SSA Kangaroo volume passes all-time record but eyes turn to 2024

Supranational, sovereign and agency issuance in Australian dollars has had a knock-out year, with new supply surpassing an annual record that had stood for nearly a decade and a half. Supply has resumed after a particularly acute mid-year lull, but intermediaries’ attention is now turning to next year as the new-issuance ground looks less fertile in the near term.

Kathryn Lee Senior Staff Writer KANGANEWS

A substantial relative-value opportunity for investors and attractive cost-of-funds relative to overseas jurisdictions carried the supranational, sovereign, and agency (SSA) market to new heights in the first half of 2023.

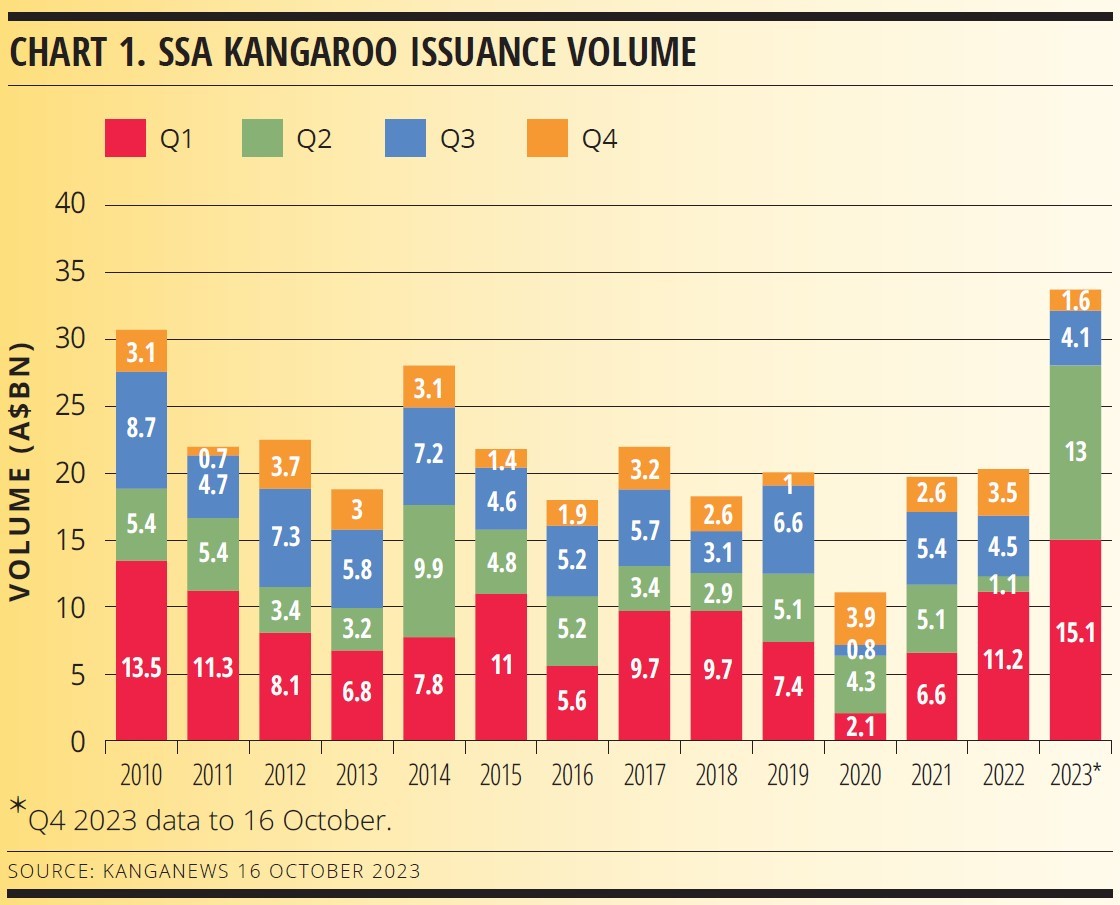

By the end of March, A$15.1 billion (US$9.7 billion) of SSA Kangaroos had priced – the most ever even for the traditionally busy start to the year. Q2 almost maintained the pace, and while the market slowed during the European summer – an expected and regular phenomenon – supply was enough to push 2023 year-to-date volume past the previous full year record by early September (see chart 1).

