Elevator going down: office landlords’ tougher funding task

Alarming headlines about office vacancy rates are the most visible sign of a downturn in the commercial property space. While cyclical and structural factors are weighing on the sector, though, investors and rating agencies continue to back the sound fundamentals of its Australian issuers.

Jeremy Chunn Editorial Consultant KANGANEWS

Australian commercial property companies – developers and asset owners – are caught in a four-way stretch under which hybrid work practices, rising debt cost, resets to valuations and looming projects are putting strain on forecasts. As the big names in the office space eye their financing options for the years ahead, investors are keeping a watching brief for tremors in gearing covenants and any opportunities to pick out alpha in what is predicted to be a protracted period of volatility in the sector.

Despite the obvious pressures, however, investors and analysts tell KangaNews the sector is likely not heading into a repeat of the aftermath of the global financial crisis, when the S&P/ASX200 Australian Real Estate Investment Trust Index lost more than 75 per cent in value between November 2007 and February 2009.

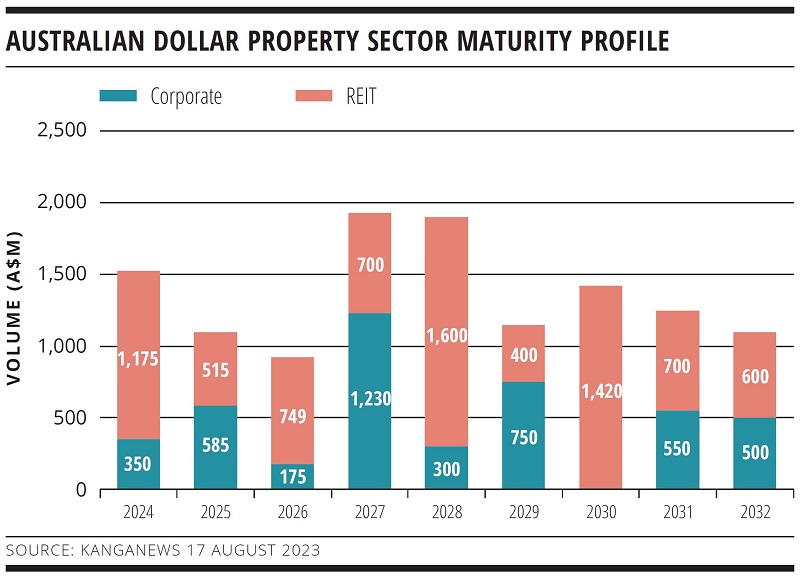

Property developers and REITs play a significant role in the Australian dollar corporate bond market and 2024 is a significant year for redemptions (see chart). The maturity profile is weighted toward retail property next year, including a A$200 million bond from Australian Prime Property Fund Retail and A$225 million of Shopping Centres Australasia Property Group paper.

Some businesses have been taking steps to shore up balance sheets. Pauline Chrystal, portfolio and ESG manager at Kapstream Capital in Sydney, points to the sale by Dexus of a 26 storey tower in the Sydney CBD in June, at a 17 per cent discount to book value – a building that was 15 per cent vacant at the time. But she argues this is reflective not of forced divestment but a sector in which many players are operating on comfortable credit metrics with fair headroom before they hit ratings triggers.

Net demand for office space in city centres has always waxed and waned. Sydney experienced dips in 2002-04, 2009-10 and throughout the pandemic. In the recession of the early 1990s, a downturn in demand that saw vacancies reach 20 per cent tallied with a long winter of corporate failures. The current situation is relatively acute, however. Property Council of Australia’s measure of national CBD office vacancies stood at 12.8 per cent in July this year, the highest level since 1996.

Against this backdrop, interest rates have moved aggressively in the past 12 months, which feeds into the capitalisation rate – the sector’s equivalent of yield – along with rental growth, especially as financing from before the hiking era continues to roll off.

Shares in property groups such as Dexus, Vicinity and Scentre are already trading at discounts to net tangible assets, and Aldrin Ang, director, corporate ratings at S&P Global Ratings in Melbourne, expects office asset prices to fall further if June valuations for unlisted issuers are a reliable comparison.

