New Zealand debt market eyes a shake-up

Proposed new capital requirements for New Zealand’s banking sector are causing consternation in the local debt market as participants grapple with a raft of potential implications. The consequences for the fixed-income sector – intended and unintended – are potentially game-changing and are relevant to sectors as diverse as the high-grade Kauri market and corporate debt.

Matt Zaunmayr Staff Writer KANGANEWS

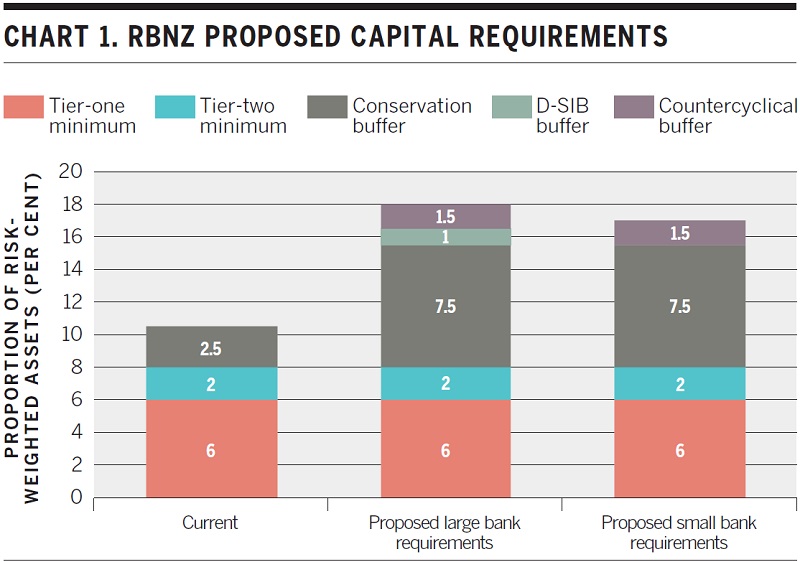

On 14 December 2018, the Reserve Bank of New Zealand (RBNZ) released a consultation paper reviewing the capital-adequacy framework for registered banks. This recommends increasing the required tier-one capital ratio for local domestic systemically important banks (D-SIBs) to 16 per cent from 8.5 per cent and for other registered banks to 15 per cent (see chart 1).

The proposals also recommend changes to the calculation of risk-weighted assets. Banks that are internal-ratings based (IRB) accredited – the New Zealand majors – will also be required to use the standardised approach methodology for credit exposures that have an external rating. This includes exposures to other banks, sovereigns and large corporates.

The RBNZ proposals set out a floor of 85 per cent applied to outputs from IRB models. The reserve bank estimates that this will result in a 15.5 per cent lift in risk-weighted assets (RWAs) for IRB banks. The already increased capital-ratio requirements would be against this likely higher calculation of RWAs.

The RBNZ says the changes are first and foremost designed to ensure stability in the local banking system, while levelling the RWA playing field between the major banks and the rest of the sector is another consideration.

Source: Reserve Bank of New Zealand 14 December 2018

According to the RBNZ’s consultation paper, the 16 per cent capital ratio is the point identified where “there is enough capital in the system as a whole to cover losses that are so large they might only occur very infrequently”.

This is clearly the outer frontier for capital requirements. The RBNZ also states that “at a tier-one capital ratio of 16 per cent there would be little room to increase stability further without some impact on expected output”.

There can be no doubt that, if implemented, the RBNZ proposals would put New Zealand’s banks at the top of any global capital comparison. A report prepared by PwC for the New Zealand Bankers’ Association in October 2017 estimated “large, internationally active banks” to be running average total-capital ratios of 14.7 per cent. New Zealand’s big four were at levels in the range 12.5-13.5 per cent, but stricter local rules led PwC to estimate that around 6 per cent could be added to the New Zealand totals on an internationally comparable basis.

Extrapolating to the latest RBNZ proposals, while the New Zealand banks might have to add just a few percentage points of capital, this could place them at more than 20 per cent total capital when internationally harmonised – especially given the further ramping up of RWA standards.

There are a myriad of implications that such a capital raising might have for New Zealand’s banks as well as the wider debt capital markets and economy.

