Autos proliferate

The Australian auto lending market is undergoing a similar structural shift to that experienced by the nonprime mortgage lending market a few years ago: a wide-scale withdrawal by bank balance sheets and a proliferation of new and existing nonbank lenders. Auto-backed securitisation issuance is booming as a result.

Laurence Davison Head of Content KANGANEWS

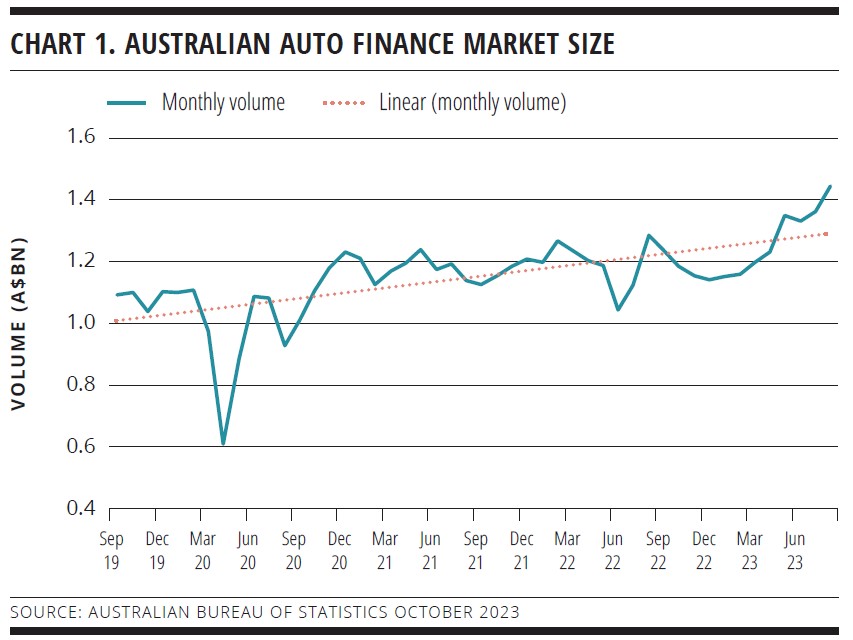

A clutch of factors have combined to drive growth in Australian auto securitisation. The first is the sheer size of the market. Australian Bureau of Statistics data show the auto loan market continues to grow, reaching a record A$1.4 billion (US$897.4 million) of monthly volume in August 2023 (see chart 1). According to Finder, in 2021 roughly 14 per cent of Australians – about 2.7 million people – had a car loan.

This volume pales in comparison with a local mortgage market that is roughly 20 times the size of auto finance. But a much greater share of Australian vehicle loans is now being written by lenders that source the bulk of their funding in the securitisation market. In fact, the seeds of the new-look Australian auto asset-backed securities (ABS) market were sown in 2021 with the disposal of the two books that had dominated issuance in the sector by the banks that owned them.

In September that year, Allied Credit acquired Macquarie Bank’s auto dealer finance business, which had previously issued ABS from the Smart programme. Shortly before the end of the year, Westpac Banking Corporation sold its vehicle dealer finance and novated leasing business to Angle Auto Finance, a portfolio company of private equity heavyweight Cerberus Capital. The book, which issued ABS under the Crusade banner, was originally owned by St.George Bank and transitioned across to Westpac as part of Westpac’s financial-crisis-era acquisition of the smaller bank.

