Domestic high-grade issuers stay ahead of the GSS curve

Australia’s three largest state government bond issuers have all been active in the green, social and sustainability market for at least half a decade, while another peer joined their ranks in 2023 and the sovereign is preparing for a green-bond debut in calendar 2024. Frameworks, programmes and issuance approaches have not been static, however, as issuers seek to meet evolving investor needs and expectations.

Helen Craig Head of Operations KANGANEWS

Laurence Davison Head of Content KANGANEWS

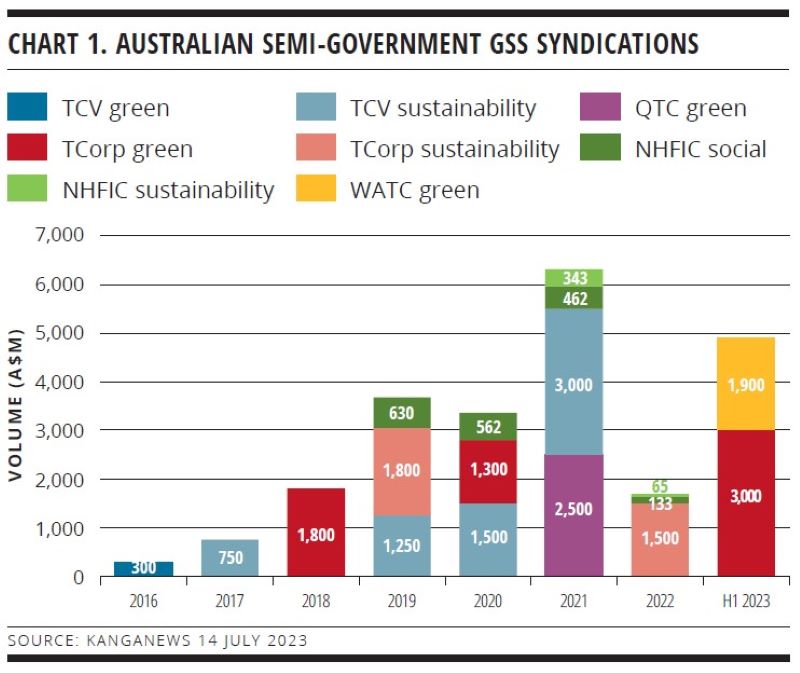

By the end of next year, green, social and sustainability (GSS) bond issuance will be close to ubiquitous in the Australian sovereign and semi-government sector. Treasury Corporation of Victoria (TCV), Queensland Treasury Corporation (QTC) and New South Wales Treasury Corporation (TCorp) debuted over a period of just more than two years beginning in mid-2017, while Western Australian Treasury Corporation (WATC) joined the club with its first green-bond deal in mid-2023 (see chart 1).

Other than state governments, National Housing Finance and Investment Corporation introduced its all-GSS programme in 2019. And, in a long-awaited development, the Australian federal government in 2023 confirmed plans for sovereign green-bond issuance. The Australian Office of Financial Management (AOFM) expects to print its first deal in calendar 2024 (see box on p40).

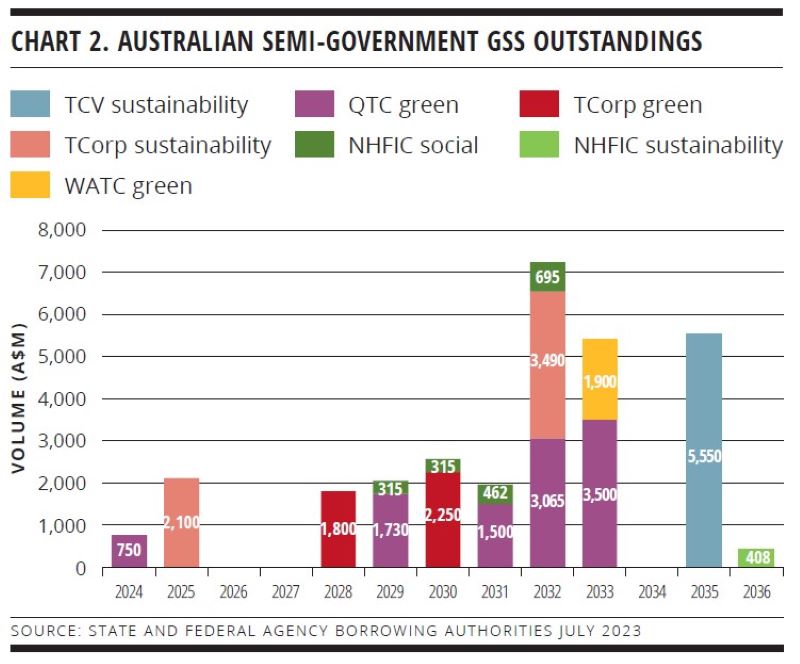

Even so, in many ways the sector is still developing. GSS bonds represent a relatively small share of outstandings across the sector: just A$29.8 billion (see chart 2) out of around A$430 billion of syndicated semi-government benchmark bonds on issue and – for now – none of the A$825 billion of benchmark Treasury bonds.