BNZ’s Wellington-based head of research, Stephen Toplis, tells KangaNews: “Capital requirements have been consistently raised since the financial crisis so we have an understanding of what the possible implications are. But we do not really have a working understanding of what the consequences might be from the degree of shift beng proposed.”

Furthermore, the RBNZ is insisting that new capital come in the form of common-equity tier-one (CET1) rather than any form of additional capital – which the reserve bank believes does not contribute to the safety of a bank.

How exactly New Zealand’s major banks would raise the equity required under the proposed changes is one of the key aspects of the debate, given the banks themselves are owned by Australia’s big four and therefore do not have the capacity to issue their own shares.

Ross Pennington, Auckland-based partner at Chapman Tripp, says there are a few ways the banks could meet the requirement. “They could shrink lending, change the composition of lending or raise equity. It will likely end up being a combination of methods.”

In loco parentis: Australian majors and Kiwi capital

Increased capital requirements on the New Zealand majors could affect their Australian parents. Whether the Australian banks will subsidise incremental capital accumulation in New Zealand is unknown, however – as is any changed impact of more capitalised subsidiaries at group level.

Specifically, it is unclear how the Australian Prudential Regulation Authority (APRA) would view increased capital in the New Zealand banking system. Under current Australian regulation, more heavily capitalised New Zealand subsidiaries would not contribute to an improved group capital position.

A Westpac Institutional Bank (Westpac) research note states that “at this point, capital held at subsidiaries does not [affect] level-two bank reporting with the banks’ exposure to their subsidiaries recognised through a 400 per cent risk weighting. Therefore, the increased New Zealand capital has no benefit for the parent”.

The RBNZ suggests that the banks could raise the capital over a period of five years through retained earnings. This may be possible – if painful to shareholders. Jack Do, director, financial institutions at Fitch Ratings in Sydney, estimates that meeting the increased capital requirement would account for 70 per cent of banks’ profit over the five-year period.

But he adds: “The major banks in New Zealand have large market share, pricing power and earning capacity so we think they can make the requirements with retained earnings. It is likely, though, that the dividend they return to Australia will be significantly reduced during this period.”

The scale of the majors’ balance sheets and those of their Australian parents at least give them capital-raising options – although the extent to which they can rely on their parents is an open question (see box). Martien Lubberink, associate professor, accounting and capital at Victoria University of Wellington, says the smaller banks may face a greater struggle in raising further common equity.

“If the proposals are brought in, there will likely be a race to the top and the banks that can will begin raising the capital immediately. Some of the smaller banks, which will have fewer options to meet the requirements, may struggle to keep up,” Lubberink tells KangaNews.

Market participants say there is clearly less capacity to generate capital from profits in the smaller-bank sector. Do says it is likely some smaller and cooperative banks will need to go to their shareholders or rely on new capital instruments – to the extent these are allowed – to meet at least some of the requirement.

Credit consequences

Such a significant increase in bank capital requirements will inevitably have an impact on banks’ all-in cost of funds, as so much more of the total funding stack will have to come from the equity market rather than cheaper debt funds.

The RBNZ is confident this will only be a marginal factor. It estimates that a 1 per cent increase in a banking system’s tier-one capital ratio from current levels “may lead to a 6 basis point increase in the price of bank credit”.

The RBNZ estimates its proposal will lead to the major banks needing to raise NZ$12.8 billion (US$8.8 billion) of additional tier-one capital to meet the proposed regulatory minimum. However, market estimates are higher in many cases given banks tend to hold a voluntary buffer over the regulatory minimum.

Assuming a 2 per cent buffer over the regulatory minimum, a BNZ research note estimates the big four will need to raise an extra NZ$18.6 billion of equity with a consequent 40 basis point increment to the aggregate cost of funds. ANZ research estimates the figure to be NZ$22 billion, taking into account a 3 per cent buffer, and a 50 basis point cost-of-funds increment.

This will inevitably lead to more expensive or less readily available credit in New Zealand. Either or both are possible, with the weight of market opinion perhaps leaning towards more expensive credit rather than less of it.

As one senior New Zealand bank funder says: “New Zealand is just one place where investors can put their money to work. The reality is if the return opportunity is greater elsewhere, they will take that opportunity. The only way to attract the extra capital will be to ensure shareholders receive an appropriate return, which means higher lending margins.”

