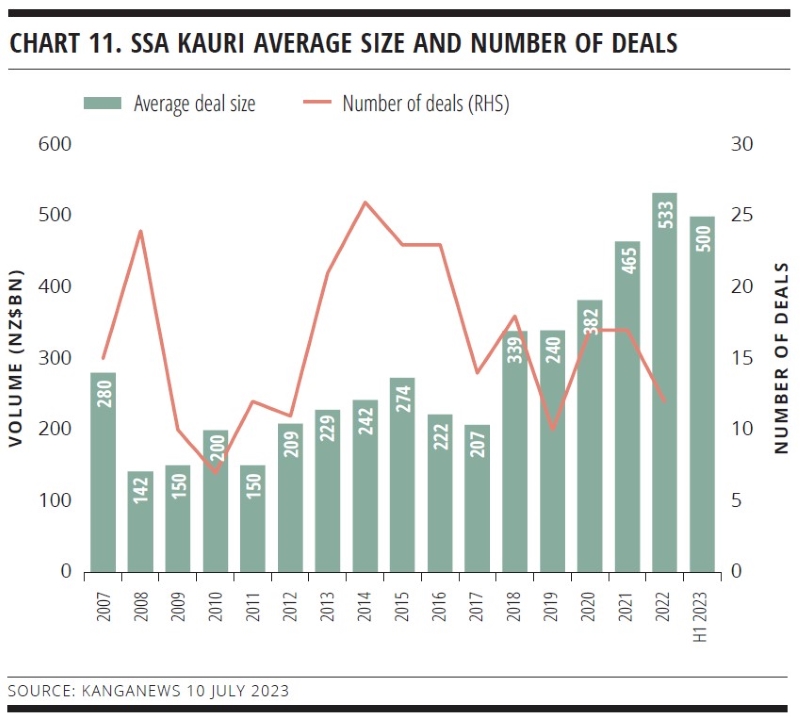

What the Kauri market has yet to develop is the true internationalisation of SSA Kangaroo issuance. Domestic investors, and in particular domestic bank balance sheets, remain not just the biggest buyer group but also the primary driver of deal flow. The absence of the long-dated Japanese bid, for instance, means Kauri volume – along with deal size (see chart 11) – has climbed only gradually and largely in line with local balance sheet growth.

There are hopes, however, that the New Zealand market will find a bigger role in international portfolios. “With rates where they are now including the RBNZ [Reserve Bank of New Zealand] getting close to its terminal rate, we are experiencing more international accounts getting comfortable with New Zealand dollars,” Popovych reveals. “World Bank’s transaction from June this year had roughly 25 per cent international distribution, for instance – which demonstrates that there are pockets of liquidity for New Zealand dollars offshore.”

The challenge comes in the form of a question mark over the core domestic bid. The RBNZ is re-examining its liquidity policy in a process that is not likely to conclude before 2025-26. The uncertainty is problematic enough, but the real fear comes from a consultation document published by the RBNZ in February this year that suggested SSA Kauris may receive less favourable treatment as liquid assets in the new regime.

The risk is that a smaller or, at worst, absent bank bid could deny the Kauri market the critical volume needed to build on its international momentum. But market users are remaining confident despite the uncertainty, based on the view that the RBNZ will not want to weaken diversity in the local capital market. Popovych comments: “The RBNZ review is obviously one of the most significant developments the Kauri market has faced. But it is encouraging to note that the last couple of deals that have come to market have received very strong support from the balance sheet community.”

He continues: “The New Zealand market is relatively small, the relevance of which in this case is that there are fewer asset classes for investors to buy. A really punitive treatment by the RBNZ will inevitably mean fewer deals and smaller volume. But this is why I would be quite surprised if the RBNZ took an action that would take away such an important source of liquidity for domestic investors.”

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news