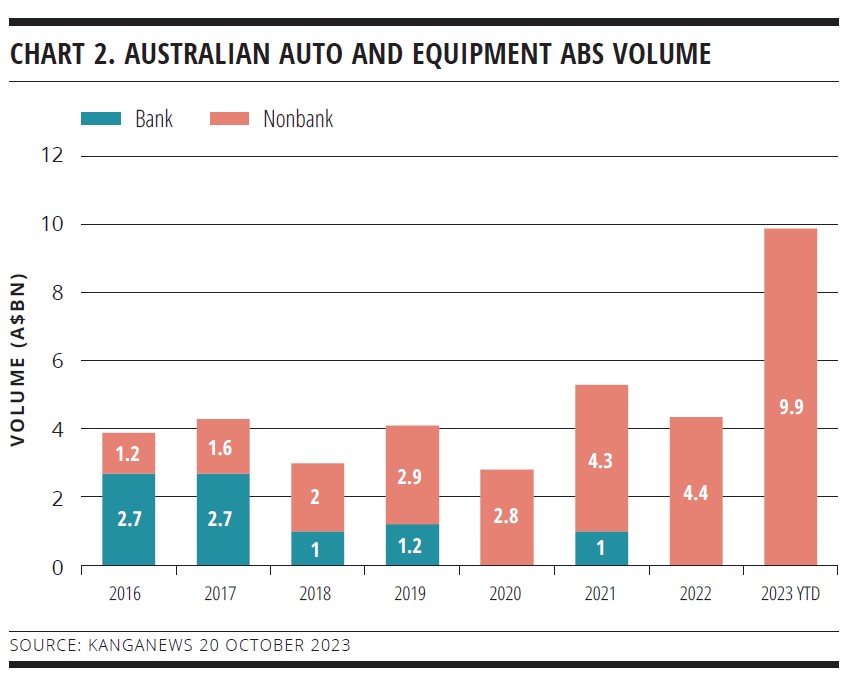

In 2022, however, the impact on Australian dollar auto ABS issuance was minimal. The absence of bank issuers was notable but not unprecedented (see chart 2) while volume – at A$4.4 billion (US$2.8 billion) – was largely in line with historical trends.

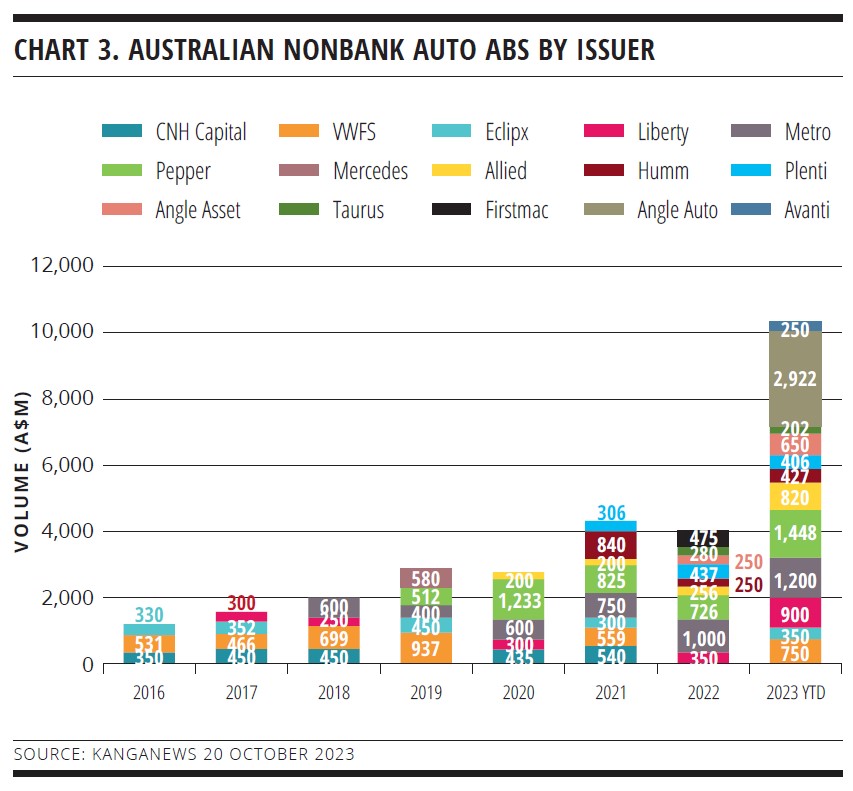

Everything has changed in 2023. By mid-October, issuance volume was approaching the A$10 billion mark and had already smashed the record for full-year issuance, with more than twice as much supply as any previous year (see chart 3).

