Australian dollars a good fit for MHCUK’s growth ambitions

Following its debut in the Kangaroo market, Mitsubishi HC Capital UK spoke to KangaNews about its plans for Australian dollar issuance as it seeks global growth. The scale of Australian dollar benchmarks and competitive pricing sent the issuer home with an outcome it hopes to build on with further future issuance.

Mitsubishi HC Capital UK (MHCUK) is a UK-based nonbank financial institution. It covers a wide spectrum of financing with a focus on autos but additional specialities in consumer and asset finance. The issuer printed its A$350 million (US$223.8 million) debut Kangaroo on 30 November, offering three-year bonds at 155 basis points over semi-quarterly swap (see box). MHCUK’s parent, Mitsubishi HC Capital Inc, guarantees the bonds.

Deal info and execution analysis

Mitsubishi HC Capital UK (MHCUK) navigated a noisy market backdrop during its marketing process, which included several other live deals in the market along with the Australian Securitisation Forum’s annual, two-day conference. It roadshowed in-person in Hong Kong, Singapore, Melbourne and Sydney.

Deal summary

Issuer name: Mitsubishi HC Capital UK (MHCUK)

Issuer rating: A-/A3

Issue rating: A- (S&P)

Transaction type: senior-unsecured Kangaroo bond

Pricing date: 30 November 2023

Maturity date: 7 December 2026

Volume: A$350 million (US$223.8 million)

Book volume at pricing: A$655 million

Margin: 155bp/s-q swap

Indicative margin: 160-165bp/s-q swap

Number of investors in book: “more than 45”