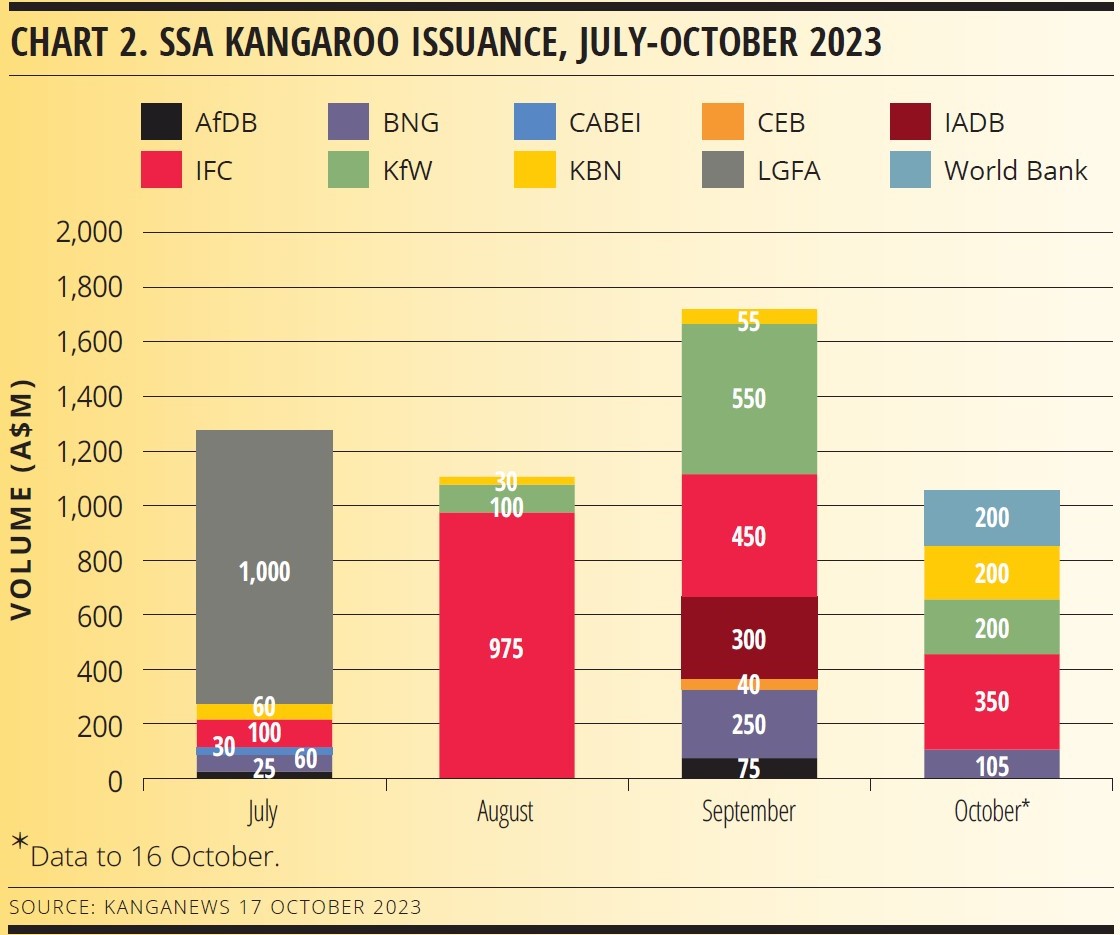

Intermediaries do not expect an issuance bonanza going into year end. While a positive September for deal volume was maintained in the first half of October (see chart 2), deal flow has been solid rather than spectacular. Lead managers suggest near-term factors have swung against the SSA sector in Australian dollars.

The main factor is a very familiar one approaching the end of the calendar year: the bulk of SSA issuers are close to complete on their annual issuance tasks and, in the absence of significant impetus to pre-fund – and thus manage carry over the holiday period – simply do not have much reason to return to market.

