Credibility and additionality top investors’ AOFM GSS considerations

In the wake of the Australian federal government’s long-awaited decision to initiate the process toward the issuance of sovereign sustainability bonds, KangaNews surveyed local investors on what they want to see from a sovereign green-bond programme. The answers – and further detail provided by some buy-side accounts – show what the Australian Office of Financial Management may need to consider as it ramps up its preparation.

Helen Craig Head of Operations KANGANEWS

Laurence Davison Head of Content KANGANEWS

Speculation about issuance of Australian sovereign green, social and sustainability (GSS) bonds has been ongoing in the local capital market ever since the May 2022 federal election produced a government with a reality-based approach to climate policy. The Australian Office of Financial Management (AOFM) has conducted preparatory work but repeatedly stated that the green light could only come from government.

The federal treasurer, Jim Chalmers, flipped the switch on 21 April this year when, following the government’s second investor roundtable, he confirmed plans to introduce a sovereign green-bond programme starting with the development of a framework and with debut issuance slated for mid-2024.

The May federal budget formalised the commitment, making A$8.3 million (US$5.5 million) over four years – and A$1.3 million annually on an ongoing basis – available to establish and maintain an issuance platform designed to “raise capital for environmental and climate change related programmes”.

In the wake of these announcements, KangaNews surveyed 20 Australian fixed-income investors on their enthusiasm, preferences and concerns about domestic sovereign GSS bonds. Their responses – and qualitative interviews conducted at the same time – may provide some hints as to how a programme and issuance from it emerges.

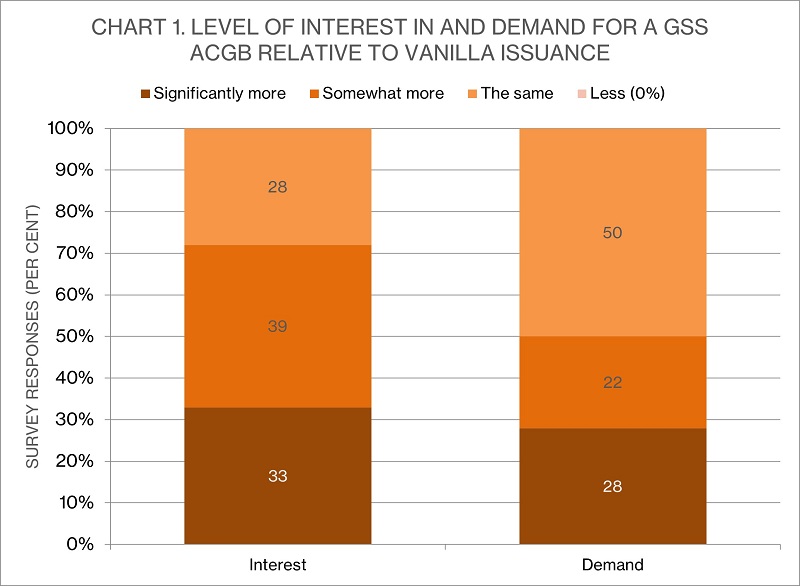

There is certainly engagement with the forthcoming labelled programme. Nearly three-quarters of investors responding to the survey say they have a degree of interest in what the AOFM does and half said they expect to have at least some more demand for a GSS line than a vanilla AOFM syndication (see chart 1).

Source: KangaNews 16 May 2023

Marayka Ward, director, fixed income strategy at QIC in Brisbane, argues that an Australian sovereign bond will bring many positives. “A use-of-proceeds [UOP] structure will give investors comfort that the risk of unwinding sustainability efforts is minimised,” she tells KangaNews. “It will also provide visibility on the projects contributing to Australia’s Paris Agreement goals and clarity on the commitments being made, particularly bearing in mind that sometimes the pathway is hard to see.”

On volume of demand specifically, Tamar Hamlyn, Sydney-based principal and portfolio manager, interest rate strategies and macroeconomics at Ardea Investment Management, says: “We would have more demand all else being equal, though demand remains capped by underlying allocations to the sector. Significantly more demand would likely be associated with additional asset allocation to the sector by end-investors and asset owners – that is, an inflow of new money and not just pricing preferences of existing capital allocated to the sector.”

“We want sustainable finance to unlock new opportunities and provide step changes. Ideally, successful green bonds incentivise the launch of more green bonds and more new projects to be included in them.”

