Reboot, reset or reconstruction?

Perhaps the biggest hope to emerge in capital markets over the course of 2022 is that the year represented the dose of medicine the fixed-income asset class in particular needed to re-establish its fundamental value after a protracted but ultimately unsustainable bull run. Whether we are experiencing a return to normal or the beginning of a fundamentally new phase remains to be seen.

Laurence Davison Head of Content KANGANEWS

I cannot prove it now, but I distinctly remember telling a family member during the early days of the global financial crisis that I believed the absolutely fundamental cause of the malaise was that we – by which I mean the global developed world, for the most part – had been acting richer than we are for several decades.

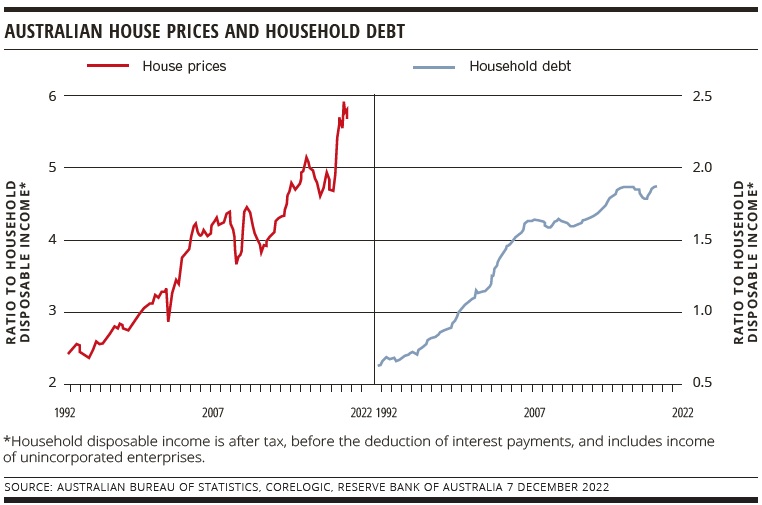

We were, in effect, maintaining the income growth of the mid-20th century by using private sector credit to push up asset prices. For instance, a generation of home owners got used to their properties rising in value on a trajectory growth asset classes would be proud of – a phenomenon made possible because there was always another buyer willing to load up on debt to buy said property.

Australian household debt grew nearly threefold as a proportion of income between the early 1990s and the eve of the financial crisis, accompanied by the seemingly ever-upward climb of house prices (see chart).

The financial crisis saw private sector borrowing supplemented by government debt. We can see in retrospect that crisis-era QE was not a temporary measure used to prop up the financial system during a stressed period – or, at least, it was not just that. The ‘Japanification’ of much of the developed world emerged slowly, pushed ever onwards by the Fed put, successive taper tantrums, the Eurozone sovereign debt crisis and other events. But it was clear leading into the pandemic that permanent government deficit was increasingly hard-wired into the system.

The situation was intractable because people and their leaders could not confront the reality of a step-down in standards of living in the developed world. Governments attempting serious fiscal consolidation found themselves on the end of public unrest. There are more factors at play in the catastrophic recent economic history of the UK than the austerity policies of the early 2010s but it is not hard to draw a straight line from them to Brexit and beyond, for example.

It is also worth noting at this point that public- and private-sector debt have supplemented, rather than substituted for, each other since the financial crisis. Australian household debt may have stayed relatively flat for a couple of years after the financial crisis but it started climbing again in the 2010s even as the sovereign stayed in deficit. US household debt resumed its growth in 2013 and has stayed on a rising trajectory ever since, even as the US government has not returned a surplus since 2001.

PANDEMIC RESET

At this point it might have been thought that central banks, governments and households were running out of bullets. The taps might not have been on full blast by late 2019 but the attempt to prop up wealth meant we were borrowing from anyone who would lend – increasingly including our future selves.

Let’s not forget, for example, that QE was being widely discussed as a 2020 option for the Reserve Bank of Australia well before anyone outside the scientific community knew what a “coronavirus” was – and despite the Australian economy recording 2.1 per cent growth and local house prices rising by 6 per cent in 2019. CPI inflation was a moribund 1.9 per cent at the end of the year and most economists, analysts and market participants had given up predicting its resurgence even as a vague spectre.

