Australia's buy side steps up

Australia’s government-sector issuers say their local real-money investor base was a key provider of funds in 2018. As market conditions shift once more, opinions about sector outlook vary within this newly re-energised buyer base.

Helen Craig Senior Content Manager and Deputy Editor KANGANEWS

Among the most significant factors for investors assessing the Australian government sector at the start of 2019 are heightened global rates volatility and the fact that Australian Office of Financial Management (AOFM)’s net new issuance is expected to be substantially lower going forward than it has been in recent years. Investors expect both to have an impact on government and semi-government demand and spreads.

Buy-side participants tend to agree that inflation will likely continue to be the missing risk factor in 2019 (see box). But elsewhere opinions are varied, suggesting the year ahead could be among the more unpredictable periods for the high-grade market in recent years.

The second half of 2018 reintroduced to global markets a level of uncertainty not seen for several years. Investors do not expect the previous benign conditions to return imminently. For instance, Anne Anderson, Sydney-based head of fixed income and investment solutions, Australia at UBS Asset Management, describes the current period as “a time for patience and waiting for the data to roll through”.

The underlying global macro environment is riddled with uncertainty. To some extent, market participants are actually impressed at how orderly bond-market behaviour has been in this context. “Interestingly, through all of this the market has not broken new ground,” Anderson says. “We still think we are in a trading range – just one that has shifted lower, by approximately 25 basis points, across the board.”

The impact of the more volatile global backdrop on the Australian high-grade sector is yet to be felt in the local secondary market to any game-changing degree. Fund managers highlight narrow bid-offer spreads and the predictably slow early-year transaction volume, though some have started to notice anomalies creeping in to relative pricing – between semis, between semis across the yield curve, and between semis and Australian Commonwealth government bonds (ACGBs).

Market infrastructure is now less able to act as a volatility buffer. “We notice from time to time that parcels of semis moving through the market will be significantly marked in or out. Without the same range of entities to facilitate flows the banks are eager to move parcels quickly and as such mark the spread wider to attract a buyer,” comments Ardea Investment Management’s Sydney-based principal, Tamar Hamlyn.

Investor rotation

The global rates environment is also having an impact on demand patterns for Australian dollar high-grade assets. Local government-sector issuers acknowledge the offshore investor segment has been a harder sell as Australian rates have gone increasingly negative to the US. Meanwhile, the big incremental bid of recent years – domestic banks building their holdings of high-quality liquid assets (HQLAs) – has completed its accumulation phase.

Australian fund managers are paying close attention to the realities of demand elsewhere, especially as their own bid has grown in significance for the sector as a whole. Darren Langer, senior portfolio manager at Nikko Asset Management in Sydney, argues that stagnant balance-sheet demand will have an impact particularly for semi-government issuers.

Langer says the Australian issuers’ curves are reliably 30-50 basis points tighter than the Canadian or German provinces that are their nearest global comps. While the Australian states are generally better rated, Langer argues that a major component of the pricing differential is regulatory demand built into the Australian system. This domestic pricing edge also explains why foreign-currency deal economics rarely work for Australian states.

Australia’s major banks have concluded the process of accumulating HQLAs, and in fact the scale of their liquid-asset books might be set to reverse to at least some extent if credit growth stalls for the big four.

At the same time, while the Australian savings system’s famously low allocation to fixed income remains stubbornly unmovable, the sheer scale of system growth has driven assets into debt portfolios – to the benefit of high-grade issuers. “We are seeing some net inflows into fixed income, particularly as fears around tightening monetary policy recede while low inflation and increased volatility persist,” Anderson adds.

Overall, fund managers say they are comfortable with a demand picture for Australian government-sector debt which they say should if anything be supportive of yield in 2019. The supply picture marginally changes this dynamic, though – especially in the state-government sector.

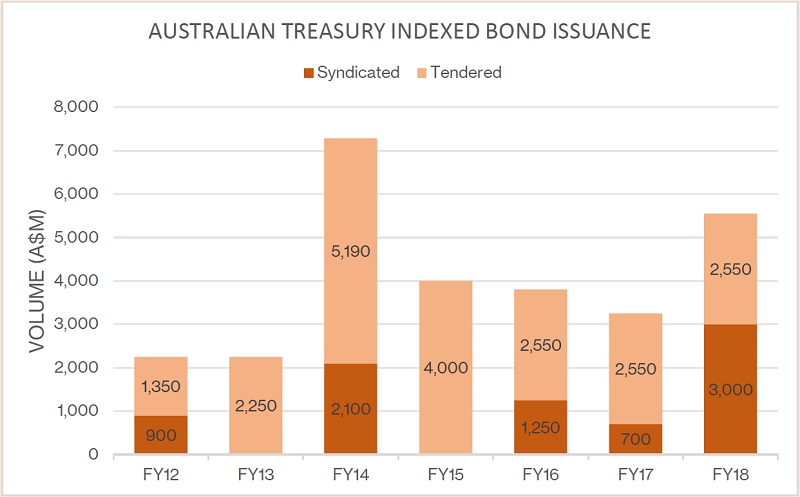

Inflation: the missing linker

Australian investors do not expect an inflation breakout. However, they say inflation-linked bonds still have a role and expect the Australian Office of Financial Management (AOFM) will continue to meet demand.

