Carpe diem for Australian fixed income

The economic outlook is weak and the world is suffering an apparently unceasing pipeline of risk events. Meanwhile, the looming US election carries the threat of geopolitical and environmental catastrophe. Nonetheless, the Australian fixed-income market ecosystem is in rude health. Market participants looking to 2024 and beyond should be thinking about how to capitalise on recent success to solidify and multiply local capacity.

Laurence Davison Head of Content KANGANEWS

It might not be the most headline-grabbing development capital markets have witnessed in recent years – if you haven’t been reading KangaNews or don’t make your living in the debt market you will almost certainly have missed it – but capacity growth in Australian dollar fixed income might produce as significant a change in the role and relevance of the market as anything else.

The past year saw a number of issuance records broken in the Australian dollar market, including the biggest ever volume printed in sectors like securitisation and the supranational, sovereign and agency (SSA) Kangaroo market. But outright volume numbers do not always tell the full story. Supply is the product of issuer need as well as investor demand, and if funding requirements are not growing – as is the case in, for instance, the local sovereign sector – deal flow will inevitably be capped.

Perhaps the best demonstration of Australian dollar capacity is the outcome for a sector that has ample headroom to issue in this market: the local big-four banks. With something in the range of A$120 billion (US$80.1 billion) or more of annual wholesale funding to complete, the prevailing wind of international flows to and from Australia has always had its direction set by the majors. Indeed, the gap between what the big four can issue at home and their total funding task is, historically, a major contributor to Australia’s need to import capital.

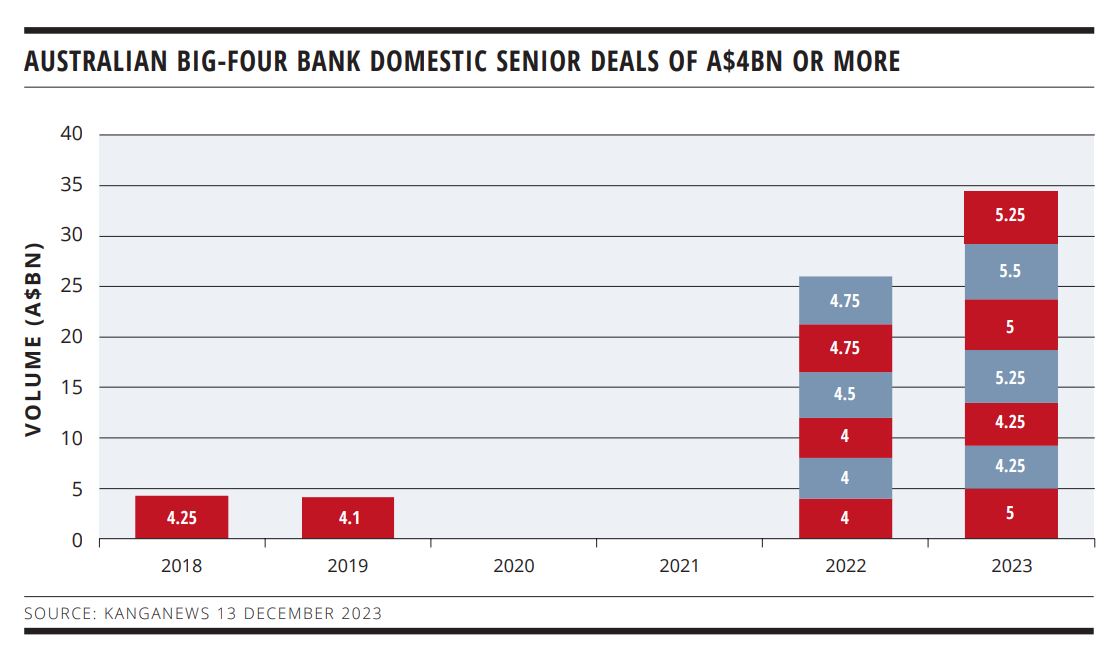

It has become increasingly clear in recent months that the majors should be able to plan for a future in which the domestic market provides a larger proportion of their issuance need. Transaction sizes demonstrate the step-change in local capacity: Westpac Banking Corporation was the first of the majors to print a deal of more than A$4 billion, in 2018. The pandemic iced the big four’s public funding needs, but since 2022 deals of this size – and, more recently, of A$5 billion or more – have become the norm (see chart).

Elsewhere in this edition of KangaNews, the big-four banks’ heads of funding suggest that larger deal books have gone from a surprise to an expectation in the domestic market. There are hopes that the Australian dollar component could provide half their overall issuance need, from the historical norm of more like 30 per cent. This degree of increased proportional issuance could itself mean more than A$25 billion of incremental annual supply to the domestic market.

Capacity growth is not just evident in the credit sector. For instance, at several KangaNews forums in 2023, Australia’s largest semi-government issuers commented on the way their increased ongoing call on markets has been comfortably absorbed in their domestic currency, with more bonds on issue going hand in hand with much greater turnover and improved liquidity.

The drivers of increased demand are fairly well known at this stage. Higher rates and better relative value to other asset classes – especially equity – have attracted domestic real money, while similar yield factors and less competing supply have increased Asian investor interest in Australian dollar product. These may be cyclical effects, but many market participants are prepared to predict that a much more visible superannuation investor presence in the debt market is part of a structural shift as funds under management grow and the population ages.

DIVERSITY DRIVE

To some extent, increased volume has also meant greater diversity of issuance – especially in the credit sector. Financial sector issuance has arguably never been more vibrant, especially if structured finance is taken into account.