COVID-19 changed the game – perhaps even more than the financial crisis had a decade or so previously. Governments that were at least flirting with the idea of surplus as an achievable goal were effectively forced to underwrite vast swathes of their economies, funded by debt issuance on a massive scale that was largely swallowed up by central bank QE programmes. If we were borrowing from our future selves before the pandemic, its arrival pushed the burden of that debt out through generations.

For a few months, the public sector overwhelmed accumulation of household debt. Australian household debt fell in the pandemic years and consumers actually started saving money. But this was really just the equivalent of the beginning of a First World War offensive: the front line went quiet during the massive artillery bombardment, but as soon as the big guns fell quiet the chatter of small arms fire commenced once more. Australian household debt surpassed its pre pandemic level in 2022.

Some things have clearly changed, though. The most speculative asset classes have taken a battering in 2022. At the other end of the spectrum, fixed-income investors are optimistic that fundamental value has re-asserted itself in their sector after a painful year of correction. To borrow Paul Keating’s phrase, this might be the correction the bond market had to have. Certainly, the market is facing into 2023 with a more positive feeling about longer-term value – assuming the rates cycle really is somewhat close to its summit.

There has also been a significant, though not yet catastrophic, correction in the housing market. Nationwide, property prices have fallen by more than 6.5 per cent since their peak in April 2022, according to CoreLogic, and most analysts expect the decline to continue as rate hikes filter through to borrowers.

LACK OF WEALTH EFFECT

However, the level of decline in the housing market so far has been pretty benign given the circumstances – including the scale of growth prior to 2022. House prices in Australia more than trebled from 2000 to their recent peak, including adding 30 per cent in the run driven by ultra-low pandemic-era mortgage rates.

Just like the bond market, it could be argued that housing needs a fundamental reset in Australia. The rate of home ownership continues to drift downwards – to 66 per cent in 2021 from a peak of more than 70 per cent in 2000. The decline may not seem dramatic but the current level is an all-time low and marks the first significant change since the middle of the last century.

It is not getting easier to become a home owner, either. Falling prices have so far been more than offset by higher mortgage rates, to the extent that Australia is adding a serviceability issue to an affordability one. Record low unemployment means the credit quality of mortgage books is holding up well – surprisingly well, many lenders admit.

I view the housing market as a proxy for a wider issue, the resolution of which will likely determine the next phase of socioeconomic evolution in the developed world. People were, in the main, relatively unconcerned about wealth inequality even within their own nations for as long as the rising tide of overall growth continued to lift wealth for most. In effect, people were able to ignore the billionaire’s private island while they were able to have an annual foreign holiday.

This may no longer be the case. The world is clearly in a lower-growth phase – even if we can acknowledge that growth we enjoyed in the previous period was turbocharged by debt. This is even before factoring in the impact of decarbonisation – a change we need to make, but one with significant up-front cost and that will profoundly alter the world’s ability to draw on ‘free’ natural capital and apparently low-cost energy.

Will people be as willing to witness the concentration of wealth, whether it be in the hands of the unaccountable ultrawealthy or just the common-or-garden property investor, when they do not have the same positive outlook on their own long-term prospects?

My suspicion is that it will become harder and harder for the centre to hold. Our economies are set up with a system of incentives designed to protect and grow wealth, especially in the housing market but also across investment asset classes. As more people find they are deriving little or no benefit from this system, demands for change will surely only grow.

Recent years have seen a worrying flirtation with the far right in many developed countries. While I don’t fully subscribe to the ‘economic anxiety’ theory of contemporary populism, there can be little doubt that people with little to lose or who feel what they have is under threat will generally be more willing to take what they consider to be a political gamble. It is more likely to seem a good idea to roll the dice with political leadership when the status quo looks like a losing proposition.

How this plays out is impossible to know. There could be further gains for the far right, an equivalent rise in old style leftwing politics or some combination of the two, under which prejudices and demands come together in a desire to take wealth from a perceived ‘elite’. On the other hand, we may be able to hope for a soft landing whereby the gateway to financial security is reopened for many.

If this is to happen, though, it surely cannot be via the old playbook of fiscal austerity being borne in large part by the people who are already experiencing financial disenfranchisement. We have to find a way, in other words, to keep letting air out of the accumulated pile of public and private-sector debt that also improves rather than weakens financial equality.