Socialising the bond market

Australia’s burgeoning green-bond market was supplemented in March by the issue of the country’s first benchmark social bond. Key deal sources discuss the considerations behind the transaction at issuer and market level, and lay out the challenges that may lie in the way of substantial growth.

Laurence Davison Managing Editor KANGANEWS

National Australia Bank (NAB) priced its “social bond (gender equality)” on 17 March. The bonds “enable institutional investors to invest in supporting Australian organisations that champion women and equality in a positive way”, the issuer says. It also highlights the role the bond plays in its wider work to support the development of socially responsible investment (SRI) options in the Australian debt market.

Proceeds of the NAB social bond are not tied to specific projects. Instead, the companies receiving the funds raised come from a group that qualify as “employers of choice for gender equality” with Australia’s Workplace Gender Equality Agency (WGEA) and that meet NAB’s own social-bond framework requirements. Sustainalytics offered a second opinion on use of funds and EY provides financial assurance.

The organisations included in the initial portfolio are concentrated – though not exclusively found – in the professional-service sector. They are Ashurst, Australian Catholic University, Clayton Utz, Corrs Chambers Westgarth, Gilbert + Tobin, Henry Davis York, King & Wood Mallesons, KPMG, Lendlease, Minter Ellison, Mirvac, Monash University, PwC and Stockland. Two of these – Monash University and Stockland – are already leaders in Australian social finance, having issued their own green bonds in international markets.

The social bond is structurally similar to the established green-bond asset class, in particular the fact that it is a senior-unsecured debt obligation of NAB with restricted use of proceeds. This differs from the social-impact bonds issued by the New South Wales (NSW) government in 2012, which are effectively a securitisation of revenues from specific social-impact projects.

Other government-sector entities in Australasia are exploring social-impact bond funding, including the states of Queensland and Victoria and the New Zealand government. But the vanilla structure of NAB’s social bond significantly increases deal capacity by facilitating access to the widest group of mainstream institutional investors.

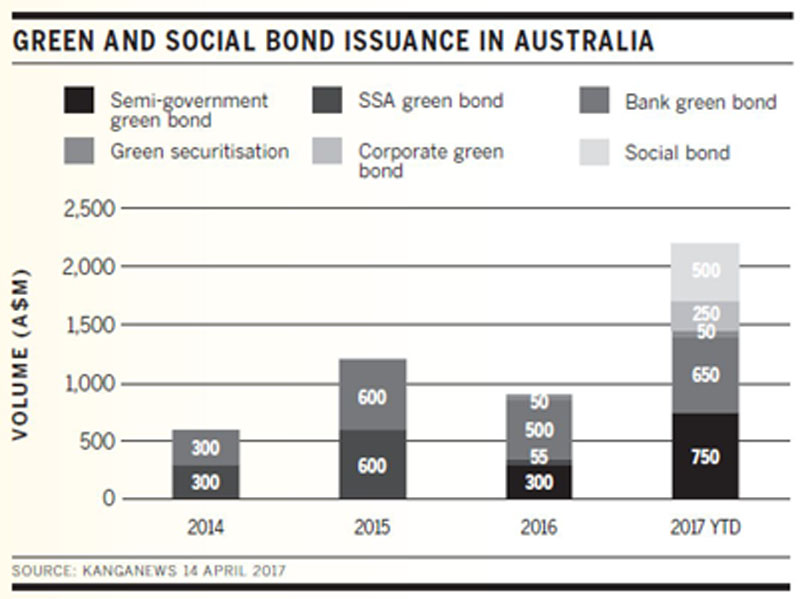

NAB raised A$500 million (US$379.2 million) of five-year debt via its social bond at 95 basis points over swap – a pricing level the issuer says was flat to its mainstream wholesale-funding curve. The deal adds to the momentum in green and social debt issuance in Australia, which is already running at a record level and includes breakthroughs such as the first domestic corporate transaction (see chart on right).