Just as notably, the range of active issuers has exploded. No fewer than 12 nonbanks have printed auto ABS in Australia in 2023, compared with eight or nine in 2021 and 2022, and just a handful in prior years.

The divestment of the Crusade and Smart books is not a coincidence, and the reasons behind the sales points to a strutual shift toward a more diverse and larger auto ABS market. In the same way as capital rules written or updated in the wake of the financial crisis have made mortgage lending outside the prime space less appealing to banks, auto lending is also no longer the natural territory of banks.

Sharad Baheti, director, securitisation origination at National Australia Bank in Melbourne, tells KangaNews the cost of point-of-sale compliance had become prohibitive for banks in the auto sector while capital requirements also weigh against authorised deposit-taking institutions as lenders.

The consequences are similar to those experienced in the nonconforming mortgage market. James Austin, Firstmac’s Brisbane-based chief financial officer, explains: “Nonbanks will always seek to participate where banks are either unable or unwilling to lend, and in the case of autos the capital requirements for banks are very high. Autos is not a straightforward space for nonbanks, either – we have to fund the first-loss piece and commissions, which are quite material – but banks have to overlay this with capital adequacy requirements on 100 per cent risk-weighted assets. It is just not efficient for them.”

There is another incentive for nonbanks to increase their presence in the auto market. At the same time that bank lenders were, in general, pulling back from the auto space the same lenders were cranking up the competitive pressure in the mortgage market. Ultra-cheap funding available during the pandemic era allowed banks to offer prime mortgages at rates the nonbank sector simply could not compete with.

While the nonconforming mortgage space is still primarily a nonbank stomping ground, the slump in prime volume for these lenders left many nonbanks struggling to maintain overall origination volume and confronting business contracting as a result.

In this environment, it is no surprise that many nonbanks took their main skills – sound credit risk pricing and superior service, including decision time – to the auto market, seeking growth in a more fertile space.

Broadly, five types of nonbanks are now competing for auto loan volume. There are the rebadged bank books under their new ownership: Angle Auto Finance, the brand that has taken on the old Crusade auto book, and Allied Credit, the new owner of Smart. Then there are lenders with an established presence in the auto market but which have seen the opportunity for growth, perhaps most prominently Liberty Financial, Metro Finance and Pepper Money.

New entrants fall into two types: those with established presences in other sectors and new-found auto ambitions – like Avanti Finance and Firstmac – and businesses, like Plenti and Taurus, that have been established in recent years.

Finally come the longstanding captive financiers. Volkswagen Financial Services is a regular issuer in the Australian securitisation market and Mercedes-Benz brought a single deal in 2019. But much of these lenders’ funding is sourced elsewhere: Mercedes and Toyota Finance Australia, for instance, are regular issuers in the Australian MTN market.

LENDING CHANNELS

Origination comes through three channels. Novated leasing allows customers to finance their vehicles through employer schemes, with the employer typically having an arrangement with a single lender. Car buyers can also source finance at point of sale through a dealer, or independently – typically through a broker.

Lenders say all three points of contact for borrowers – employers, dealers and brokers – have good reasons to support diversity in sources of finance. The most significant developments in car sales that could weaken dealers’ business proposition.

Baheti explains that brands are starting to sell direct to the consumer. For instance, Tesla does not typically use dealerships and Mercedes has moved away from the dealership model to an agency model. Hyundai is selling its Ioniq electric vehicle (EV) range via an online presence only. Baheti acknowledges that “the jury is out” on whether this approach will maintain traction as supply constraints ease, but it still provides an obvious motivation for dealers to try to shore up their value proposition.