Issuers have also had to stay in touch with evolution in the GSS asset class as a whole and, in particular, with investor needs and preferences. Notable buy-side focus points include a desire to ensure their capital is making a material difference and ever-growing scrutiny of issuers’ credentials beyond the assets identified for GSS bond pools.

Darren Sloane, executive director, debt syndicate at ANZ in Sydney, explains: “Investors are very focused on the forward-looking nature of Australian government and semi-government frameworks. In particular, we have seen a notable increase in the attention they pay to the additionality aspect – investors’ ability to see and measure the contributions of issuers.”

Issuers report a similar enhancement of investor attention over time. In particular, the buy side increasingly wants to understand the sustainability ambition and achievements of the issuer even beyond the GSS asset pools. This does not make labelled bonds irrelevant, however – instead, state treasury corporations say, it requires closer integration of GSS programmes with the rest of their activities and reporting.

“The feedback we receive from investors is they are keen to understand the organisation at a macro level, in other words how the state is showing leadership and ownership for climate change. Eventually, this filters down to what we are doing at labelled bond level – but this is the end of this process,” says Paul Kelly, head of markets at TCV in Melbourne.

This was a significant consideration for Australia’s newest state government green-bond issuer. Kaylene Gulich, chief executive at WATC in Perth, says the treasury corporation was supportive of sustainability issuance for some time ahead of its 2023 debut but “wanted it to be with all-of-state involvement”. This was a work in progress for some time but reached a tipping point in recent years with a raft of significant state government commitments in support of overall sustainability outcomes.

“We now have a strong, cohesive story that we believe suits engagement with investors, backed by commitments and projects of a scale that is meaningful to the state and for investment,” Gulich told KangaNews in the wake of the May publication of WATC’s Sustainability Bond Framework.

In fact, far from stopping at a GSS asset pool, investors now expect the whole-of-issuer approach to go beyond even the boundaries of a state government. Western Australia (WA)’s economy is concentrated in the resources sector, so the WATC framework includes a section covering “decarbonisation and the mining industry” that acknowledges WA’s “relatively high” per capita carbon footprint and its growth over the past two decades, which it ascribes to “the rapid expansion of the resources sector to service the global economy”.

The framework adds: “The majority of large mining and energy companies in WA, which contribute about half of the state’s emissions, have set targets for net zero emissions by 2050. The WA government is partnering with the state’s mining, energy and manufacturing industries to reduce emissions and support the goal of the Paris Agreement.”

TAILORING A FRAMEWORK

As WATC demonstrates, delivering GSS bonds that meet investor needs nowadays starts at framework level. While the end goal is to produce a marketable product, the first step is to identify the issuer’s own priorities and targets.

“The work we do to create the sustainability framework starts 1,000 by delving deeply into the journey the issuer has taken along the way – in other words, what is material about the issuer’s journey

that it would be appropriate for investors to consider,” explains Bronwyn Corbet, executive director, sustainable finance at ANZ in Sydney. “This includes targets or goals the organisation has already set – such as goals or interim goals to reach net zero – as well as any other material ESG [environmental, social and governance] aspects that are already being addressed.”

After this, the detail of framework development begins. At this point, Corbet says, ANZ examines current investments more closely and discusses whether new asset investments might be needed. Scrutiny of the asset position informs decisions about whether use-of-proceeds (UOP) GSS bonds or sustainability-linked structures would be more appropriate to the specific issuer.

“The most important thing to highlight with high-grade issuers is that they have typically already done a lot of the work they need to do – they are well prepared, and the organisation is fully committed,” Corbet adds.

The sustainable bond market can be broken down into three constituent parts: issuer ambition and progress, investor expectations, and governing standards. None of these has stood still – and Australian semi-government issuers, like others globally, have responded through their GSS issuance programmes.

For instance, Daniel Chandler, Sydney-based head of funding and sustainability at TCorp, notes that since its green-bond debut in 2018 the issuer has continually striven to ensure its framework captures all the core elements required by investors. Over time, this has included updates to align with evolving global standards, highlight New South Wales government initiatives and expand eligible project categories as new criteria have been developed.

