Woolworths tests appetite with two SLBs

Woolworths priced two sustainability-linked bonds in September – the first time the issuer has taken advantage of the relatively new format – tapping the euro and then the Australian dollar markets. The issuer says the deals represent the evolution of its green, social and sustainability funding strategy.

Kathryn Lee Staff Writer KANGANEWS

Matt Zaunmayr Deputy Editor KANGANEWS

Woolworths priced a €550 million (US$647.7 million) long-seven-year sustainability-linked bond (SLB) on 9 September and followed with a dual-tranche, A$700 million (US$509.9 million) SLB on 28 September.

A Woolworths spokesperson tells KangaNews: “We have set ambitious emissions-reduction targets and want to play our part in addressing this urgent issue. We have committed to reducing our scope-one and scope-two emissions by 63 per cent from a 2015 baseline, which provides an important trajectory to link our bond to.” Woolworths has already reduced its emissions by 27 per cent since 2017, the company says.

The transactions share a sustainability-performance target (SPT) that covers absolute scope-one and scope-two greenhouse-gas emissions reduction, in line with a 1.5-degree Paris Agreement scenario. A 25-basis point margin penalty is built into the structure of both transactions, with test dates for each note about two years before their maturity dates.

HSBC structured the euro transaction and acted as joint lead with BNP Paribas, Citi, MUFG Securities and SMBC Nikko. Citi and HSBC were also leads on the Australian dollar note, alongside Commonwealth Bank of Australia and Westpac Institutional Bank.

The transactions form part of Woolworths’ commitment to increase its environmental, social, and governance (ESG) profile in capital markets, having issued a landmark Australian dollar green bond in 2019. They also represent the completion of the A$1.5 billion capital-markets funding Woolworths’ announced its intention to carry out in its FY21 results.

EURO EXECUTION

Woolworths is the second Australian company to issue an SLB in the euro market, after Worley printed the first on 1 June. Kate Stewart, Sydney-based managing director and head of debt capital markets at BNP Paribas, says marketing SLBs in Europe is a more intensive process than vanilla deals.

“Investors in Europe are interested in why targets are chosen, how ambitious they are and how they fit into a company’s overall ESG strategy, as well as the issuer’s credit,” Stewart notes. “But they are familiar with the structure now and do not require much extra time for it.”

Ian Campbell, Sydney-based managing director and head of debt capital markets Australia and New Zealand at Citi, adds that European investors were keen to gain an understanding of Woolworths’ position in the Australian retail market and understand the borrower’s intentions for ongoing issuance.

The deal was marketed to European investors as well as those further afield over two days. Andrew Duncan, head of debt capital markets Australia at HSBC in Sydney, says the group used SLBs from Tesco and Carrefour as reference points for the transaction. He adds that Woolworths connected with more than 180 accounts during the roadshow.

Luke Spitty, managing director at SMBC Nikko in Sydney, says the borrower took an open approach to its issuance timeline, allowing investors adequate time to analyse the credit. He notes investors were receptive to the deal in a busy market and the SLB format garnered attention, adding to demand.

While European investors are still widely acknowledged as the global leaders in demand for ESG debt, a particularly pleasing element of the Woolworths deal was interest and participation from investors outside Europe, according to Violeta Kelly, director, debt capital markets at MUFG in Sydney.

Kelly says more Australian investors engaged in the deal than would be expected in a typical Australian-origin corporate transaction in the euro market.

This demand may not be entirely related to the SLB format, however. Spitty says the level of engagement from Australian fund managers is also part of a developing trend of increasing participation from local accounts in Australian corporates’ offshore deals.

The final book was in excess of €2.1 billion. Campbell says this is one of the larger single-tranche books for a triple-B-rated Australian corporate in the euro market. The level of demand allowed for final pricing of 60 basis points over mid-swap after the deal was initially marketed at 90-95 basis points.

AUSTRALIAN FOLLOW-UP

Deal participants say they were pleased with the result of Woolworths’ domestic market follow-up, which garnered strong interest. This was despite domestic-market sentiment being slightly below its peak as the China Evergrande situation gave market participants reason for hesitancy. At its peak the transaction was A$2.9 billion oversubscribed.

Comprising long six- and 10-year tranches, Duncan says the dual-tranche diversifies Woolworths’ maturity towers, while also allowing access to different points of demand. However, he notes final support came across the maturity profile, with many investors showing interest in both tenors.