ICMA foundations

According to James Waddell, director, capital financing at NAB in Sydney, the social bond was around 18 months in the making. Impetus was provided in June 2016 when the International Capital Markets Association (ICMA) published its guidance for issuers of social bonds. This provided a definition of the asset class including a range of potential issuance categories and target populations, as well as explicitly comparing the characteristics of social bonds to green bonds.

“We were already thinking about and discussing a social transaction by this point, but we received positive investor feedback around the ICMA guidelines and the appetite for the product from this point on,” adds David Jenkins, Sydney-based director, capital financing at NAB.

The ICMA social-bond guidelines form a subset of its green-bond principles. The basis for the wider interpretation is the association’s acknowledgment of “the application of the ‘use of proceeds’ bond concept to themes beyond the environment, such as bonds financing projects with social objectives, or with a combination of social and environmental objectives”.

Catalina Secreteanu, associate director, institutional relations at Sustainalytics in Sydney, explains that the introduction of the social-bond guidance in 2016 paved the way for mainstream product like NAB’s gender-equality bond. She compares the principles to those that set out the standards for the green-bond market, explaining that they discuss the impact of social transactions, the use and management of proceeds and what areas can in general be considered to be of social benefit.

As a result, the ICMA guidelines, despite being less than a year old, are becoming the widely accepted basis for social-bond issuance. For instance, Starbucks was the first corporate issuer of social bonds when it debuted with a US$500 million transaction in May 2016. This was prior to the publication of the ICMA guidelines, but Starbucks aligned its follow-up social-bond deal – a ¥85 billion (US$779.5 million) print – with the guidelines ahead of pricing in March this year.

From NAB’s perspective, establishing an established framework for social bonds was an important step in the journey from a concept the issuer supported in principle to taking a transaction to market.

Eva Zileli, head of group funding at NAB in Melbourne, tells KangaNews the idea for the social-bond transaction originated with the bank’s capital-financing team. But the concept quickly won the backing of group treasury, which added its weight to the product-development effort. “It’s certainly a concept I support personally and one we embrace as a business. But of course as much as we like the idea we also have to have absolute confidence in it from a funding perspective,” Zileli says.

This means the bank was keen to establish a platform suitable for repeat use. “Once we decided to pursue a deal we further developed our existing climate-bond framework specifically for social bonds and were mindful of using this framework for additional SRI issuance,” Zileli comments. “This meant working with our legal and capital-financing teams to develop a robust product that adheres to the ICMA green-bond principles for social bonds.”

Establishing credibility

As has been the case in the Australian green-bond market, the emphasis during the development of NAB’s social bond was on creating a product with unimpeachable SRI credentials. This started with the ICMA principles and also encompassed the use of third-party verification as well as a conservative approach to the volume printed relative to scale of qualifying assets.

When it comes to external review, Jenkins explains: “We looked at what else was out there and found some precedents offshore, especially for social bonds issued by UK and European banks. These used similar processes to what we have seen in the green-bond sector, with second opinions provided by Sustainalytics. Sustainalytics has credibility in this space – we see it as having a similar position in social bonds to that of Cicero in the early green-bond market.”

EY also provided financial assurance on the NAB social bond. This additional layer of third-party review was once again part of NAB’s view that, as Jenkins puts it, “for a new product in Australia it was appropriate that we set the highest benchmark for compliance available”.

He adds: “Through the whole process we felt it was vital to be able to articulate the purpose of the bond and how it would deliver on this purpose. The use of third-party opinion really added to the strength of this message, which also allowed investors to have certainty and comfort in advance. Most of all, we couldn’t risk an unsuccessful transaction or one that didn’t pass the reputational or credibility tests.”

Establishing the transaction’s purpose and value is a critical element of the external review process. “For us, the first thing to understand when we look at a potential transaction like this is the issuer’s objectives,” Secreteanu tells KangaNews.

There is a degree of complexity here. Unlike green-bond issuance, Secreteanu adds, the NAB social bond is not funding specific projects but instead focuses on general business lending to companies that are leaders in gender equality in the workplace.