Do agrees that it is likely the New Zealand major banks will be able to pass on the cost of the capital requirements through higher lending rates. “The New Zealand major banks are rated where they are because of the strength of the franchises and their overwhelming control of market share. If they can pass on price increases, we don’t see any scenario where they wouldn’t opt to do so,” he tells KangaNews.

However, David Tripe, professor and head of the school of economics and finance at Palmerston North’s Massey University, believes it is more likely that there will be a reduction in lending rather than a material increase in the price of credit.

“Reducing lending is one way of decreasing the amount of equity that needs to be raised. Furthermore, with a downward shift in the return on bank equity, the market value of banks will be undermined. This could also lead to banks cutting back on their lending exposure,” Tripe tells KangaNews.

ANZ’s research draws a similar conclusion, stating that the move to build a higher capital buffer affirms the bank analysts’ call that the next move for the official cash rate (OCR) will be a cut rather than a hike.

The note states: “Conceptually, a higher cost of funds, whether temporary or permanent, would need to be offset by a lower OCR…Another reason the OCR may need to be lower during the transition period is that banks can meet the new ratios not only by raising capital but also by reducing their balance sheet.”

Dominick Stephens, Auckland-based chief economist at Westpac Banking Corporation New Zealand Branch, doubts monetary policy would be able to offset the macroeconomic impact of the increased capital requirements totally. He still believes the next move in OCR will be a hike – eventually – as any move put in place purely to counter capital changes would only be a temporary stopgap.

The key risk of banks reducing their lending is specifically that they lower the intensity of their exposure to higher-risk assets that contribute more to economic growth, such as SMEs, Lubberink argues. He says the context of recent economic data pointing to either stabilising or negative economic growth means this type of credit withdrawal would present a significant risk to the broader economy.

When the European Banking Authority (EBA) began implementing new bank capital requirements, it also issued two warnings – in 2012 and 2013 – instructing banks not to meet the requirements through de-risking.

The EBA asked national supervisory authorities to ensure banks maintained a nominal amount of capital corresponding to their capital requirements. This was designed to preserve the flow of lending into the real economy and thus maintain credit and economic growth.

Lubberink believes a similar message from the RBNZ could be warranted to ensure credit supply in New Zealand is maintained. This is not something the RBNZ is currently consulting on, according to its Wellington-based deputy governor and general manager, financial stability, Geoff Bascand. He adds, though, that the reserve bank may look at how the new capital is raised if capital availability did become a concern or if the consultation suggests it is likely to do so.

But he does not expect this to be necessary given the competitive nature of the banking sector. “The banks are very profitable, with rates of return on equity of 13-14 per cent. It would take a lot to drive this down to levels where they would rather pull out or shrink their business.”

Theory Issues

The Reserve Bank of New Zealand (RBNZ) used several parameters to establish its proposals for new bank-capital requirements. Market participants have expressed particular concern over the applicability of the Modigliani-Miller (MM) theory.

Proponents of heightened capital requirements place heavy reliance on the MM theory, which posits that a firm’s capital structure is irrelevant to its value. Instead, value is discerned completely from earnings potential and underlying asset risk.

This is important in assessing the cost of increased capital requirements because, if it is true, there should be no funding-cost increase passed through to borrowers in the real economy. Even though equity capital is more expensive than debt, a bank’s overall cost of capital will be equalised through the reduction in its risk.

The extent of any MM offset is therefore critical in assessing the likely cost of an increase in the required level of common equity.

Market participants admit that it is too early to attempt to make final-position predictions about credit supply and cost in a new capital environment. Toplis insists there is little doubt that banks will supply less credit than they otherwise would, but the magnitude is difficult to predict.

“When a vacuum is created in financial markets, typically other actors will come in and fill it. While supply of credit from banks will likely be slower, the negative implications of this for the wider economy aren’t necessarily a given as it is likely other players – such as international banks or nonbanks – will play a larger role in the lending market,” Toplis tells KangaNews.

Pennington is sure the new regime will give wholesale-funded nonbank lenders a competitive boost – unless the equivalent impact on banks’ provision of credit to this sector is even greater. While there are plans to bring nonbank lenders into the capital-adequacy framework, Pennington has doubts this can be achieved.