For example, a European Investment Bank update says that by October it had only €1 billion (US$1.1 billion) left of a 2023 funding task that had seen it issue nearly €49 billion. While it is not unfeasible that it might choose to do some of this in Australian dollars, it is more likely to wrap up the year’s issuance in core markets. This story is largely repeated across the European SSA complex, intermediaries confirm.

While SSA issuers printed a clutch of benchmark Kangaroo deals in September and October, these were typically in the A$200-400 million range.

New Zealand Local Government Funding Agency is the only international SSA to print a deal of A$1 billion or more so far in H2; there were two such deals in Q2 and four in Q1.

SPREADS COLLAPSE

Further direction of what is left of SSAs’ 2023 funding needs to the Australian dollar market is likely to be hindered by less conducive technical market conditions. The biggest impact, leads say, is the collapse in SSA relative value. Earlier this year, SSA paper was notably attractive relative to local sovereign bonds in particular, promoting domestic participation.

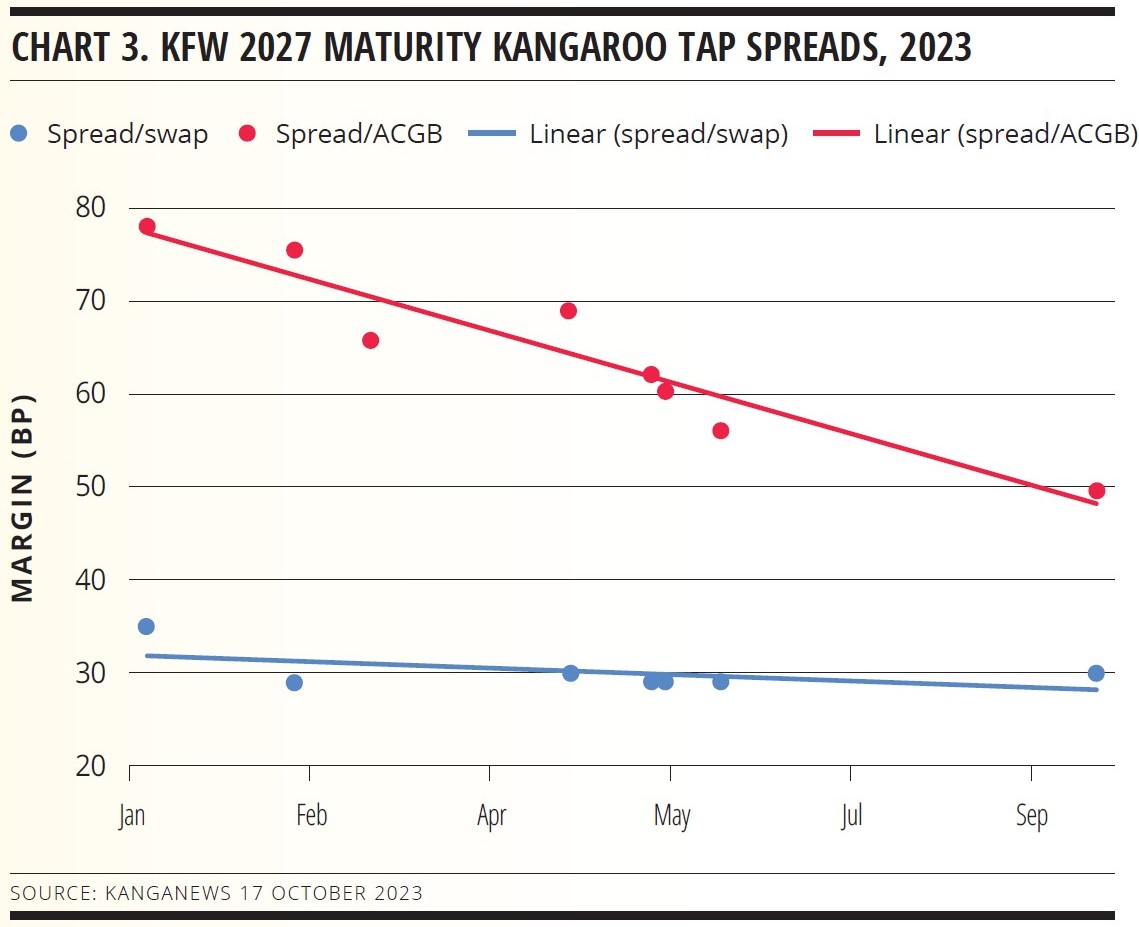

Intermediaries say SSA swap spreads have tightened by 40-60 basis points over the course of the year. Pricing results from regular issuers confirm this: KfW Bankengruppe’s 2027 Kangaroo taps, for instance, have paid a gradually declining premium over Australian Commonwealth government bonds over the course of 2023 (see chart 3).

“It is a material drop from where it has been,” says Cameron Lofstedt, executive director, DCM syndicate at UBS in Sydney. He adds that declining relative value has led to SSAs being less favoured by some investor types.

Harald Eikeland, director, debt syndicate at RBC Capital Markets (RBCCM) in Sydney, confirms the investor make-up has shifted. “We have found transactions are more dependent on offshore demand,” he says. “This ties into the swap spread story – when swap spreads are wide investors can buy SSAs at a large spread to, in particular, semi-government bonds. Domestic accounts are really motivated by this."

By mid-October, demand for new SSA Kangaroo issuance – while still in evidence – was largely focused on international accounts.

Domestic buyers typically participate on a relative-value basis while offshore buyers tend to be more focused on outright yield, explains Liam Orr, Sydney-based analyst, debt capital markets at RBCCM.

“There has been a bifurcation in the SSA market between domestic and international investors,” he tells KangaNews. “Offshore accounts have driven primary transactions in the last 3-4 months, whereas domestic investors – which bought a lot of SSAs earlier in the year – are generally comfortable waiting on the sidelines and being selective in primary offerings.”

