Woolworths delivers next evolution of Australian green-bond issuance

The scale of demand for Woolworths’ debut green bond – which supported a significant price revision – further demonstrates the potential of the asset class for local corporate borrowers, issuer and leads say. Demand for certified sustainable bonds could even be sufficient to put mid-curve domestic issuance on a pricing par with bank loans and thus entice more issuers to market.

Woolworths printed A$400 million (US$285.8 million) of five-year green bonds on 12 April. ANZ was green-bond adviser and led alongside Citi and J.P. Morgan. Final pricing was 120 basis points over swap or 10-15 basis points tighter than guidance, a tightening that was supported by a book that reached A$2.1 billion.

Taken at face value, the transaction delivers a number of landmarks – including being the first retail-sector green bond in Australia and the largest from a nonfinancial corporate, and the first Climate Bonds Initiative (CBI)-certified deal globally to be based on supermarket assets.

Deal sources – including investors – are if anything more excited about what they believe to be the wider connotations of Woolworths’ green debut. While noting that corporate issuers need to be fully bought in to sustainable issuance well beyond the treasury department, there is clearly a sense that this type of issuance hints at potential that the Australian dollar corporate market as a whole has historically struggled to unlock.

Book blowout

The main purpose of the Woolworths deal was to refinance a A$500 million maturity from March this year, and its size was capped at A$400 million as a result. The company had not issued domestically in any format since 2012. Demand massively outstripped maximum volume and held up even after the significant price revision.

According to Aby Owen, director, Australian dollar syndicate at Citi in Sydney, the book grew to A$2.1 billion at its peak and closed at more than A$2 billion even at the final price. Around 90 accounts participated in total, which Owen compares to the typical book of a jumbo, multitranche corporate deal.

Green bond issuers often say their main goal in using the asset class is to gain access to new investors – and Woolworths is no exception. David Marr, the company’s Sydney-based CFO, says the main benefit of a green bond for the issuer was the added diversification it provided. “I don’t think the pricing outcome came about just because it was a green deal,” he adds. “It was the product of the level of interest in general – though there is no doubt that the ESG component was an element of that interest.”

The scale of demand for its debut allowed Woolworths to take a more proactive approach to finding new investors. Leads report that identifying potential buyers’ credentials in the environmental, social and governance (ESG) space was part of the deal process going back to the predeal roadshow.

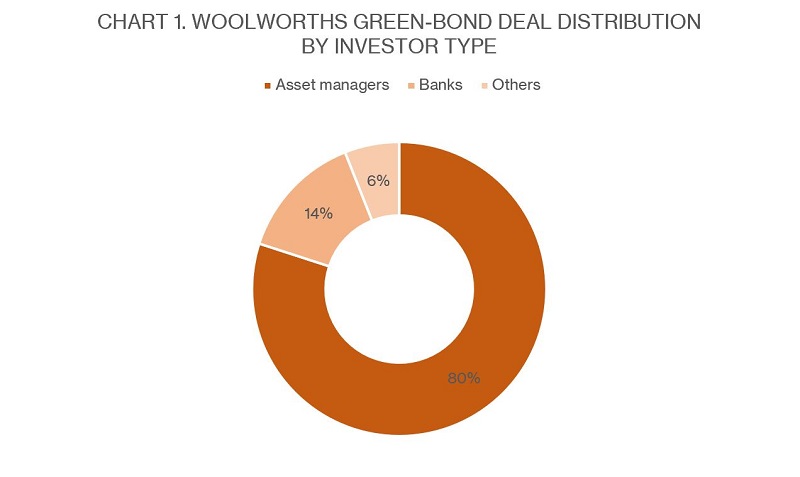

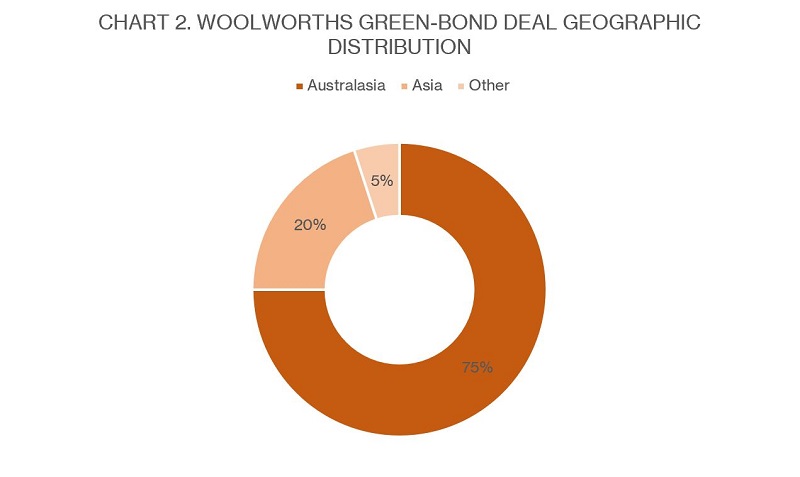

Lead manager data reveal that 98 per cent of deal was placed with green investors. Meanwhile, three-quarters was sold to Australasian accounts and asset managers took the lion’s share (see charts 1 and 2).