Tripe is more circumspect on the likelihood of nonbank lenders having sufficient capacity to make up a potential credit shortfall. Given New Zealand’s largest nonbank lender, UDC Finance, is owned by ANZ and the second-largest, Latitude Financial Services, currently has less than 1 per cent lending market share, he says it is difficult to envision these institutions making a meaningful difference across the credit landscape.

Certain uncertainty

More fundamentally, there are also questions about whether the 16 per cent capital figure the RBNZ has landed on is really necessary for the “soundness and efficiency” of the New Zealand financial system.

“Stability and efficiency are companion pieces and the way the RBNZ has dealt with them is artificial,” says Pennington. “It has sought an amount of ‘soundness’ required to survive a one-in-200-year banking crisis, and only then does it look at how much more equity can be brought into the system without affecting efficiency. The efficiency element is completely ignored in the first part of the equation.”

Tripe says while the increased capital ratio has a good chance of making the financial system somewhat safer, one of the consequences of a decrease in lending – particularly to businesses – could be economic distress which could then lead to problem loans.

The bulk of New Zealand bank books comprises residential mortgages. The major risk factor in this context is that a policy aimed at bolstering financial-market stability could end up doing the opposite by creating a credit squeeze and thus property-market weakness.

A UBS research note argues that the RBNZ is underestimating the potential mortgage repricing that could result from the new requirements, which would come at a “significant cost to the New Zealand economy”.

The RBNZ’s own calculations suggest a 3 basis point decline in the steady-state level of GDP for every 1 percentage point increase in banks’ required tier-one capital ratio. But the central bank says this should be balanced by the benefits of the additional safety this capital would provide.

Observers are not convinced by the theory or parameters used by the RBNZ in its consultation paper (see box). The reference to a one-in-200-year crisis in particular has caused consternation.

Pennington points out that in the last 40 years – which he says constitutes the time in which the banking system has been comparable to what exists now – New Zealand is one of only three countries that has not had a bank crisis, along with Australia and Canada.

Another senior bank funder tells KangaNews that the level of incremental capital the RBNZ is requiring to safeguard against such a crisis is perhaps past the point of diminishing marginal returns. In other words, the amount of safety the incremental capital brings is not worth the cost – to the banks or the broader economy.

Furthermore, Tripe says: “No-one can know what the impact of such an event would be because there is no data available. Even if there was, what happens at one point in a probability distribution does not give any basis for knowing what happens at another point in the probability distribution.”

“Stability and efficiency are companion pieces and the way the RBNZ has dealt with them is artificial. It has sought an amount of ‘soundness’ required to survive a one-in-200-year banking crisis, and only then does it look at how much more equity can be brought into the system without affecting efficiency.”

Debt market in flux

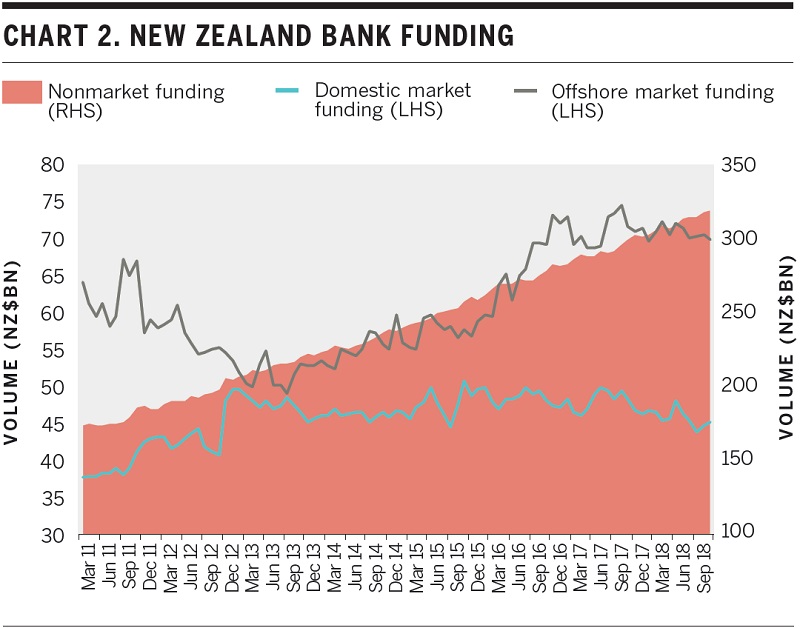

For debt-market participants, the consequences of the RBNZ’s capital proposal could run much deeper even than a reshaped and repriced lending market. The additional equity funds the banks need can be expected to result in an equivalent reduction in wholesale debt issuance. The major banks are significant sources of issuance in an already undersupplied domestic bond market.