The outlook for inflation in Australia is largely driven by oil prices, energy and – in the near term – the direction of the currency. While the Australian dollar has been falling, its inflationary impact is hard to maintain.

“The impact of the currency on inflation is only temporary – to repeat it the Australian dollar would need to fall consistently quarter after quarter,” says Tamar Hamlyn, principal at Ardea Investment Management. “The medium-term impact is driven by demand and economic activity. In Australia, consumption is subdued, we have high debt levels and we don’t have the type of organically strong domestic demand that could give us an inflation problem over the next 3-5 years.”

Source: Australian Office of Financial Management 5 February 2019

The currency markets will continue to move the inflation poles around until there is sufficient global demand to bring about a global upswing in inflation.

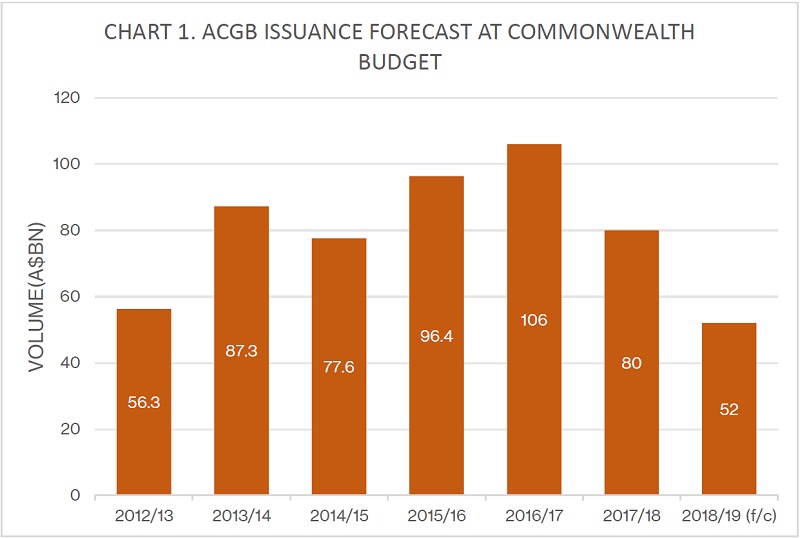

Material reduction

Following the release of the Australian government’s mid-year economic and fiscal outlook in December 2018, the AOFM revealed a reduced 2018/19 financial-year borrowing requirement of around A$52 billion, down from A$70 billion at the 2018/19 budget and its smallest funding year for a decade (see chart 1).

The impact on pricing is yet to be determined. Some buy-side sources believe lower supply of ACGBs could support yield. Others claim the impact of lower supply will be less directly felt.

“The lower AOFM supply outlook is positive,” Anderson tells KangaNews. “The stock of debt has stopped growing and the flow is being cut back, which has to be positive in an environment of risk-asset volatility.”

Langer says less AOFM supply may only offset the general reduction in demand from the banking sector. “If you look back over the last 10 years, any time the AOFM has needed to increase its borrowing programme it hasn’t had a problem – so if anything being able to reduce it in the current environment will help.”

Source: Australian Office of Financial Management 2 February 2019

It may be important for the Commonwealth government to hit Treasury forecasts, though. Langer says the risk factor would be if the budget deteriorates and the AOFM has to increase its programme in the future without concurrent growth in HQLA books or globally appealing Australian headline yield.

The bigger issue the AOFM might have to face, Langer continues, is the relative value of Australia compared with other global options. “The US is obviously much higher in yield. It is still not as attractive for some offshore investors to buy US Treasuries as it is ACGBs but this could change if the relative-value dynamic continues,” he says.

Investors are certainly focused on the respective paths of Australian and US rates. But, in common with much of the tone at the start of 2019, there is little clarity about expectations. The key areas of interest are whether the US Federal Reserve is now officially on hold or has simply eased off the gas in its hiking journey and whether the Reserve Bank of Australia (RBA)’s next move is a hike, a cut or on hold indefinitely. There seems to be some confidence in the US economy among Australian investors. Otherwise, the buy side is largely waiting for data guidance.

“The marked policy divergence between the third quarters of 2017 and 2018, when the Australian-US spread inverted quite strongly, and the November to December 2018 period where market participants started to wonder whether the US policy stance was sustainable, has been an interesting dynamic to observe,” says Justin Tyler, director at Daintree Capital in Sydney.