Local and global banks have generally had positive experiences in the Australian dollar market this year, especially those that have taken the time to build good investor connections: the Singaporean banking complex, for instance, provided nearly A$7 billion of new issuance to the Australian market in 2023, comfortably doubling any previous year.

The securitisation space, meanwhile, has welcomed a more diverse set of issuers and collateral types than ever – including its own doubling, to more than A$10 billion, of new-supply securities backed by auto collateral.

The message does not yet seem to have reached corporate Australia, however – or, at least, not all of it. There were some truly exceptional outcomes for corporate deals in 2023, most recently the A$600 million printed by Coles from a book of more than four times this volume, with half the demand coming in for a rare Australian dollar 10-year tranche. Other recent transactions may have had lower profiles and aggregate corporate issuance for the year was unspectacular, but it does not seem that credit appetite is restricted to financial names.

SSA borrowers have noticed, too. At least one major name tells KangaNews it will be prioritising engagement with the Australian domestic real-money investor 35 base, which has historically been lukewarm on the sector. Elsewhere, new issuers and recent debutants from the global high-grade sector have found supportive investor bases in Australia and offshore, adding a lot of the incremental supply that drove a record SSA issuance year of more than A$35 billion.

FILLING A GAP

Looking ahead, the issuance trends of 2023 spur two critical questions. One is whether this scale of demand is reliable or something that cyclical and relative value changes will bring back to earth. The other is, if the market really has experienced a step-up in capacity, what makeup of supply can be found to satisfy Australian dollar appetite?

The first question may be impossible to answer but most indicators are positive. While the conducive issuance environment of 2023 was certainly the product of a number of positive factors coinciding, it would be wrong to think of it as a perfect storm. Plenty of domestic fund managers have remained relatively cautious about credit, whether this view manifests itself in ongoing reluctance to extend tenor or caution about bid sizes or aggressive pricing.

The Japanese bid, meanwhile, faced challenges throughout the year. Yen weakness is an ongoing problem for unhedged FX buyers – and the cost of hedging made doing so challenging, too – while the first steps toward local monetary policy normalisation could, some believe, lead to a significant repatriation of Japanese investor funds.

There are, by contrast, signs that the baseline level of demand in the Australian fixed-income market has grown. This likely does not reflect a fundamental redrawing of the norms of local asset allocation, however. Rather, it is the product of the sheer weight of funds in the local superannuation sector, where population growth, increased contributions and the gradual shift of superannuation member demographics toward the retirement phase all tend toward more funds being tipped into the income basket.

In short, issuers have every reason to think the domestic market ecosystem is supported by a robust level of fundamental demand that may ebb and flow to some extent but will do so from a higher baseline than before.

If this is true, the next question is supply. The current and forecast economic environment makes it hard to anticipate significant expansion in corporate issuance, for several reasons. Investment-grade borrowers are unlikely to be in expansionary mood or to have much appetite for ramping up gearing. Investor caution is already in evidence – particularly in some sectors that have been major contributors to the Australian market, such as real estate. And the chances of a local high-yield bond market flourishing have barely improved since the pandemic – especially as sources of private capital continue to proliferate.

There are reasons to be optimistic about further development of the Australian financial institution credit market. Domestic credit growth likely caps the volume local banks will fund, locally or offshore, but a more competitive deposit market and – perhaps – greater regulatory value placed on term wholesale funding in the wake of bank runs in the US and Europe in 2023 should mean issuance continues to flow relatively freely.

Alongside SSAs, there is every reason to think international banks will be an ongoing component of Australian dollar credit issuance. Perhaps what is needed here is a few more eye-catching transactions: if issuers believed they could reliably access deal sizes at least comparable with what they issue in the US and Europe, with consistent volume and competitive pricing, Australia could become a much more strategic option.

The main game, however, ought to be financing the energy transition. If the scale of financing need is as great as estimates suggest – close to A$2 trillion – a vast quantity of debt capital will be required. The question here may be scale: the Australian market will certainly favour substantial projects from well-established corporate or government names.

It is not going to be a free kick. Local super funds have pushed back hard on political pressure to adopt, effectively, ‘national interest investment’ strategies while they are at the same time facing demands to demonstrate their investment is in the best financial interests of members. The local bond market, meanwhile, is not traditionally well-aligned with early stage, development or project risk. Still, it is hard to imagine the Australian dollar debt investment pool not playing a major role in a task of this size.

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

New Zealand's market ready to step up as degree of difficulty grows

With a substantial infrastructure requirement looming and a weak economic environment, the New Zealand capital market will have to be on top of its game in the years ahead. Participants at KangaNews’s annual women in New Zealand capital markets roundtable discussed the issues at hand and how they believe a constructive ecosystem can be developed.

New Zealand looks for the silver lining despite economic headwinds

Speakers at the ANZ-KangaNews New Zealand Capital Market Forum, which took place in Auckland on 21 March, believe the local market continues to offer opportunities despite the obvious challenges of an economy in recession. The everincreasing urgency of the energy transition, a significant infrastructure shortfall and the role of the fixed income market took centre stage in discussions.

Foundations for the future

The KangaNews Debt Capital Market Summit 2024 took place in Sydney on 18 March amid an unprecedented bonanza of new issuance and at what could prove to be an inflection point for the local market. The agenda covered a raft of topics centred on the theme of taking advantage of recent growth to deliver a market that is match fit for the demands that will be placed on it, with discussions ranging from the impact of geopolitics and global economic currents to the need to stay ahead of accelerating technological advances.