Small steps to subinstitutional scale

For the finance industry to support low-carbon economic transition to the fullest extent, sustainability principles must be applied across the business landscape and not just to the largest companies. However, the challenges are magnified for companies without the resources of the institutional sector.

Matt Zaunmayr Deputy Editor KANGANEWS

The takeup of sustainable debt among Australian companies – particularly the adoption of sustainability-linked loans (SLLs) and, most recently, sustainability-linked bonds (SLBs) – has been notable in 2021. More deals have been done, across a greater variety of sectors, than ever before.

Even companies that have not yet borrowed in any sustainable format are experiencing enhanced demand for reporting and disclosure on environmental, social and governance (ESG) standards – from banks and capital-market investors.

However, engagement with sustainable finance remains focused on institutions at the big end of town. The only corporate issuers to access the Australian dollar GSS or SLB markets in the year to the end of August 2021 have been Lendlease and Wesfarmers. Large companies – such as Coles, Incitec Pivot, Ramsay Health Care, ISPT and a clutch of public-private partnership (PPP) sponsors – also dominate the list of ESG-labelled loans.

There are reasons for this concentration. Larger companies typically have sustainability teams, in-house and often positioned alongside treasury, dedicated to identifying sustainability-related risks and opportunities. These teams can facilitate the reporting and disclosure necessary for labelled debt facilities as financing increasingly becomes a focus of corporate sustainability efforts. Large businesses are also at the pointy end of public, investor and regulatory scrutiny – doubly so if they are listed entities.

External pressure – from capital-market investors and regulators – for smaller businesses proactively to address sustainability risk has not been as great. At the same time, the tools big companies are deploying to understand and report on ESG factors have not been available to smaller companies.