Source: ANZ 15 April 2019

Source: ANZ 15 April 2019

This type of targeted placement was a clear positive for the issuer. Andrew Brown, Sydney-based director, debt capital markets at ANZ, says: “Woolworths was very focused throughout the process on helping to develop the green-bond market. It was keen to understand investors’ green credentials, so we asked for information from accounts on this and where bonds would be placed as part of the bookbuild process.”

Tagging investors on an ESG basis is not necessarily quantifiable at the current stage of market development, however. Rishik Arya, debt syndicate at J.P. Morgan in Sydney, explains: “It’s hard to be too scientific – we can sometimes say definitively that an investor wants to allocate a specific volume into a certain green fund, but really it is more about understanding their overall ESG approach.”

Deal sources universally say that funds targeting sustainable assets are growing in Australia. Duncan Beattie, J.P. Morgan’s Sydney-based co-head of DCM, says every one of environmental, social and governance considerations will continue to grow in importance.

Investor response

Buy-side sources confirm that they were asked to provide details of their own ESG engagement as part of the Woolworths deal process. Jeff Grow, executive director at UBS Asset Management (UBS AM) in Sydney, reveals: “We were asked to provide some green credentials, and did so willingly – for instance industry awards such as KangaNews's Australian Sustainability Fund Manager of the Year, our proven track record of investing in green and sustainable bonds and others.”

Marayka Ward, Brisbane-based senior credit manager and ESG champion at QIC, reveals that issuers wanting to understand investors’ green credentials is not uncommon in recent years.

While a third fund manager tells KangaNews their interest in the deal was limited by its perceived tight pricing, others were comfortable even at the revised level. Those that stuck with the transaction received an immediate reward, as Arya says it was marked 5-7 points tighter in early secondary trading.

Ward says: “From a pure relative-value perspective the initial price talk was fair… Add into the equation growing interest from investors looking for sustainable investments and the book size was always going to be large. Of course, it would have been great to see the deal print at the initial price talk but as an investor we also want to see a well-structured, well-supported deal that is going to perform after it is priced.”

Grow says investors would likely have had natural appetite for Woolworths as a household name in Australia with no domestic bonds outstanding. Its indicative price was wide of local comps like the 2024 tranches of the recent McDonald’s Corporation Kangaroo, and even the tighter revision largely brought it into the mid-range of such peer issuance.

“With the deal being capped at A$400 million by the issuer and more than A$2 billion of reported demand, it was inevitable that some firm pricing was necessary to clear the market,” Grow concludes.

Conducive market

It is, however, relatively hard to attribute the evident success of the Woolworths deal accurately between green factors and market conditions more generally. “It’s a high-quality, defensive name that hasn’t issued domestically since 2012 so it was always likely to be well supported,” Beattie comments. “But equally there’s no doubt the green aspect attracted additional demand that would not have bought a vanilla Woolworths bond.”

On the execution front, a market that has been relatively starved of corporate issuance was well set up to be receptive to a Woolworths deal – whether or not it came to market with green certification.

“It’s a very technical-driven market at present with low corporate issuance the main driver,” explains Paul White, ANZ’s Sydney-based global head of capital markets. “A vanilla Woolworths transaction would have been well received despite the company having a lower rating than the last time it issued domestically.”

Owen is reluctant to estimate the exact extent to which demand was driven by the green component of the deal specifically. But she does say: “Green was a differentiating factor for many investors and there were orders in the book which would not have participated in a vanilla bond. Cumulatively, these helped enable us to push the price revision to the extent we did.”

Pricing connotations

It may have taken all the supportive factors in combination to lay the foundations for Woolworths’ pricing outcome. Whatever the cause, the difference between indicative and final margin could be significant for the Australian dollar corporate bond market.

Specifically, tighter pricing – supported, leads believe, by green certification – pushed the Woolworths deal into a range that could make domestic issuance a more compelling option for corporate names, says Ian Campbell, Citi’s Sydney-based managing director and head of debt capital markets, Australia and New Zealand.

“Bank debt has been very competitive, especially liquidity from Asia, and there has been a clear gap in pricing between the bank and bond markets in the 5-7 year part of the curve,” Campbell tells KangaNews. “Woolworths’ pricing closed that gap, and if issuing in green-bond format is able to deliver this sort of outcome I don’t think it is too much to say that it might make issuers look more positively on the domestic bond market.”

This will not be a binary decision, however. While Gavin Chappell, head of syndications, Australia at ANZ in Sydney, agrees that Woolworths’ pricing was in line with what the borrower might expect to achieve in a similar-tenor bank loan, he says a simple price-based comparison of funding options misses the more detailed debt strategies corporates are increasingly deploying. This includes adapting their bank books to take liquidity from a wider range of lenders.

“Borrowers are getting more sophisticated about who their investors are – it’s not just about the product they are offering,” Chappell explains. “Of course they want tenor at attractive pricing but they also want to diversify their investor bases, including in their loan books.”