For buyers focused on outright yield, buying SSA bonds is still quite attractive provided they remain convinced that the end of the Australian global central tightening cycle is in sight, Orr adds.

Eikeland tells KangaNews Japanese life insurance investors have been notably visible in the sector, especially those with natural Australian dollar demand. He explains: “The accounts that sell Australian dollar product are motivated by the elevated yield, and many central banks also continue to see value. On the other hand, Japanese investors that swap into yen tend to come and go.”

The sense in the intermediary community is of pockets of demand rather than a solid, ongoing bid. This is because even the Australian outright yield story is not quite as gold-plated as it was early in 2023. At the beginning of the year the Australian dollar yield curve – particularly at the front end – was considerably higher than elsewhere. Hence the flurry of SSA issuance in the 3-5 year part of the curve: nearly A$9.5 billion of the A$13.5 billion priced in Q1 was at tenor of five years or shorter.

Now, however, the front end offers a lower yield than the US. Oliver Holt, Singapore-based head of origination and debt syndicate at Nomura, says there is some bid for longer-dated Kangaroos as there is a yield pickup in the longer end. But he warns that the sell-off in fixed income around the end of Q3 – of more than 10 basis points in two weeks – means it is not a clear decision to buy duration, even for higher yield.

“If an investor has a desire for duration there is some extra inducement to buy Australian dollar 10-year paper versus US, but it is not without the risk of a continued sell-off,” Holt points out. “Some accounts are buying the dip, but we are not seeing an en masse buying of duration in the Australian market in any meaningful way.”

Lofstedt adds that recent volatility in the face of what has otherwise been a positive year for bonds might also convince some investors to rest on their laurels as year-end starts to loom, staying out of transactions as a result.

“The rhetoric from central banks is clearly ‘higher for longer’ – this message has been repeated by the US Federal Reserve and the Bank of England at the start of October, while rates have continued to sell off,” Lofstedt says. “Investors have had a good year – especially in comparison to 2022 – and when conditions get volatile it would not be unexpected if they put the brakes on and were more selective to protect performance into year-end.”