Dexus offered some guidance on 30 June when it devalued its office portfolio by 7.7 per cent. Western Asset Management Melbourne-based senior credit analyst, Sean Rogan, believes Dexus – even though it has “the biggest portfolio of prime and A-grade assets” – will likely announce further downgrades in the months ahead, of perhaps 10-12 per cent, depending on the economic outlook. However, he also notes that occupancy is holding up well and rent increases are not unachievable.

“We are not getting a massive 20 per cent correction that speculation in the market may suggest,” Rogan says. “Australian REIT issuers are typically in the single-A minus to triple-B range, they own prime buildings and seem to be benefiting as tenants upgrade to take advantage of juicy incentives. It is the peripheral assets that are taking the brunt of softness in the market.”

Pain should also be diluted for diversified REITs, analysts argue, where office buildings are offset by better performing logistics, industrial or retail assets. Over the next 1-2 years, says Moody’s Investors Service Sydney-based vice-president and lead analyst for the A-REITs sector, Saranga Ranasinghe, offices will likely be the worst affected of the property subsegments she covers. “There are quite a few challenges for the office real estate subsegment,” Ranasinghe says. “But high ratings are reflective of asset quality and financial policies. We also feel these issuers have some levers – which is why we are maintaining the stable outlooks on all of them.”

Despite the challenges faced by the sector, Moody’s has not taken any negative actions on issuers in Australia with office exposure, which it rates from A2 to Baa2. Ranasinghe explains that gearing thresholds allow ample headroom against issuers’ debt-to-asset covenants and internal targets.

“They can weather quite a bit of a reduction in asset values and still not trip parameters set for each rating or even come close to where the covenants are,” she says. “Interest coverage ratios will be affected, though these too are still at levels appropriate for the assigned ratings.”

By contrast, in the past 12 months S&P has changed the outlooks on Australian Prime Property Fund Commercial and AMP Shopping Centre Fund to negative from stable, and on Dexus Wholesale Property Fund to stable from positive. It has also downgraded its rating on Australian Prime Property Fund Retail by one notch, to BBB+, and on QIC Property Fund by two notches, also to BBB+.

STRUCTURAL SHIFT

A major unknown for the office sector is how much of the current weakness is cyclical – the result of A

an economic downturn – and how much reflects a long-term change in working patterns and the rise of hybrid or remote working. Occupancy in some offices on a day-to-day basis can be as low as 45-50 per cent, says Helen Mason, fund manager and senior credit analyst, fixed income at Schroder Investment Management in Sydney.

Mason does not believe reversion is imminent. “Employers can’t just demand people come back into the office when they have seen that a hybrid model has worked really well – employee expectations have changed,” she says. “On the other hand, some organisations are trying to incentivise their people to come back. This is a more balanced strategy.”

Quality buildings in good locations are in demand, and assets that tick sustainability boxes for energy efficiency are even better. Vacancy rates for office space of the issuers rated by Moody’s is around 5-6 per cent, much lower than the entire market. “Bifurcation is the key word right now,” Ranasinghe says. “A flight to quality can help prime assets maintain occupancy levels. Anything that is well located and is a good asset will be able to retain or attract tenants better than a secondary asset.”

Developers are aware of this trend. For instance, when Lendlease completed the three towers that make up the Barangaroo site in Sydney, the developer delivered more than floor space. Premium tenants were attracted by a new precinct with cafés, bars, ferries, restaurants, high-end shops, end-of-trip facilities, a running track and even a harbour swimming cove.

Ultimately, investors still believe premium-grade assets will see their valuations lowered – just not by as much as B-and C-grade buildings. The contagion effect will cast a shadow over all addresses. “One has to think that, at some point, we need to see negative revaluations,” Mason suggests. “From a credit trading perspective, the market is less likely to mean revert until we have seen meaningful asset revaluations.”

The road back may come through discounting. When it comes time to renew leases, tenants of landlords whose portfolios are at lower occupancy levels will be inclined to negotiate greater incentives to stay, such as funds toward a fitout or discounts on rent. The effect on income can offset CPI-linked rent escalation structures.

Mason describes incentives around 30-40 per cent as a possible inflection point that may indicate that “face rents” need to come down. “Landlords can’t keep pumping up incentives forever and at the same time maintain face rents as high as they are,” she suggests.

While the hybrid working story is yet to play out, property owners should probably not expect the future to be like the past. “We are not expecting occupancy to go back to levels seen before the pandemic, because we think flexible working is here to stay,” Ranasinghe says.