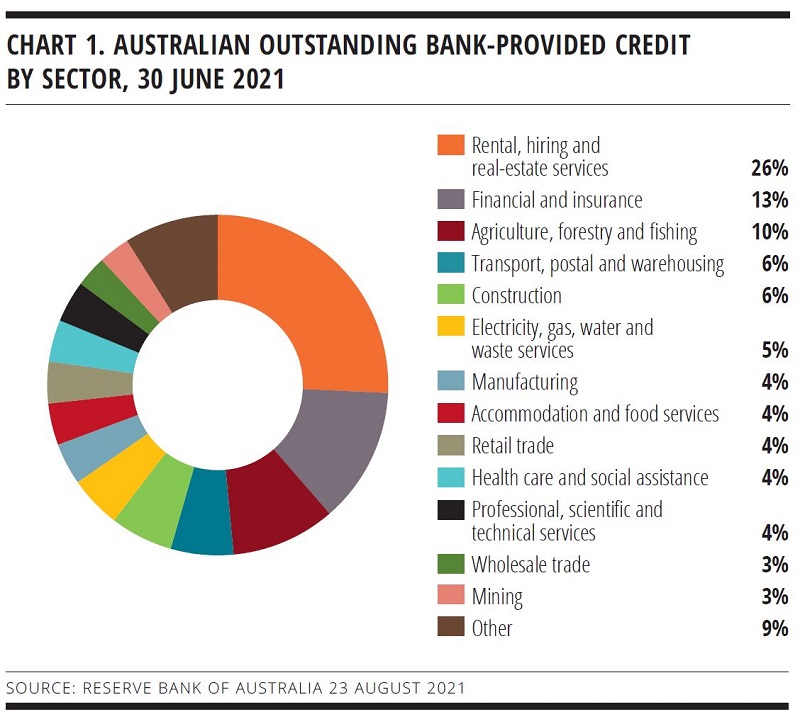

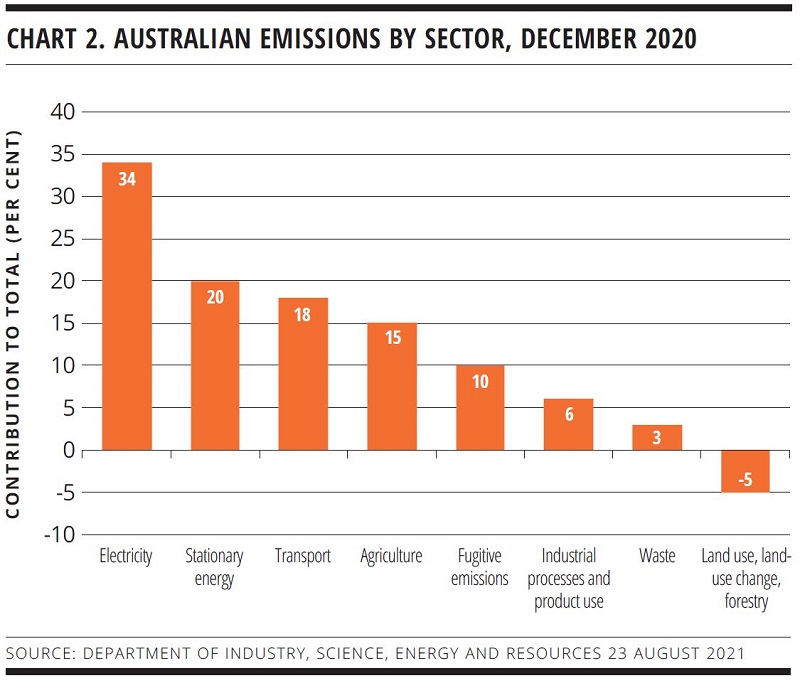

But these businesses are relevant. Sectors like agriculture and transport – neither of which have yet figured to the fullest extent in the Australian institutional GSS market – should play a large role in the transition to a low-carbon economy, and also figure prominently in Australia’s lending landscape (see charts 1 and 2).

CIRCULAR CHALLENGES

Financiers say the challenges smaller companies face in accessing sustainable finance predominantly relate to education, resourcing and scale. The self-reinforcing nature of these challenges is a compounding factor.

For example, a small company is unlikely to dedicate the necessary resources to sustainability if it is not sufficiently aware of the related risks and opportunities. Without these resources, even if the company comes to understand the risks it needs to mitigate and opportunities it can exploit, it will not be able to undertake the sort of measurement, reporting and disclosure sustainable finance requires.

Rory Lonergan, executive director, infrastructure and alternatives at Clean Energy Finance Corporation (CEFC) in Sydney, tells KangaNews: “Significant knowledge gaps exist across the economy. This is starting to fill at the top end of town, where businesses now often have sustainability resources. But education on the costs and opportunities of emissions reduction is still required for many.”

However, Charles Davis, managing director and head of sustainable finance and ESG at Commonwealth Bank of Australia in Sydney, says interest in sustainable finance is growing among smaller companies and many are seeking to expand their knowledge of the sector.

“We are seeing a lot of interest from companies in the basic concepts of sustainable finance, such as the difference between use-of-proceeds [UOP] financing such as green loans and SLLs incorporating forward-looking KPIs,” he reveals.

It is not a quick process, though. Years of reporting on sustainability and interaction with bankers and other investors precede public debt issuance for most large companies now availing themselves of sustainable-finance options. Smaller borrowers that are only just beginning this process cannot be expected rapidly to become ready for labelled finance.

RESOURCING AND REPLICATION

As the sustainable-finance market as a whole strives for greater understanding of impact, the barriers to entry may actually be getting higher for smaller businesses. Collecting data and reporting on sustainability metrics and outcomes is inherently resource-intensive and will likely always be a challenge.

Sustainable-finance reporting requirements may at this stage simply be a bridge too far outside the institutional space. In agriculture, for example, Jasmin Jenkins, CEFC’s Sydney-based director, says most farms remain family-owned and operated even if they are very large. Many farmers intuitively understand the benefit of sustainability, given the farm is an intergenerational asset, but are yet to use data to back up any sustainability measures they may be taking.

One option for truly subinstitutional-sized businesses is aggregation facilities. Market participants say these are proliferating among bank and nonbank lenders, to provide discounted lending for green assets such as electric vehicles and solar panels (see box).

The biggest resource gaps might actually be in the middle market. Bankers say these could be filled by means other than in-house capability. Bank sustainable-finance teams – particularly at the major banks – have become significantly better resourced in recent years. At the same time, the proliferation of sustainable-finance transactions means more relevant – and potentially replicable – examples are available for smaller borrowers.

Combined, these factors mean banks may be able to offer a greater hand to smaller companies seeking to use sustainable finance to aid their transition.

But Davis says it will never be as simple as intermediaries taking a sustainable-finance transaction executed by a large company and applying it directly to a smaller one. He explains that banks still need to understand the specific challenges for each sector and each company in depth.

It may be possible to develop a degree of uniformity in parts of sustainable finance, for example sector-specific KPIs for sustainability-linked transactions. Even large borrowers say application of more consistent KPIs across transactions could be helpful in expanding the market – though the bespoke nature of SLLs is undeniably part of their appeal. Ensuring targets are credible and ambitious while still being achievable may not fit with a cookie-cutter SLL concept.

National Australia Bank (NAB)’s Sydney-based head of sustainable finance, David Jenkins, believes replicable KPIs could be achieved in some sectors. Emissions-reduction targets are the most commonly used in SLLs and SLBs, and Jenkins says these could be replicated by smaller companies in some sectors.

“Tailored KPIs are much more challenging to implement for smaller, bespoke transactions. But there are opportunities. It is just a matter of identifying what is material in each sector then ensuring it is measurable, relevant, credible and scalable for individual companies,” Jenkins explains.

Davis agrees, adding that banks should be focused on removing friction from the sustainable-finance market. “We do not need to reinvent the wheel for each transaction but availability of data is critical in developing and baselining metrics, and every organisation is at a different stage. Smaller companies could perhaps focus on a more limited number of metrics to ease the resource burden, but KPIs will always be bespoke to a degree.”