He continues: “It’s interesting that we haven’t seen the Australian-US spread widen out at the start of this year – which proves that the spread inverting the way it did was due to the US policy stance. Without the global growth slowdown that caused the US move in the first place, in particular the China element, one might have expected to see the spread go back the other way.”

Hamlyn suggests the RBA would have been hoping that gradually rising US interest rates would provide some cover for it to remain on hold. But he also suggests that by doing nothing while the US has edged higher the RBA has created a degree of de facto stimulus.

The February 2019 RBA cash-rate decision took a notably more dovish tone. But Hamlyn sees a high hurdle to an RBA cut given the fragility of the housing market. “It is also not clear that cuts would be effective in stimulating the right type of demand or that they would be effective in addressing what are likely supply constraints to credit emanating from the royal commission.”

Investors expect a more orderly US-Australian spread in 2019, albeit one in which the differential continues to invert. As Hamlyn explains, it is not just divergent national economic fortunes that are driving the spread gap.

“The difference is that during previous periods of divergence between Australia and the US the Australian dollar was relatively weaker, our external deficit was larger and we were running current-account deficits that were bigger than they are now. We have seen a huge investment in commodities in the last decade – in production and exporting capability – so Australia doesn’t have the structural deficit it used to.”

This means Australia’s need to pay a high yield to fund its deficit does not apply to the same extent it has in the past. “The fact that we can run lower yields because we don’t have to fund this deficit means we might expect a bit more outperformance relative to US Treasuries,” Hamlyn concludes.

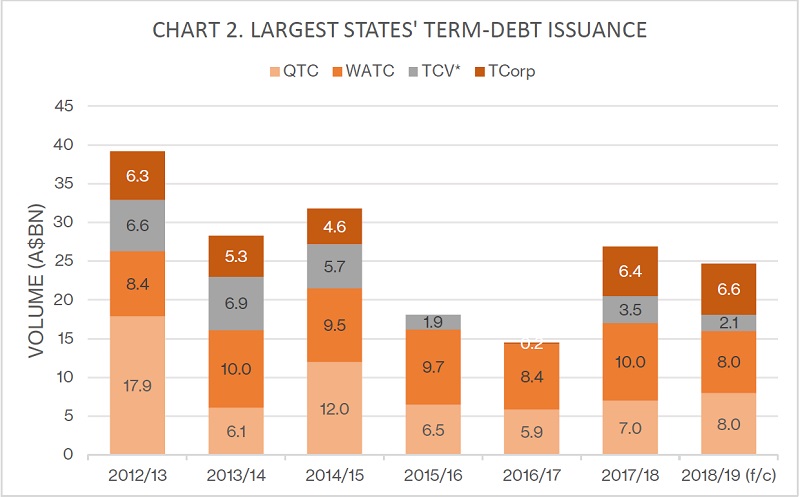

Semis to the fore

While any number of market directions are possible, the issuance story for ACGBs – especially the fact that the gross funding task will be mainly refinancing existing debt rather than net new issuance – suggests healthy supply-demand fundamentals. This is good news for state-government issuers, which in aggregate are preparing for an increased new-issuance task in the medium term.

The four biggest semi-government issuers – New South Wales Treasury Corporation (TCorp), Queensland Treasury Corporation (QTC), Treasury Corporation of Victoria (TCV) and Western Australian Treasury Corporation (WATC) – have forecast an aggregate term-funding need of close to A$25 billion for the current funding year, 2018/19. This is slightly less than actual volume raised in 2017/18 but significantly more than the two years prior (see chart 2).

But it is the states’ need to fund their future infrastructure requirements that investors believe will fill the gap left by falling ACGB issuance. For instance, the Victorian government has pledged to borrow more than A$20 billion to fund projects including a rail line to Melbourne Airport. There is similar rhetoric around the need for infrastructure funding in New South Wales (NSW), although a March 2019 state election could change the outlook.

Source: KangaNews, New South Wales Treasury Corporation, Queensland Treasury Corporation, Treasury Corporation of Victoria, Western Australian Treasury Corporation, 2 February 2019

Langer is not as convinced that the federal government’s return to surplus is as set in stone as the government predicts, and potential increased ACGB supply could have an impact on semis’ access to markets later in 2019.

“Growth is probably going to come in below estimates so we think the return to surplus this year is unlikely,” he tells KangaNews. “It is likely that there could be some argy-bargy between the need for the federal government to borrow more – which is probably an end-of-year story – and the states funding their infrastructure.”

This could cause a widening in semis’ spreads in 2020, Langer continues. “We have already started to see this with the longer-dated semis starting to push out a few basis points here and there. I can’t see what else, apart from the anticipation of more supply, would be driving this.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

Related news