However, Nick Smyth, Wellington-based interest rate strategist at BNZ, says this outcome is not certain. In fact, it depends on how the relationship between credit and deposit growth plays out. Smyth adds that any slowdown in wholesale debt issuance by the banks is most likely to come in offshore funding given this is where funding growth has been focused in recent years and is also where funding is most expensive (see chart 2).

One bank funder KangaNews spoke to is explicit on the assumption that the proposed changes would result in a decreased appetite for offshore funding.

The domestic capital market would not be immune to such a shift, though. Less offshore funding could result in a less liquid and repriced New Zealand dollar basis swap, which could in turn put a drag on Kauri-market economics.

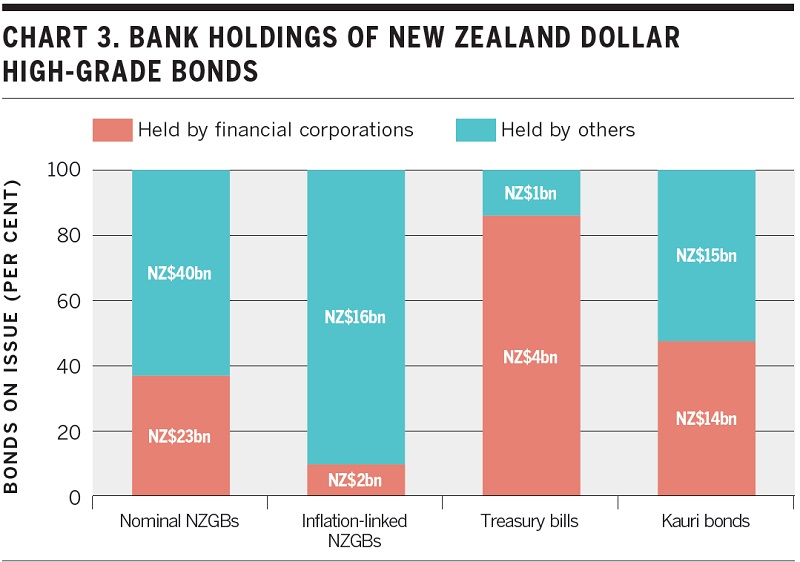

Demand for Kauri and other high-grade product would already be under question. With more CET1 capital, less wholesale funding and – perhaps – less lending, banks’ high-quality liquid asset needs might be expected to fall. RBNZ data confirm that financial corporations are substantial holders of New Zealand government bonds (NZGBs) and Kauris (see chart 3).

BNZ research states: “In time, this might be expected to put some marginal upward pressure on NZGB yields relative to swaps, although we expect this should be second order compared to the NZGB supply outlook and broader trends in investor demand.”

Less frequent senior wholesale bank funding might be expected to benefit spreads – and this is a key plank of the RBNZ’s thinking on the overall cost impact of its proposed capital changes.

Source: Reserve Bank of New Zealand 25 January 2019

Source: Reserve Bank of New Zealand 25 January 2019

But Stephens says: “The benefit for bank senior bondholders might be positive but it is likely to be vanishingly small. Interest rates on New Zealand bank paper reflect the fact that they are subsidiaries of the Australian major banks, with only a small premium paid. If the New Zealand subsidiary becomes safer this premium may fall, but it will likely be very marginal.”

There is a potential positive consequence for the New Zealand domestic credit market. If higher capital requirements force up the cost of corporate lending, as many in the market believe they will, Stephens says it is possible that some additional corporate borrowers may look to finance through direct debt issuance.

Smyth agrees that there is some potential for capital-market growth from increased bank regulation. He cites the disintermediation that has occurred in Europe over the last 10 years in which he says bank regulation has played a part.

“It would likely take some time to play out, but if the cost of accessing credit becomes higher one implication could be that some larger names, which would typically borrow from banks, may look to borrow in their own name if the cost is advantageous,” Smyth tells KangaNews.

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

Related news