Adding to the challenges is the emergence in 2023 of a new-issue premium for SSA transactions. Holt says this had previously not been a feature of the Australian market but estimates it was about 3-6 basis points during the first few months of the year. This was an inducement to buy the early-year deals – Holt believes it supported the record volume – but if it is baked into Australian dollar investor expectations it becomes another hurdle to clear in less conducive market conditions.

“It is no surprise that investors will buy bonds if issuers offer a premium, but it was not previously a meaningful feature of the Australian dollar SSA market,” Holt suggests. “The start of the year was coming off a rocky period and issuers were concerned about meeting funding programmes, so they paid a premium. From that point onward, it was like a mental threshold where each deal was successful and encouraged more issuers to do it.”

NEW YEAR OUTLOOK

Now that most issuers are at the end of their annual funding programmes they have backed away from providing a concession on new deals. But Holt believes the premium will likely reappear in the new year when volume once again becomes the main game – particularly as early indicators suggest market conditions may be at least somewhat challenging.

Since July, 10-year US Treasuries have sold off by 110 basis points, Holt explains. Low issuance volume makes this a less pressing consideration, but if the market reopens in January in an ongoing elevated yield environment, with issuers needing to kick off new A$20-50 billion funding programmes, Holt expects investors in general will expect concessions before they offer significant volume.

Another banker says while issuers might say they expect issuance to return to normal, this is unlikely. The argument goes that most issuers will have large funding programmes to begin the new year in an environment where accessing duration has become harder. As a result, issuers could be forced into 2-5 year tenor and will need to start paying a concession to get volume done even there.

Holt is not ruling out a slight pickup in Kangaroo SSA activity in November and December. It is not likely to be huge in scale, but in addition to possible supply from Washington-based issuers such as World Bank and International Finance Corporation – which operate on July-June funding years – he also thinks it is plausible other issuers may decide to pre-fund for 2024. He comments: “By the time we get to November and December, if there are issuers that have the ability to pre-fund, I think we will see a sudden change in mentality around new-issue premia. If issuers can get money through the door at a sensible concession, they will take it. This does not mean five back-to-back SSA Kangaroo benchmarks before the end of the year, but there could be a small activity pickup.”

Overall, however, the expectation is clearly that SSA Kangaroo issuance will remain slow until the new calendar year. But the volume of supply from early 2023 may not be an outlier. In fact, Orr says the success of 2023 is leading some issuers to seriously consider increasing their share of Australian dollar funding.

“Off the back of how strong 2023 was, some issuers have indicated they may seek to allocate more of their funding tasks to Australian dollars,” he says. “This will of course depend on market conditions but it is a positive development for the Kangaroo SSA market.”

AUD PROMINENCE RISES

Holt is also optimistic. He says the volume printed in 2023 was a positive development and while he does not think another record year in 2024 is the base case, he does anticipate an ongoing healthy and diverse market. “I think borrowers will start the year with the intention to do larger trades,” he continues. “The emergence of newer borrowers like CPPIB Capital and return of less frequent names like Export Development Canada puts Kangaroo issuance on the agenda for global borrowers, and I think we will see further new participants that are keen to make a good entrance.”

Holt says the development of Australian dollar issuance from global financials also bodes well. “Banks like Santander and Credit Agricole are now approaching the market with the right format – Kangaroo documentation – which sets the scene for continued activity from this sector,” he says.

No matter what plays out with pricing dynamics, Eikeland says elevated yield will be an ongoing and positive feature in the new year. “It is difficult to predict whether January will be as busy as it was this year,” he comments. “However, with yields being where they are it is clear bonds are back. A seven-year supranational offering 5 per cent return, even against a backdrop of recession fears in the global economy, is something an asset manager can buy and earn a substantial return.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

Quantum leap for Canadian provinces as Québec smashes Kangaroo record

Investor diversity, relative value and the growing status of the Australian dollar market lined up for Province of Québec as it shattered the record volume for a Canadian province Kangaroo transaction. The A$1.35 billion, 10-year print was nearly four times larger than any previous deal from the sector – a record that had stood for a decade.