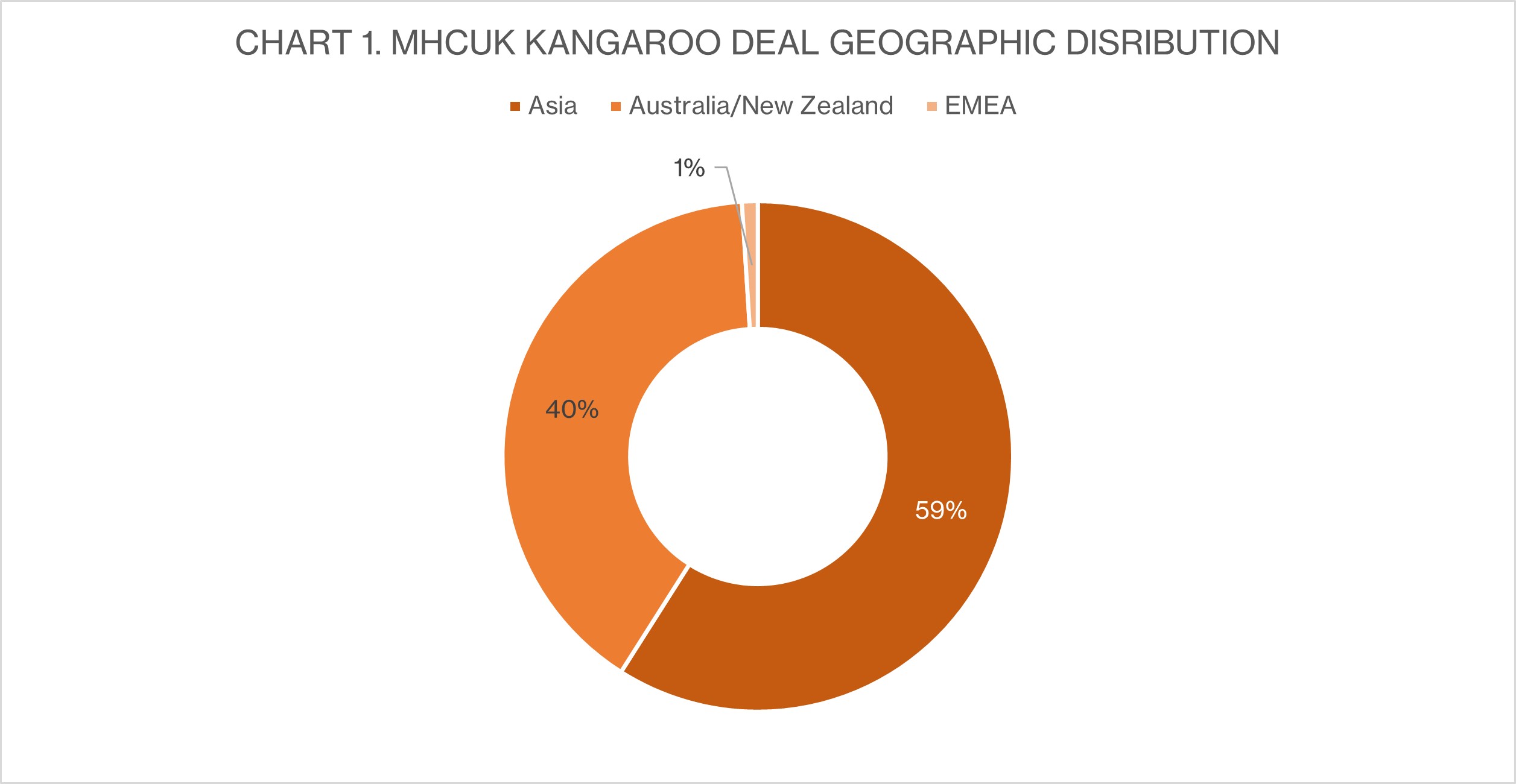

Geographic distribution: see chart 1

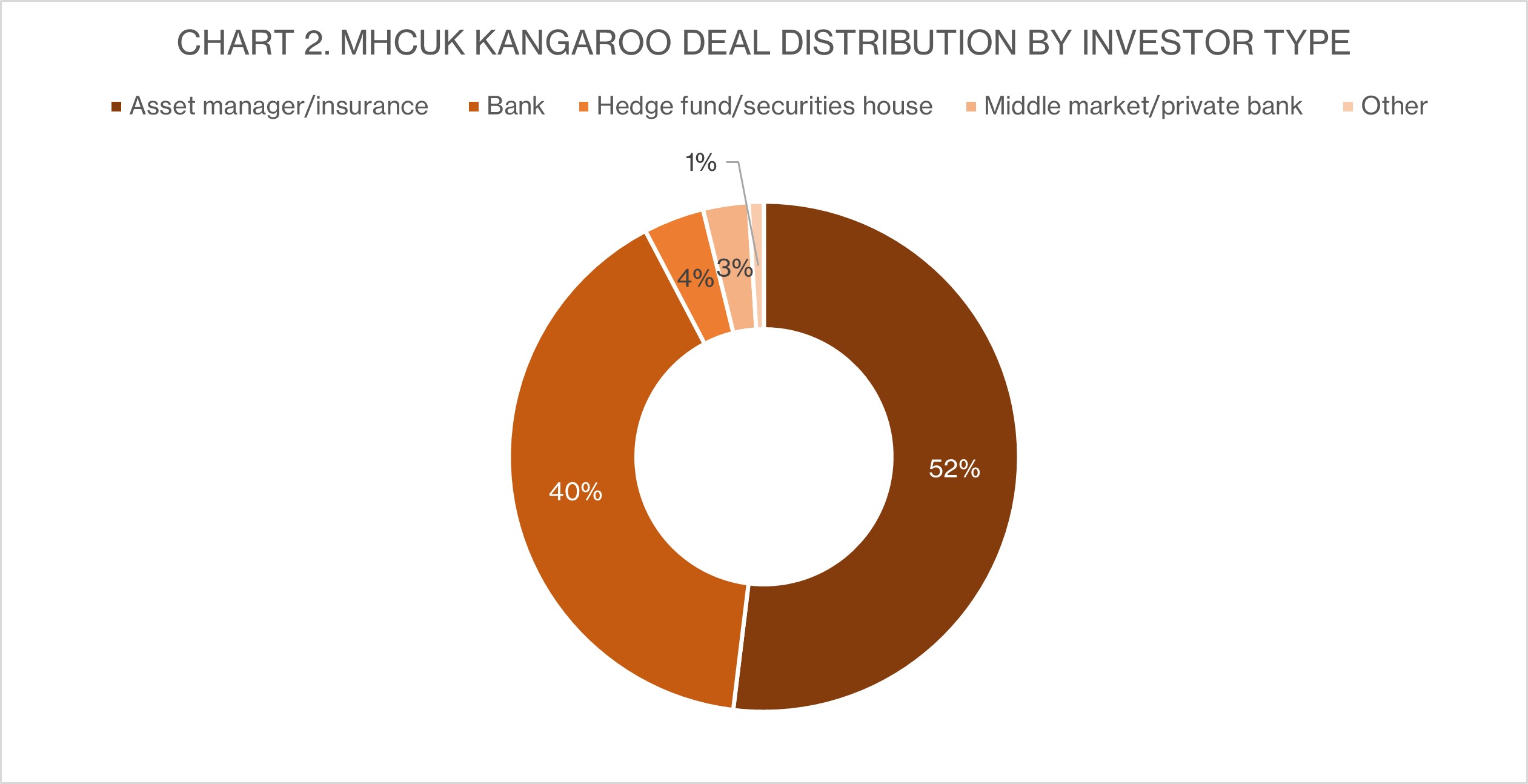

Distribution by investor type: see chart 2

Lead managers: ANZ, MUFG Securities, Nomura

Source: MUFG 6 December 2023

Source: MUFG 6 December 2023

Jocelyn Wong, Sydney-based executive director at ANZ, says the Australian dollar market can be challenging for inaugural issuers, especially offshore names, during busy periods and approaching the Christmas holiday. It is often a struggle to capture the focus of domestic accounts.

“The fact MHCUK attracted a broad investor base regionally is a testament to its marketing efforts,” Wong tells KangaNews. “It also demonstrates the resilience and depth of the Australian dollar market as it remained open to offshore issuers. Hopefully, more offshore issuers will consider our market next year to further supplement diversity.”

The issuer’s high rating also stood out in the Australian dollar credit landscape, Anna Germanos Sydney-based director, debt capital markets at MUFG, tells KangaNews. In particular, she adds, there is a notable lack of nonbank financial institutions in the single-A rating band.

Germanos says MHCUK received among the strongest IOI books she has seen in recent months, which provided the syndicate confidence to launch with revised guidance of 160 basis points over semi-quarterly swap, from 160-165 basis points. A rally in rates during the marketing process tightened outright yield without spread movement. Even so, Germanos says the book continued to grow and suffered little attrition even after a further price revision.

Jonathan Segal, managing director, EMEA Capital Markets at MUFG, adds: “MHCUK’s debut Australian dollar bond achieved the issuer’s key objective of diversifying its investor base into several large Australian asset managers while also leveraging support from a range of Asian investors to ensure a competitive financing cost.”