Significant market development will likely be needed for smaller companies easily to be able to identify and apply relevant sustainability KPIs to their financing arrangements.

Julia Hinwood, Melbourne-based infrastructure lead at CEFC, says: “SLLs currently have no consistency in application and can be used for a range of ESG outcomes. CEFC’s focus on carbon-emissions reduction means we apply more targeted criteria to investment. We may need more granular categorisation for SLLs to improve their transparency and consistency.”

The Australian Sustainable Finance Initiative (ASFI) has included a sustainable-finance taxonomy as a medium-term goal – to be achieved between 2023 and 2025 – in its roadmap. This could provide similar granular categorisation of sustainability measures and outcomes as the EU’s sustainable-finance taxonomy.

Replication may be more immediately achievable in UOP sustainable finance, where qualifying assets are more clearly defined by international standards. PPP sponsors, for instance, have now taken green-loan financing for low-carbon transport assets in Canberra, south-east Queensland and Sydney.

The impetus for these came at least in part from commonalities among the ownership and banking groups, and in the assets being financed, with expertise applied to one PPP then being transferred to the others.

CEFC’s Lonergan tells KangaNews large lenders can play a role in education and addressing the resource gap, as well as providing guidance on sustainability goals and outcomes – even at a significantly smaller level than major PPP projects.

Ultimately, though, he says the impetus needs to come from companies themselves – no matter how big or small they are. “We need to impress upon companies that sustainability is not just a burden they need to bear, it is good business,” Lonergan adds.

Retail scale-up

Most companies will not have the required volume of assets to package into a use of proceeds (UOP) sustainable-debt transaction, or the overall scale for an institutional KPI-linked loan facility. However, retail channels and aggregation facilities for green finance are proliferating.

Much of the progress that can be made toward a low-carbon economic transition is through small business. Examples include the replacement of a small business’s vehicle fleet with electric vehicles (EVs) or the instalment of solar power and thermal efficiency measures on premises.

Unless these are done by companies with the scale to access institutional markets it is unlikely there will be a financing incentive to undertake these types of steps. However, in aggregate they are potentially even more meaningful for economic transition and at the same time could become sought-after institutional assets once enough scale is gained.

WORK IN PROGRESS

Financiers are well aware of the importance of sustainable finance becoming more widely deployed across the economy. They say progress is being made despite the challenges.

NAB’s Jenkins reveals there has been some penetration of sustainable-finance principles into smaller companies, particularly in sectors where sustainability issues and ESG risks have been to the fore for some time – such as agriculture and property. In agriculture, he says lenders can offer incentives for measures such as emissions reduction, water and land use, and biodiversity. In property, the focus has typically been emissions reduction and energy efficiency.

Agriculture appears to be an increasing focus across the finance sector. Davis explains that, in July, CBA executed the Australian agriculture sector’s first SLL, with beef-producer Stockyard. He reveals that the three-year facility includes targets for emissions reduction, animal welfare, and workplace health and safety.

Meanwhile, CEFC’s Hinwood tells KangaNews solutions have been possible in regenerative agriculture financing. She says these are not groundbreaking in the method of farming per se but they oblige the measurement of operating decisions and productivity so farmers can have more informed conversations with their lenders once they have proof of a more productive asset.

She adds that downstream demand for sustainable practices in agriculture is increasing, particularly from food producers and retailers that are in turn keen to demonstrate their sustainability credentials.

Elsewhere, CEFC sees great opportunity in applying sustainable finance to greenfield infrastructure such as for social housing, hospitals and rail. These assets are largely debt financed, and it is much more effective to establish sustainability measures from the outset than to retrofit them.

Hinwood says one challenge in including sustainability measures in greenfield infrastructure plans is that operators are often working within bid constraints, which can crimp ambition. The benefits of starting with high ESG standards are clear, though.

Hinwood uses the example of a new logistics park in Sydney’s outer suburbs. By implementing sustainability measures from the outset of construction and mode-switching to rail, the logistics park achieved CO2 equivalent savings representing a 77 per cent reduction compared with a business-as-usual freight-delivery scenario.

There may be even greater opportunities to make a difference to smaller companies through private-equity transactions. Lonergan says CEFC can more effectively embed the need for a company to understand and measure its emissions profile through the lifecycle of an investment via its private-equity funds.

Ultimately, harmonised standards and minimum levels of sustainability ambition will be needed throughout the economy to achieve the widest possible application of sustainable-finance practices, including for mid-market companies and SMEs.

NAB’s Jenkins says it is vital to find ways of incentivising lending to help businesses of all sizes improve their sustainability profile. “The urgency has not been as pronounced for smaller businesses, but this is changing. We have seen a step-change in sustainability ambitions for larger corporates, especially this year, and the same thing is coming across the economy.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news