She comments: “Sustainalytics performs its own ESG [environmental, social and governance] analysis so we have a view on what companies should do to qualify for social-bond inclusion. But we also believe that the WGEA certification is an extremely thorough process. It is certainly very helpful to have such a robust local benchmark as the starting point for an issuer like NAB.”

As well as WGEA certification, Secreteanu reveals, companies included in the NAB social-bond pool have to pass a number of negative screens – often relating to ESG issues other than gender equality. These exclusionary screens prevent lending to companies involved in high-level ESG controversies as well as involvement in sectors or activities like controversial weapons, tobacco or live-animal transportation.

Ongoing reporting

It will not be sufficient for end borrowers to tick the ESG boxes ahead of the social bond’s pricing. Sustainalytics will provide an annual verification update on the social bond, and NAB will also produce impact reporting on an annual basis. Jenkins comments: “Impact reporting is still evolving even in the green-bond world, and the story is the same in the social space. We are looking to follow the precedents from the green-bond market, especially around case studies.”

This should also provide a pathway for future deals, including the WGEA accreditation and ESG overlay. Secreteanu adds: “Subsequent to issuance we will also provide an annual review, to demonstrate that companies continue to comply with the requisite criteria and to examine the bond’s impact. This annual report was commissioned to be publicly available, to support investor confidence in the use of funds on an ongoing basis”

The fact that NAB’s bond is not project-based also makes the post-issuance review task more nuanced, Secreteanu says. End borrowers have to continue to comply with inclusion criteria, but as these include requirements such as being in line with or better than industry best practice it may be necessary for companies to enhance their practices related to gender equality even during the life of the bond.

Finding assets

As has been the case with Australian green bonds, social-bond deal sources suggest the biggest challenge may have been identifying qualifying assets and working with end borrowers to secure their support for the funding outcome.

The asset pool NAB identified as being suitable for gender-equality bond issuance already stands at A$1 billion, Waddell reveals. Some of the total pool will be retained as effective overcollateralisation in the event that other assets lose qualification status – though Waddell is quick to point out that the bank regards this as unlikely.

There is also expansion potential. “We are seeing ongoing growth in the gender-equality portfolio as a larger cohort of companies upgrade their policies. There is also system growth as the borrowers that already qualify themselves grow and require more financing,” Waddell explains.

Having the assets was not sufficient to create a social-bond pool, though. Waddell explains that NAB was convinced it was imperative to offer investors the “high-water mark in disclosure” to ensure the success of the deal. In the gender-equality space, this meant being able to offer maximum transparency around where proceeds would be lent, even though most of the end borrowers are not directly active in capital markets.

Specifically, NAB had to persuade its borrowing clients to allow their names and funding positions to be disclosed to investors, so the social bond could demonstrate that its proceeds were being used to fund only entities with appropriately high standards.

“This was clearly the most time-consuming part of the process, but it is the only way to ensure optimal investor buy-in and thus benefits for the borrowers themselves,” Waddell tells KangaNews. “It also means investors are able not only to allocate to firms that are doing the right thing, but also invest in names that aren’t usually available to them. You don’t typically see an accountancy firm, for instance, in the debt market.”

After initial soundings just a handful of the clients NAB had identified as suitable for the social-bond pool proved willing to allow the requisite level of transparency. However, by launch the list of borrower names had swollen to 14 – and Waddell says more have expressed interest in being involved in future deals subsequent to the debut pricing.

Investor growth

Finding buyers appears to have been easier. NAB’s social bond saw 61 per cent distribution to accounts explicitly seeking responsible or ethical assets, according to issuer data. This group comprised 8 per cent “dark” or specialist funds and 53 per cent “light” funds, or those with ethical overlays but not outright SRI mandates. By comparison, Jenkins reveals that NAB’s recent euro-denominated green bond saw 90 per cent distribution to dark or light green funds.

“We are seeing growth in SRI assets in Australia as fast as anywhere else in the world,” Waddell reveals. “Investors are getting on board with this story and momentum is growing constantly.”