“As the sector evolves, standards will continue to rise and investors will increasingly demand more reporting on projects in the asset pool,” Chandler suggests. “Another area of increasing focus for investors is the overall credibility of the issuer, the policies and strategies it has in place and how they will meaningfully contribute to the targets set.”

QTC updated its green-bond framework in May 2021. Even more recently, TCV published a new framework in September 2021, TCorp followed suit in January last year and WATC followed in April 2023.

Kelly tells KangaNews that TCV started its GSS story by elaborating its belief that the state of Victoria is a leader on climate action. The 2021 framework update followed the state government’s publication of an initial climate change strategy – a roadmap to net zero emissions by 2050 – which was subsequently updated to a roadmap for net zero emissions by 2045. The state has also announced interim emissions targets, not only to reach net zero emissions by 2045 but also to reach 70-80 per cent by 2035.

Loading the big gun: AOFM targets 2024 green-bond debut

The news that Australia will enter the green-bond market as a sovereign borrower was long-awaited and – by the time the announcement arrived, in April – widely expected. Detail is gradually emerging on the Australian Office of Financial Management (AOFM)’s issuance plans but the process is still in its early stages.

Speculation about issuance of Australian sovereign green, social and sustainability (GSS) bonds has been ongoing in the local capital market ever since the May 2022 federal election produced a government with a commitment to overhauling national climate policy. The AOFM conducted preparatory work but repeatedly stated that the green light could only come from government.

The federal treasurer, Jim Chalmers, flipped the switch on 21 April this year when, following the government’s second investor roundtable, he confirmed plans to introduce a sovereign green-bond programme.

The May federal budget formalised the commitment, making A$8.3 million (US$5.5 million) over four years – and A$1.3 million annually on an ongoing basis – available to establish and maintain an issuance platform designed to “raise capital for environmental and climate change related programmes”.

Kelly adds: “On top of this, toward the end of 2022 we became the first Australian state government to publish TCFD [Task Force on Climate-Related Financial Disclosures]-aligned climate-risk disclosure. This has cemented the government’s commitment to climate change and drives how future projects might look. This, in turn, will determine the volume of suitable assets that become available over time to support labelled bond issuance.”

Updating issuance strategies can lead to broadening the range of GSS issuance a borrower uses. TCV and TCorp debuted with green-bond transactions while NHFIC’s initial issuance was in social-bond format, but all three have since added sustainability bonds – which combine green and social UOP – to their funding mix.

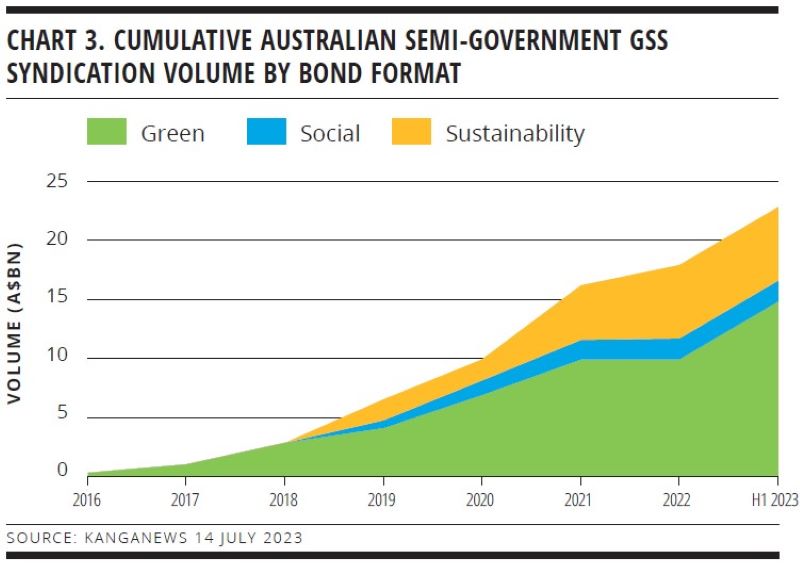

Social and sustainability bonds in aggregate made up roughly one-third of Australian government-sector syndicated GSS issuance by the end of June 2023 (see chart 3).

TCV issued green bonds before having a framework in place, but expectations have changed and the issuer published its framework in preparation for adding sustainability bonds to its issuance menu. The framework lays the foundations for issuance in any of the GSS formats and TCV believes it has the inherent flexibility to accommodate market evolution.

“The programme and assets contained within it are reviewed annually but the framework itself is robust and meets our needs in the current environment, and therefore it should not need to be reviewed,” Kelly suggests. “Obviously, if standards change or the environment evolves, we will consider whether it is appropriate to review the framework.”