Chappell is also cautious about extrapolating Woolworths’ success generically to corporate Australia. He says the options and pricing available to borrowers across different sectors varies. For instance, the price and tenor that has for a long time been available to many infrastructure borrowers in the US private placement market is a challenge the loan market has “only very recently been able to get close to matching”.

At the same time, ESG developments in the loan market – including the emergence of sustainability-performance loans that offer borrowers improved pricing if they meet ESG targets – means the loan option is not falling off the pace when it comes to engagement with corporate sustainability agendas.

White highlights the significance of Woolworths’ five-year tenor. He tells KangaNews the demand for green corporate bonds does not of itself solve all the challenges of the local credit market for issuers. Specifically, he suspects there would not be A$2 billion of 10-year demand for a green corporate deal.

Extended tenor is not easy for green-bond issuers, either. Campbell adds that it is hard, if not impossible, to certify non-infrastructure assets for longer-tenor green-bond purposes – specifically, for 10 years or longer.

But the type of competitive pricing Woolworths achieved at five years might hint at a new value paradigm for the local bond market in the mid-curve, which has historically been the sweet spot for Australian real money but where bank debt has always been the preferred option for local corporates.

Issuer commitment

Even so, Campbell acknowledges that companies need to have a wider commitment to sustainability to justify the preparatory work necessary for green-bond issuance. The payoff in funding cost and diversity can be evident, but issuers – especially those from new sectors – will need to deploy resources to certify and verify programmes. This process is likely to require management and board buy-in.

This certainly appears to have been the case for Woolworths. Marr says the company realised in advance of its A$500 million domestic bond maturity in March that there was an opportunity to do more than a straightforward refinancing transaction. He explains: “As a company, we have spent a lot of time and money on environmental initiatives so we thought that if the opportunity was there for a financing that aligned with those it would be one we should explore.”

It was not simply a case of identifying existing green-bond standards and mapping assets to those. Nathan Wong, treasury manager at Woolworths in Sydney, tells KangaNews the company wanted to be a “credible issuer” in the green-bond space and decided the best way to achieve this status was to meet the green-bond principles and to secure CBI certification.

The latter in particular took some work. “There were some existing CBI standards that some of our assets would qualify for, around things like energy efficiency – but that wasn’t enough for us,” Wong continues. “We wanted to make the low-carbon buildings standards work, but when we started the process these were really focused purely on office space.”

As a result, Woolworths commenced a six-month collaborative process with CBI to develop rigorous standards for supermarket premises. Marr says this also breached new territory for CBI.

Newly qualifying assets contributed A$390 million to a Woolworths pool which has aggregate volume of A$470 million, according Brown. He explains that the standards are stringent, so although Woolworths has a retrofitting programme that will build its qualifying asset pool this growth will likely be steady rather than exponential.

While the company does not have a specific forward target for transitioning more premises to this status, Marr says: “We definitely want to grow this asset base – not just because it is the right thing to do but because these assets provide a very good return.”

Corporate interest

The equation for potential corporate green-bond issuers is relatively clear: adding a commitment to sustainability across a business to a treasury department’s willingness to commit to robust issuance standards can produce a highly cost-competitive outcome with the much sought-after element of investor diversification.

“We hope the success of the Woolworths labelled bond will provide yet another signal to corporate issuers of the increasing appetite for sustainable product in Australian dollar fixed income,” Grow comments. “That said, success cannot be taken for granted and any prospective issuer must be able to demonstrate a credible sustainable issuance framework as well as a clear commitment to key investors in this market.”

Woolworths’ lead managers say the deal is already grabbing the attention of other borrowers. But the degree of commitment needed to unlock the best outcomes means corporate market growth will remain a work in progress.

“Even though we’ve seen a good spurt of green and sustainability issuance of late, I think we are still going through an education and awareness phase,” admits Katharine Tapley, head of sustainable finance at ANZ in Sydney. “Momentum builds with each new transaction type, whether it be social and sustainability bonds from New South Wales Treasury Corporation, Housing New Zealand and National Housing Finance and Investment Corporation or a retail-sector bond from Woolworths. It is really about continuing that process.”

The underlying trend is positive, though. “With every new deal the value of the market becomes more obvious to issuers,” Tapley tells KangaNews. “Wider developments, like the Australian Sustainable Finance Initiative, are also helping demonstrate what treasury teams can do to engage with corporate sustainability agendas.”

The path is easier for borrowers in sectors that have already established norms for sustainability-bond issuance. But Beattie says, in the corporate realm, this currently only really applies to REITs and banks. With just one obvious peer in the supermarket space, Woolworths will probably be a further proof of concept rather than a direct precedent.

“Sectors like infrastructure and airports are certainly interesting and there are some examples of deals from these internationally,” Beattie suggests. “There will be a next mover in Australia, but at this stage it is still hard to say exactly who will go next.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Vicinity’s domestic print shows ongoing appetite for real estate

Vicinity Centres’ Australian dollar return provides another example of investor support for a wider range of corporate sectors – in this case, an oversubscribed book coming in for an issuer in the retail real estate sector as it seeks to move on from the pains of the pandemic. The issuer says domestic market conditions proved attractive for pricing and tenor.

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.