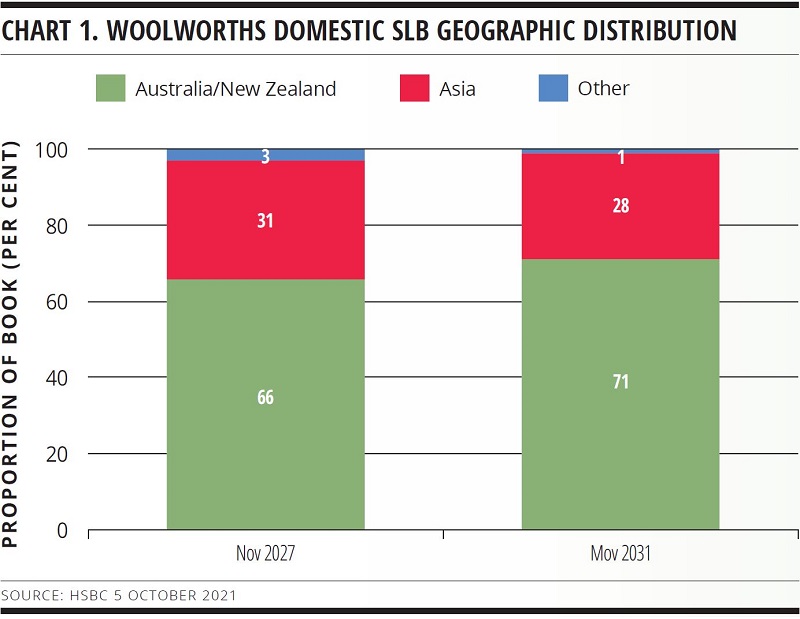

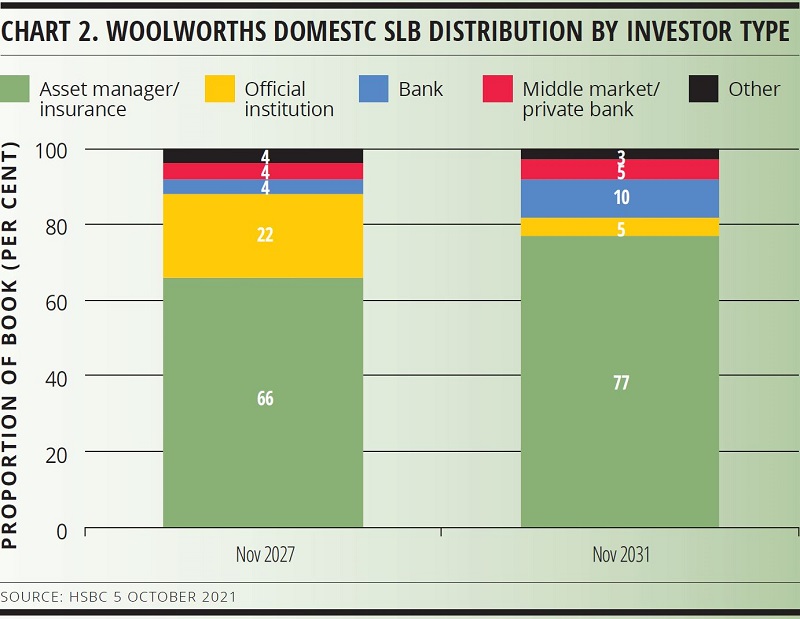

Australian and New Zealand investors dominated the book, with the remainder mostly from Asia (see chart 1). Asset managers and insurance companies formed much of the demand in both tranches (see chart 2).

Coming to market a little more than a week after Woolworths’ euro deal, Peter Block, head of DCM at Westpac in Sydney, says the back-to-back nature provided some execution advantage – such as adding another data point to work from. But he notes that other elements also played in the deal’s favour.

Final pricing was 75 and 117 basis points over semi-quarterly swap for the long six- and 10-year tranches, having been marketed at 90-95 and 130-135 basis points.

Block points out that many investors were ready to look at the opportunity before the deal was even announced, with several waiting for a domestic offering given the funding intentions announced in Woolworths’ FY21 results. “Woolworths is a rare borrower with a business that is very well respected and understood in Australia,” he says. “We were also bringing a structure that I think investors were attracted to. This all had an impact on pricing.”

GREEN ADVANTAGE

According to Woolworths’ leads, both deals attracted a “greenium” of at least 5 basis points, though they acknowledge it is difficult to quantify. MUFG’s Kelly notes the euro transaction managed to hold onto typically price-sensitive accounts due to their specific sustainability focus. Additionally, KangaNews understands one of the world’s largest ESG fixed-income investors participated in the euro deal with a larger bid than it typically would offer an Australian corporate borrower.

Duncan says the ESG link is attractive. “I think the reality is investors become more emotionally involved in these types of transactions,” he comments. “They want to buy these bonds more than they would the vanilla day-to-day bonds they have been

investing in for a variety of years.”

He adds that sustainability-themed bonds generally perform better in the secondary market, which also contributes to demand. “Investors are loathe to part with them at points of volatility because they are harder to replace,” he explains.

Block says SLBs are on every issuer’s radar, but notes they are not always appropriate. “These sorts of securities are really only

relevant to a certain subset of companies, and issuing an SLB – or continuing to issue SLBs – is not an option for every corporate

borrower,” he says, noting it depends where the issuer is on its ESG journey.

SLB issuance began in Europe in 2019, but has become more prominent in 2021. According to Climate Bonds Initiative, SLB

issuance is on the rise as more corporates seek funding not tied to specific projects. In the first half of 2021, issuance reached

US$32.9 billion compared with zero issuance recorded in the same period last year.

Block adds that a duplication of Woolworths’ dual-market offering is possible, but such quick-fire issuance is only applicable to a handful of companies given the minimum transaction sizes required in both markets. At least one other borrower is considering a similar issue, Block notes.

In the short term Block expects the market will see a lot more use-of-proceeds (UOPs) and SLB issuance. He adds that participants are probably more comfortable with UOPs due to their simplicity. “Issuers cannot just replicate the structure required for these transactions,” he says. “It needs to be tailored to the company, its ESG strategy and what it is trying to achieve.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Vicinity’s domestic print shows ongoing appetite for real estate

Vicinity Centres’ Australian dollar return provides another example of investor support for a wider range of corporate sectors – in this case, an oversubscribed book coming in for an issuer in the retail real estate sector as it seeks to move on from the pains of the pandemic. The issuer says domestic market conditions proved attractive for pricing and tenor.

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.