Sustainability-bond issuance is not necessarily a natural progression, though. Jose Fajardo, head of funding and liquidity at QTC in Brisbane, argues that investors understand that the majority of the Queensland government’s operating expenditure is on social services such as health, education, social welfare, housing and community services without the issuer needing to fund social assets using labelled bonds.

“QTC chose a standalone green-bond programme, which is consistent with investor feedback we have received for a preference for this thematic type of issuance,” Fajardo continues. “Our approach to ESG has been to highlight and support projects and assets with a positive environmental benefit to the state through our green bonds.”

The AOFM has confirmed that its plans are to issue green – rather than social or sustainability – bonds.

Sloane agrees that all approaches are valid based on the issuer’s priorities or the specific investor preferences it is seeking to satisfy. “As to whether QTC and AOFM will decide to broaden their frameworks down the track, it is fair to say that, for now, both issuers are very comfortable with an explicit focus on green labelled issuance,” Sloane tells KangaNews. “We have seen issuers,

for example TCorp, move from a green to a sustainability bond framework, so there is a precedent for broadening the programme. But I don’t expect a change like this in the foreseeable future.”

Whatever label or labels issuers select, Corbet says “the bar is being raised higher all the time” in the GSS market. However, she also suggests the primary driver is issuers themselves. “It is more likely to be issuer strategy, based on a macro perspective of a state’s business or economy, that evolves over time. This is what we aim to highlight to investors. It means things like more ambitious targets or developments in accordance with new and evolving legislation.”

ENGAGEMENT AND AMBITION

Even so, investor engagement is still a vital part of the process. For instance, Kelly says TCV undertakes a continuing investor engagement programme and, when it came to designing and reviewing its framework, listened to investor feedback on the type of labelled bond, the duration of transactions, and the type and diversification of assets that went into the pool.

Sloane adds: “We carry out extensive work with issuers and investors to ensure their sustainable financing frameworks speak to their goals and commitments, while at the same time making sure they are best-in-breed for investors. It is a balancing act and comes together via general industry engagement as well as more bespoke investor work in the lead up to and throughout the development of the framework.”

Enhanced investor engagement continues in the deal execution process. For instance, WATC conducted an extensive roadshow in Asia – including Japan – Europe and Australia ahead of its debut green-bond deal. The issuer was rewarded with a more than three-times oversubscribed book from more than 65 participating accounts, including new names to the WATC programme and others returning after more than a decade (see p8).

“At all stops on the WATC roadshow there was very robust investor engagement, from domestic accounts as well as in Asia and Europe,” Sloane says. “Highlighting this, a quarter of the final book was allocated to offshore investors.”

This could grow further. Although only 6 per cent of the WATC transaction was sold to investors in Asia, Sloane says engagement in the region was high. “If interest at the roadshow is a good indication, I expect to see greater participation from Japanese accounts in WATC green bonds over time,” he concludes.

There are still challenges. One is that, while the global perception of local climate policy environment has improved, Australia may still be making up something of a credibility deficit on the low-carbon transition – some of which comes down to its economic fundamentals.

A credible response is possible, however. Sloane explains: “Australia has a large hard-to-abate focus and this has an impact on ESG views. As a mining state, WATC made a point very well on its roadshow: without the mining industry the state cannot manufacture the goods we all need – for example, batteries or solar panels – to support the development of a more sustainable, carbon-neutral environment.”

Perhaps the biggest issue of all is the same one the semi-government sector has faced since it issued its first green bonds nearly a decade ago: identification and verification of suitable assets for UOP financing. This does not necessarily mean the assets are not already on state balance sheets, just that corralling them for labelled financing can be a time-consuming and difficult process.

Kelly says: “Government is a very big beast and one of the challenges for us has been to communicate with the departments that own the assets to ensure they understand their role in the government’s push to net zero. As a disaggregated lender, we lend to the government and are therefore at least one step removed from the asset. Our challenge – though it is not insurmountable – is to work as closely as we can with the various departments to continue to identify new and appropriate assets we can include in our pool.”

Demonstrating the achievability of this task, Fajardo points out that QTC has grown its green-bond pool in the water infrastructure space in recent years, by adding the South-East Queensland Water Drought Resilient Network – a unique, climate adaptation water supply asset that provides many options to make drinking water available in and around the most populated part of the state.

“With the state government’s announcement, in September 2022, of the Queensland Energy and Jobs Plan, QTC will work with its clients to identify eligible projects and assets that may be brought into our green-bond pool,” Fajardo continues. “We have received feedback that investors prefer newer projects and assets. At the same time, we will continue to monitor developments in the GSS debt space and remain agile as investor and market expectations evolve.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news