MHCUK’s London-based group treasurer, Jeremy Johnson, spoke to KangaNews about the issuer’s decision to come the Australian dollar market, the nature of its credit, the execution process and its funding plans.

What led MHCUK to come to the Australian dollar market now, and how will it fit into your overall funding profile? When and why you decided to engage with Kangaroo issuance?

MHCUK currently has an investor base of private placement MTNs – many of which are sold into Asia – and euro-denominated public bonds in Europe. We are keen to broaden out from this base. Australian dollar public bonds will form part of the mix of medium-term debt issuance in addition to the use of bilateral term bank borrowing, euro CP and securitisation in the UK.

Adding Australian dollar public debt issuance fits with the wider MHC Inc group’s global strategy, which is to raise more out outside its home market of Japan. This is because the business has already become, and will further become, more international.

The Australian dollar market is attractive to MHCUK because the minimum size for a public bond is around half that of a euro transaction, which enables us to deploy proceeds more efficiently and lowers concentration of rollovers in any single month.

We have been looking at the Australian dollar market for some time and, after seeing the strong market earlier in 2023, decided to take the first step by adding a Kangaroo wrapper to our MTN programme at the annual update in September.

Do you expect to return regularly?

Yes, after the success of our debut issue we anticipate returning to the Australian dollar market, potentially once or twice a year, to firmly establish our credit and access more domestic investor portfolios over time. This is provided, of course, that market rates and swaps co-operate.

