Harmoney spots opening to print debut public securitisation

Harmoney took advantage of ongoing limited supply of securitisation – and good-quality, diverse credit in all formats – in New Zealand to print its debut public deal. The issuer now plans to be a regular securitisation issuer at home and in Australia, while its arranger says the New Zealand market remains conducive to new supply in various formats.

Harmoney priced NZ$200 million (US$118.3 million) in Harmoney NZ ABS 2023-1 Trust on August 17, with BNZ as sole arranger and joint lead manager alongside Commonwealth Bank of Australia. The deal is the public first securitisation transaction for the New Zealand-headquartered nonbank lender, which also operates in Australia.

Harmoney launched in 2014 offering peer-to-peer lending funded by retail investors. Harmoney lends for three, five or seven years, with five- and seven-year agreements being the preference for New Zealand customers. Most loans are repaid within two or three years, according to Harmoney’s Auckland-based chief executive and managing director, David Stevens, as borrowers aim for higher repayments than are calculated for a relatively longer contractual term.

The average loan size is around NZ$28,000, with funds most commonly put to use for home renovations, car purchases, debt consolidation and “life experiences” such as education and medical expenses.

Harmoney was a peer-to-peer lender until 2020, by which time it was originating about NZ$10 million a week – more than New Zealand’s retail investor cohort could fund even though this platform had 20,000 investors at peak. “Trying to find retail demand that sits across all the different risk profiles was complicated,” Stevens adds.

More recently, Harmoney it has attracted funding from three of the big four banks and three mezzanine funders, and privately placed a A$105 million (US$67.2 million) securitisation in October 2021. “We aim to refine the funding mix, and get better pricing and more demand as we do future deals,” Stevens says. “We are pretty excited to be on the securitisation journey now.”

The funding model may have changed but public securitisation was always one of the end goals. “When I came on board at Harmoney four years ago it was always the intention that we would term out warehouses with securitisation deals. We felt the time was now right,” Stevens says.

The Australian private placement in 2021 was part of a plan to lay the groundwork for public issuance. Stevens says it “greased the wheels”, including initiating a ratings process to test that systems could manage transfers to facilitate a new trust. “We built up more warehouses after that transaction, so it is now a matter of terming out those warehouses – ideally on a regular basis.”

The ambition is to issue asset-backed securities annually in New Zealand or Australia. “Hopefully we will be able to do at least one or two a year across the group,” says Stevens.

EXECUTION APPROACH

BNZ’s Auckland-based head of capital markets, Mike Faville, says the Harmoney deal drew a broad range of investors across the capital stack, including accounts from Australia and New Zealand. The NZ$100 million A1 tranche, which priced at 165 basis points over one-month BKBM, was 1.7 times oversubscribed. As is common for an inaugural issuer, Faville says tranches lower than A1 were pre-placed.

During deal marketing, Stevens says enquiries mostly dwelt on Harmoney’s business, its loan products, arrears and processes around losses. Loans through Harmoney are unsecured, although the lender has recently launched a secured auto product. “We brought new investors into the lower-rated rated notes and there were questions about credit analysis, how the business performs on an ESG [environmental, social and governance] front and what the structure looks like,” Stevens tells KangaNews.

Source: KangaNews 21 August 2023

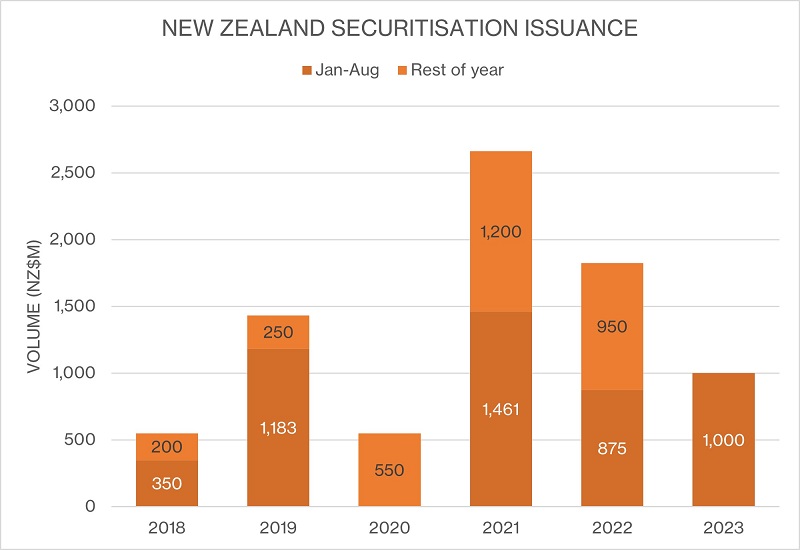

According to Faville, the Harmoney deal represents some welcome dealmaking in a year of limited securitisation volume in New Zealand. New issuance has now reached NZ$1 billion (see chart), so supply could match last year but is unlikely to pass the record set in 2021 – especially as further flow does not appear to be imminent.

“There are no mandates out there in New Zealand dollars at the moment, but the environment is constructive and positive for future issuance – investors are receptive,” Faville says. “Australia is a market investors and issuers look to for reference, and it is continuing to print and mandate quite strongly. This suggests conditions are right to follow track here.”

The Harmoney deal was well-timed, Faville adds. “The investor community is looking for product that suits and has good credit enhancement.”

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

Related news