Zileli echoes the view that issuers are responding to Australian SRI demand as it develops. She explains that the investor-engagement process around green and social funding is very much ongoing, as NAB attempts to understand how the buy side is thinking about the SRI component as part of its overall funds under management. In fact it was this contact that tipped the bank off to the fact that there could be demand for an SRI product outside the climate-change-mitigation sphere in the first place.

Even so, NAB took a cautious approach to the deal in terms of outright size and the volume of supporting assets. The bank launched a minimum A$300 million transaction and capped volume at A$500 million despite having excess demand in the book and a certified asset pool of A$1 billion.

“There was an overwhelmingly positive response from investors domestically and offshore, with real enthusiasm for the introduction of new SRI options,” Zileli says. “But we think it is vital to offer the highest product standards in a new asset class like this, including making sure we have sized the bond appropriately with regard to the reference pool.”

NAB achieved further investor diversification through the social bond, Zileli says. But the real benefit for the issuer was being able to align its funding goals with its broader enterprise ambitions (see box below).

Social finance: a whole-of-bank perspective

National Australia Bank (NAB) has been associated with some of the key breakthroughs in Australian green and social bonds, including being the first domestic issuer, lead-managing the first government-sector transaction and now issuing the first benchmark social bond. Steve Lambert, the bank’s Sydney-based executive manager, capital financing, tells KangaNews its environmental, social and governance (ESG) commitment goes well beyond a mere product push.

NAB has obviously committed significant resources to its involvement in the development of sustainable and socially responsible debt securities in Australia. What’s the bigger picture at the bank?

This is certainly part of a broader ESG commitment within NAB, and it also relates to the fact that we’re constantly working very hard to create product that the broadest group of investors wants to buy.

The bigger picture for us is that we have adopted a ‘shared-value’ approach to completely rethinking parts of our core business. This has involved creating products and services that address social and environmental issues, to give the investor community choice in how they invest their money in more meaningful ways.

I think this commitment is unusual for a bank. It is having real impact in areas like fair and affordable finance for individuals through our A$130 million (US$98.6 million) investment in microfinance and our development of the socially responsible investment (SRI) market.

There are wider trends at play. We are going through a long process of demystifying fixed income for noninstitutional investors, including giving access to a wider range of products.

Wider uses

As the green- and social-bond space matures in Australia, Waddell says the next step may be more consistent issuance. “Investor feedback has been that they would like to see a curve being filled in,” he tells KangaNews. “There is also some notable interest in adding floating-rate issuance to the mix.”

With this in mind, NAB continues to explore opportunities to issue social bonds to fund lending in other socially inclusive areas. “The challenge at present is finding loans in sufficient quantity to support a reference pool for other types of issuance,” Zileli comments. “Although we are not expecting our typical benchmark-sized Australian dollar deals, we view issuance size of around A$200-300 million as appropriate for these thematic bonds. For now there isn’t the volume of assets to issue in all sectors.”

While NAB clearly found it easier to identify and certify assets for a gender-equality product, Secreteanu points out that the ICMA social-bond guidelines can be applied to a range of outcomes including lending in the health, education and agriculture sectors. NAB only funded gender equality in this particular bond, but issuers can also combine multiple uses of proceeds into the same social-bond issuance.

This approach is already being taken in global markets. For instance, in March Communidad de Madrid mandated lead managers for its debut euro-denominated sustainable benchmark bond. According to Sustainalytics, the deal will align with the ICMA social-bond guidelines while funds raised will be used across affordable housing, education, healthcare, social and economic inclusion, SME financing, and climate-change and environmental management.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

New Zealand's market ready to step up as degree of difficulty grows

With a substantial infrastructure requirement looming and a weak economic environment, the New Zealand capital market will have to be on top of its game in the years ahead. Participants at KangaNews’s annual women in New Zealand capital markets roundtable discussed the issues at hand and how they believe a constructive ecosystem can be developed.

External support still the talking point in bank ratings review

The nature and likelihood of pre-failure external support for banks has been brought back into focus following an update to the methodology Moody’s Ratings uses to assess the Australian banking sector. Some banks do not believe the new analysis gives sufficient weight to the likelihood of external support before the point of failure – even for entities not deemed systemically important.