One way of doing so is to have access to reliable point-of-sale finance outside the captive lenders. “Dealers value lenders like us because we are independent, which means we are relatively indifferent about what brands the dealer wants to sell,” explains Steven Mixter, group treasurer at Angle Auto in Sydney. “Dealers want us to succeed because they view us as a natural complement to captive financiers.”

In fact, lenders say, dealer finance is now often largely indistinguishable from the broker model. The dealer will have access to a panel of lenders and can offer the customer a choice based on price and service. Some nonbanks believe the change of ownership of the old bank books has accelerated this transition.

Peter Riedel, Liberty’s Melbourne-based chief financial officer, explains that Westpac and Macquarie effectively “owned” the dealer market prior to the 2021 book sales – and therefore dominated the retail space – because they had exclusive arrangements with dealers. He argues that the change in ownership, from banks to private equity, has provided a further incentive to spread the net wider when sourcing financing options.

“Dealers want access to diverse lenders because they are seeking funding certainty for their customers,” Riedel explains. “Larger dealers in particular want to have a panel of lenders to choose from – the bottom line is that they want to make sure the finance enables the sale rather than getting in the way of it.”

Market sources suspect different lenders will focus their activities – and thus find varying levels of success – in one or more of the origination channels. For instance, Baheti predicts Allied Credit and Angle Auto will ultimately secure the bulk of market share in the dealer space. On the other hand, Riedel sees potential for the longer-established nonbank names, like Liberty, as dealers seek diverse options. Some lenders – including Liberty – have no presence in novated leasing, while Angle Auto does not play in the broker channel, in part to avoid crossover with its sister company, Angle Asset Finance.

There is little doubt, however, that the market is big enough and has sufficient sources of demand for credit to support lender diversity on an ongoing basis. This is without even considering the potential for specialist types of lending – of which EV finance is perhaps the most intriguing (see box).

EVs add a new avenue for auto ABS

Electric vehicles (EV) uptake is responsible for a growing share of Australian vehicle sales. The scale to support regular asset-backed securities (ABS) issuance is not there yet but dedicated EV tranches should soon become a regular feature of the local market.

In 2023, EVs comprise roughly 8 per cent of all new cars sold in Australia. This is four times the level just two years ago and market users are confident the growth represents the early stages of a long-term transition in buyer preferences and behaviour.

For instance, speaking at a Clean Energy Finance Corporation (CEFC)-KangaNews roundtable in September, Ellen Liang, co-founder and general counsel at JET Charge in Melbourne, said: “We know from global comparisons that 5 per cent is the tipping point at which disruption becomes inevitable – so we are past the point of inevitable disruption.”

SUPPLY AND DEMAND

This will inevitably mean more auto ABS supply. For instance, Baheti estimates that Allied Credit and Angle Auto alone can between them conservatively expect to generate A$500-600 million of new loans on a monthly basis, which he expects to translate into roughly A$5 billion of loans being distributed into capital markets each year. The pair is jointly already close to this level: Angle Auto will price at least A$2.4 billion of ABS in 2023 – some of it privately placed – while Allied Credit has a little further to go, having issued more than A$800 million by mid-October.

With a clutch of other active players, 2023’s auto ABS market volume of close to A$10 billion may be the baseline for future years – assuming market conditions and investor demand remain supportive.

There is already appetite for the auto product among traditional securitisation investors. James Donovan, portfolio manager at Challenger Investment Management in Sydney, tells KangaNews: “We certainly expect the auto ABS market to grow, and we are backers of this growth. Challenger has supported a number of new market entrants as an early-stage warehouse funder in mezzanine and select senior positions, through to supporting private placements and inaugural public issuance. Some of these new entrants have subsequently become repeat public issuers and we believe others will follow this path. Issuer diversity in the securitisation market can only be a good thing.”