Button TextISSUANCE CREDIBILITY

Hamlyn adds that he believes this type of capital inflow is possible, but it will likely depend on how end-investors perceive the AOFM’s programme in the lead-up to a debut transaction.

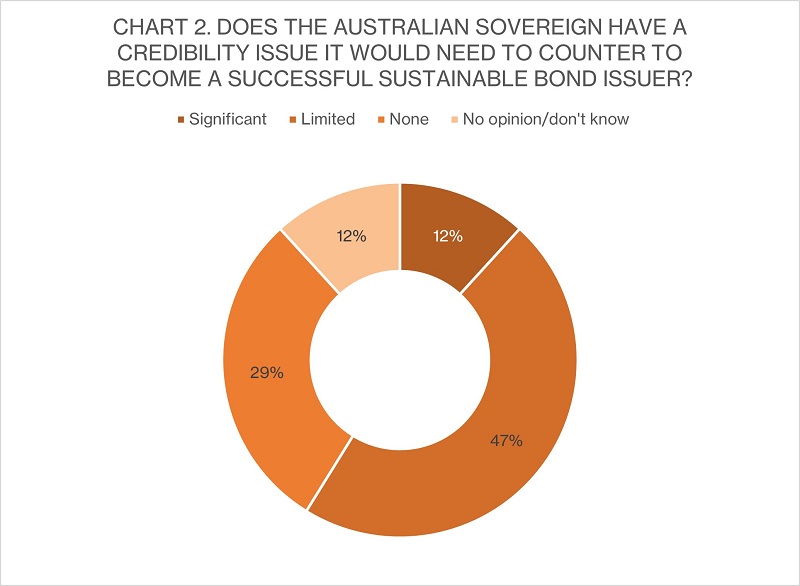

Investors repeatedly refer to the word “credibility” when discussing an Australian sovereign GSS programme. The issue is particularly acute for Australia given the prevalence of the resources sector in its economic mix and the lamentable policy backdrop of the years before the last federal election. More than half the investors responding to the KangaNews survey believe the Australian government needs to deal with a credibility issue in its GSS planning, though most of these believe the issue is limited in scale (see chart 2).

Source: KangaNews 16 May 2023

Adrian Janschek, portfolio manager at First Sentier Investors in Sydney, acknowledges that Australia’s “well-known environmental perception issues” make labelled issuance “somewhat of a political novelty in the first instance”. But he also believes progress is being made at the policy level including a clear direction being set, such that the AOFM should not be afraid to sell a positive story.

Hamlyn’s level of concern is greater. He explains: “The credibility issues are unfortunately significant. There is a risk that the domestic market underappreciates the extent of international negative perception about Australia’s enabled emissions.”

There could be a two-way effect here, whereby a sovereign programme either helps improve investor perception of Australia’s environmental commitments or suffers because of that perception. If the former outcome is to be achieved, investors say, it is vital that the programme be regarded as impactful and that GSS funding provides additionality.

George Bishay, head of credit and sustainable strategies at Pendal Group in Sydney, says his firm is “excited” about Australian sovereign sustainability issuance but notes that “not all green bonds are equal”. Specifically, he highlights the difference between a programme that refinances existing infrastructure versus one that responds to future needs.

Pendal will be seeking four key pillars from an AOFM programme. These are that it supports new projects and encourages future ones, that it funds “more risky projects” with the potential for bigger impact, that the government sets expectations for meaningful and measurable impact reporting, and that there is an accompanying and ongoing commitment toward environmental concerns.

Bishay suggests a labelled bond programme is in and of itself a statement of intent with regard to the latter expectation. In effect, he argues, expressing interest in issuing a green bond is a signal to the market that the federal government is taking investments into climate stability and the energy transition seriously.

Overall, Bishay says: “We want sustainable finance to unlock new opportunities and provide step changes. Ideally, successful green bonds incentivise the launch of more green bonds and more new projects to be included in them.”

He adds: “Governments should be funding revolutionary and speculative projects that help raise the tide and bring about a different, positive future. We are seeking projects that support new technologies and alternative energy: the production of hydrogen, renewable projects, large-scale batteries, maintaining biodiversity and climate-change adaptation.”

Ward agrees that the AOFM should be focused on additionality. “We would like to see support for some of the technologies we know exist and that are required to influence climate change, but that are not yet commercialised,” she says.

“It is crucial that the AOFM launches an issue of sufficient size to create as much liquidity as possible in the first instance, and it would be helpful if real-money investors have some repo capability to enhance tradability. Failure to achieve this means the free float is lower immediately, especially because ESG investors are limited in their activity.”