How did you explain the nature of the credit and its business to Australian dollar investors?

The consumer and equipment finance businesses were readily understood by investors in Australia as similar companies are active in Australia.

What was important for Asian and Australian investors was the stability of the credit. In fact, this was critical. Notably, our strong capitalisation and low credit losses, alongside the strong ownership and credit ratings. We also set out MHCUK’s strategy and differentiating factors in our markets, which help us protect our business flows and margins.

You mention the appeal of Australian dollar benchmark deal size, but would you like to do bigger deals over time?

As noted, the deal size in Australian dollars is attractive to us as it is smaller than other public markets. MHCUK adds around £150-200 million ($US189.5-252.7 million) of assets per month, hence we can deploy this amount of proceeds easily within a month. We anticipate similar sized deals in the future, or slightly larger if our asset growth accelerates.

How did the landed cost of funds compare with what else is available to MHCUK?

MHCUK swapped the proceeds into sterling, given our predominantly sterling asset base. The cost of funds was broadly in line with other public bond markets such as euro, or possibly slightly lower. It was more expensive than MTN private placement issuance bank loans and, interestingly, securitisation – which is not usual.

Post-COVID-19, in-person roadshows are not a given. But an emerging theme this year is the deals where issuers have gone to the effort of conducting in-person roadshows have had better success. MHCUK chose to road show in-person, in Hong Kong, Singapore, Melbourne and Sydney. What bearing do you think this had on the deal’s outcome?

MHCUK was advised by its joint bookrunners that a physical roadshow was strongly recommended for a debut issue, to meet key investors in person and demonstrate commitment to the Australian dollar market.

We believe the roadshow achieved these objectives and led to a stronger focus on the transaction by investors – particularly domestic investors, in the context of a very busy Australian dollar new issue market in late November.

We viewed the physical roadshow as an investment to launch our Australian dollar fund raising and establish a base from which, next time, we hope to do more virtually. This would be more in line with our ESG [environmental, social and governance] credentials.

How helpful was post-roadshow feedback from Australian and regional investors, and what was the conversion rate?

We received good feedback from investors and the conversion rate was around 50 per cent of the investors we met in person, in Australia and Asia. We heard that some investors either did not have credit lines for MHC Group or preferred to wait to see how the first issue performs and then participate in secondary or subsequent issuance. This is helpful information in light of our strategy to build a presence in the Australian dollar market over time.

This deal went predominantly to an Asian investor base. Do you hope to build a domestic Australian following over time?

Indeed 60 per cent of the bonds were allocated to Asian investors and 40 per cent into Australia. This was due to strong support from a single, large Asian investor that knows us well. Without this investor it would have probably been predominantly domestic Australian investors. We do indeed look to build domestic participation over time.

How, if at all, did the strong rally in rates during MHCUK’s execution window affect thoughts on pricing and did you notice any shift in demand? Were you satisfied with the price outcome and what was the new-issue concession?

The rates rally worked in both ways. On one hand, it provided a positive backdrop for fixed income. On the other, it reduced the attractiveness for some yield-focused investors.

MHCUK was indifferent to the yield level, since we swapped the proceeds into sterling. We were satisfied with pricing, which is broadly in line with our public bond levels in other currencies albeit wide to our MTN issuance levels.

What factors did MHCUK consider before selecting three-year tenor and would it aim to extend its Australian dollar curve in future?

The three-year tenor is appropriate for MHCUK as it is close to the average life of our assets. For future issuance, we would likely issue in a similar tenor or slightly longer – after factoring in investor preferences and pricing dynamics.

MHCUK specialises in consumer, asset and auto finance. Is Australian asset-backed securities (ABS) issuance a viable option in the future?

This is not a near-term objective. MHC Group’s business in Australia uses private securitisation at the moment, but this is a joint venture. Securitisation is not always efficient from a cost and time perspective, and it needs scale to work efficiently. MHC Group’s Australian dollar asset base is probably not large enough yet for a public ABS deal, and MHCUK itself does not have Australian dollar-denominated assets. It would be more likely that we would add the Australian business to the MTN programme, to access capital markets that way.

Related news