There are plenty of reasons why a wider set of investors could find auto ABS appealing. Credit quality is typically good and the bulk of issuance is coming from nonbank lenders with long track records in autos or, if not, in other types of credit. Investors appear to be comfortable with the idea of issuers porting their credit skills from – typically – the mortgage sector to autos.

Donovan comments: “Existing nonbanks already have treasury teams that are comfortable with securitisation funding and investor expectations. This provides comfort to Challenger, because securitisation knowledge and experience is largely transferable between asset classes. Meanwhile, lenders created from bank divestments will bring in new hires – usually experts who are already well known in the industry.”

He adds: “It is also not the case that diversifying businesses just bring staff across from their mortgage teams. They are typically fairly well resourced and willing to hire new, specialised management and sales teams.”

Adding to the appeal, auto ABS typically offers decent yield pickup for relatively short weighted-average life. Concerns investors may have about secondary liquidity in Australian securitisation should be offset to at least some extent by a product that amortises over 1-2 years.

“Auto ABS should be a good place to start for investors that are new to securitisation or to nonmortgage securitisation,” Mixter suggests. “The transaction structures are pretty straightforward and the collateral is car loans to mums and dads, and tradespeople – it is simple risk to understand. Plus, the ABS structures pay off quickly.”

But take-up in the domestic investor base is still a work in progress. Geographic investor diversity is no bad thing but it is notable that some deals have experienced much stronger demand from offshore, where many buyers have greater familiarity with nonmortgage ABS. Angle Auto’s debut transaction – a A$900 million ABS priced in April – had 80 per cent international distribution, for instance.

Mixter says: “We would love to build out the real-money investor base in Australia. Traditionally, the senior piece of the capital structure was supported by banks because of the committed liquidity facility. This is not available anymore, so issuers can’t really rely on that bid – though, to be fair, banks still play a role in supporting the market. Longer term, issuers should be trying to build a strong Australian real-money bid for the product – and there is no reason for there not to be one.”

Riedel adds: “We are now talking to investors that are very familiar with auto ABS. It is a very well understood and well supported asset class. These investors view Australia as an attractive location for diversification, so our product makes a lot of sense to them.”

BUILDING FAMILIARITY

By contrast, Firstmac’s debut auto ABS – a A$475 million deal priced in November 2022 – found a primarily domestic investor base. “A number of the investors that participated were known to us but had never bought auto ABS before,” Austin reveals. “They did so because we fully underwrite and the auto product we offer is prime only. I think this demonstrates that more investors will look at this market but that it needs tiering to develop fully.”

Austin believes the changing of the guard in the auto lending market has left something of a vacuum in the funding space, in the sense that the Crusade and Smart programmes used to provide a de facto benchmark price and this has not yet been re-established. There is also no tiering within the sector, Austin continues – no established delineation of a prime or nonconforming auto ABS – and pools are often mixed bags of auto, equipment, solar and other loans.

“The market needs to evolve, including the development of tiering and the emergence of a benchmark issuer,” Austin concludes. “This benchmark issuer would need to have volume and also prime, underwritten credit.”

Market participants are confident the sector will evolve in a positive direction. Riedel comments: “There has not been much auto ABS issuance until recently, whereas at least four issuers will now be issuing auto ABS more frequently – and there will undoubtedly be new entrants, too. This makes it much more worthwhile for investors to assess the asset class.”

This could entail price tightening on a relative basis, specifically relative to the primary margins offered by residential mortgage-backed securities (RMBS). Riedel points out that the Smart and Crusade programmes typically printed tighter than RMBS and “there is really no reason” for nonbanks not to achieve the same outcome. He suggests it might take some time to get there, however, as investors will “quite reasonably” want to experience consistent performance.

But increased supply, from a larger number of issuers, should be enough to produce results in and of itself. Mixter tells KangaNews: “From a capital markets perspective, it is great to see a wide range of auto ABS issuers in the market. Ultimately, it should become a self-fulfilling prophesy in the sense that the more product investors see, the more willing they are to do the work on the asset class.”

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news