NEW ISSUANCE

A main component of the near-term challenge is that sentiment has changed so quickly that the construction pipeline has delivered a glut of supply – and may continue to do so for some time yet (see box).

On the other hand, Australian debt investors insist they are still open for business – at the right price. Rogan comments: “We are hoping we will get more issuance in the remainder of the financial year, after the current reporting season. We have been starved of decent primary issuance for the past year, given market conditions were volatile and rates have been rising quickly.”

Any new bond that presents an appropriate spread and tenor will likely appeal to investors. “It might be a matter of whether issuers are willing to pay more than terms available in the loan market,” Chrystal says. “We don’t have any concerns about the ability to refinance, in any case.”

Refinancing will come at a cost, though. “In the past, the REITs have been able to access very cheap funding, but now they are going to have to start paying up,” says Mason. Bonds for GPT, LendLease, Dexus and Charter Hall are all trading wider than the quality of their portfolios might imply, Mason says. “There is a theme here, which is the risk the market is attaching to them. If they want to get a deal done, I think they would succeed but they would have to pay up for it.”

Overall, balance sheets are in good shape, gearing levels are not topping out and financial-crisis-era financial engineering is not evident. “I think this is more of a re-basing,” Mason says. “I’m absolutely keen to invest in Australian REITs but my biggest concern at the moment is probably spread-widening risk associated with certain issuers. This possibly has further to go.”

Chrystal adds: “We are comfortable with the Australian office players, especially the larger names. What we are worried about is headline risk and a general wariness of the REIT sector – this is resulting in those bonds trading a little wider than run-of-the-mill corporate names.”

Supply dynamics not yet offsetting negative sentiment

Over time, the office market should adjust even to a fundamental shift in working habits, by easing supply of new facilities. The challenge at present is that the change in sentiment is well ahead of what was a fully-loaded development pipeline.

A reasonably sure way to navigate a period of loose demand is to restrict supply. However, according to the Property Council of Australia, about 1.1 million square metres of new office space is in the pipeline: 354,000 square metres is planned in Sydney, 273,000 in Melbourne, 164,000 in Brisbane, 87,000 in Perth and 77,000 in Adelaide.

Another trend is for upgrades to add floorspace to existing structures. For instance, the 45,000 square metre AMP Capital tower in Sydney is reemerging as the 89,000 square metre Quay Quarter Tower after a makeover by Multiplex. Seven minutes’ walk away, the 44 story Grosvenor Place is half empty.

The market will be tested by new supply, though there are some offsets. In the Sydney CBD, for instance, Saranga Ranasinghe, vice-president and lead analyst for the A-REITs sector at Moody’s Investors Service, says most of the new supply is pre committed. Ranasinghe comments: “The supply that is coming online is a lot more green than the existing stock, so the buildings are attractive. But attracting tenants, even to these buildings, is becoming really hard in this environment. We are more concerned about Melbourne than we are about Sydney.”

On the other hand, the investor consensus seems to be that while the local office market is facing a challenging period, the narrative is being influenced by – rather different – circumstances offshore. Sean Rogan, senior credit analyst at Western Asset Management, says: “The news flow from offshore – the US particularly – has been really bad. There are some eye-watering stats about vacancy rates and stranded assets in New York. This has muddied investor sentiment toward the sector in Australia.”

Some larger offshore investors are directing Western Asset to steer clear of new REIT assets for the time being – swayed, Rogan suspects, by their gloomy view on the global sector. “We make an argument defending the Australian REIT sector but in some cases it has not resonated enough for investors to change their minds,” he reveals.

Many observers expect debt issuance and equity raising will become harder. Some issuers are already showing signs of gearing pressure. Options available may involve divestment strategies or issuance of convertibles or hybrid instruments. “Those with short-dated debt books also run refinancing risk,” says Aldrin Ang, director, corporate ratings at S&P Global Ratings. “The response could be to change to secured from unsecured financing, and maybe bank loans instead of the bond market – which is arguably more volatile at this stage.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Sydney Airport adds euro benchmark to domestic outcome to deliver ideal blend

Sydney Airport navigated a significant upturn in market volatility to deliver a massively oversubscribed and competitively priced return to the euro market, the deal group says. European investors responded positively to the issuer independent of its recent successful return to Australian dollar issuance, with the domestic deal not even relevant as a comp for euro pricing.