Button TextMARKET CONSIDERATIONS

Chalmers’ original announcement refers specifically and exclusively to green bonds, as do the budget papers – which also only mention climate and environmental commitments as the UOP. But investors say UOP could – and perhaps should – stretch beyond environmental.

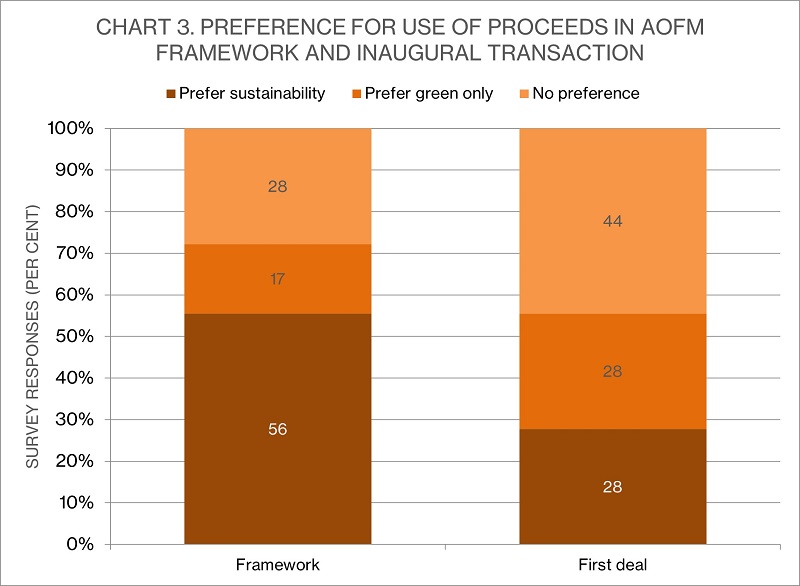

However, there is clear preference in the investor base for a sustainability framework that incorporates green and social UOP: 56 per cent of survey responses favour a sustainability framework while just 17 per cent favour green only (see chart 3). Bishay, for instance, notes Pendal’s interest in sustainability bonds that incorporate social outcomes like energy-efficient social housing as well as ‘pure’ green product.

Investors appear to be suggesting the AOFM opts for flexibility in its framework rather than demanding sustainability over green bonds, as there is much less concern about the format of a debut transaction. Nearly half the investors who responded to the KangaNews survey have no preference between a green bond and a sustainability bond for the first transaction, and those that do express a preference are evenly divided between the two.

There is also a practical consideration. Hamlyn says Ardea favours a green and social asset pool simply to ensure it is initially large enough and can continue to grow at increments sufficient in scale to support an ongoing programme of additional issuance. Narrowly defined green bonds may not be sufficient to achieve this, Hamlyn suggests.

There is clearly a degree of focus in the investor base on the liquidity prospects for AOFM GSS issuance. Opinions in the survey are relatively equally divided between those that expect such issuance to be as liquid as vanilla Australian Commonwealth government bonds (ACGBs) and those that anticipate tighter liquidity based on the likely makeup of the investor base.

Source: KangaNews 16 May 2023

Source: KangaNews 16 May 2023

There is clearly a degree of focus in the investor base on the liquidity prospects for AOFM GSS issuance. Opinions in the survey are relatively equally divided between those that expect such issuance to be as liquid as vanilla Australian Commonwealth government bonds (ACGBs) and those that anticipate tighter liquidity based on the likely investor base.

“It is likely to have lower liquidity, given the flow would be very much one-way as ESG [environmental, social and governance]-constrained investors tend to buy and hold as part of their asset allocation,” Janschek suggests. “In other words, dealers are less likely to go short if they think they might struggle to get the bonds back.”

The advice is that the AOFM seeks to build line size quickly. Janschek continues: “It is crucial that the AOFM launches an issue of sufficient size to create as much liquidity as possible in the first instance, and it would be helpful if real-money investors have some repo capability to enhance tradability. Failure to achieve this means the free float is lower immediately, especially because ESG investors are limited in their activity: they can't switch into another labelled maturity either near or far away on the curve, because they simply don't exist.”

Janschek recommends that the AOFM publicly consider the idea of issuing GSS bonds at liquid grid points – for instance three-, five-, seven- and 10-year tenors – such that switching by investors and traders becomes an option. Even so, he believes the very specific characteristics of ESG issuance will likely preclude such bonds being included in futures baskets.

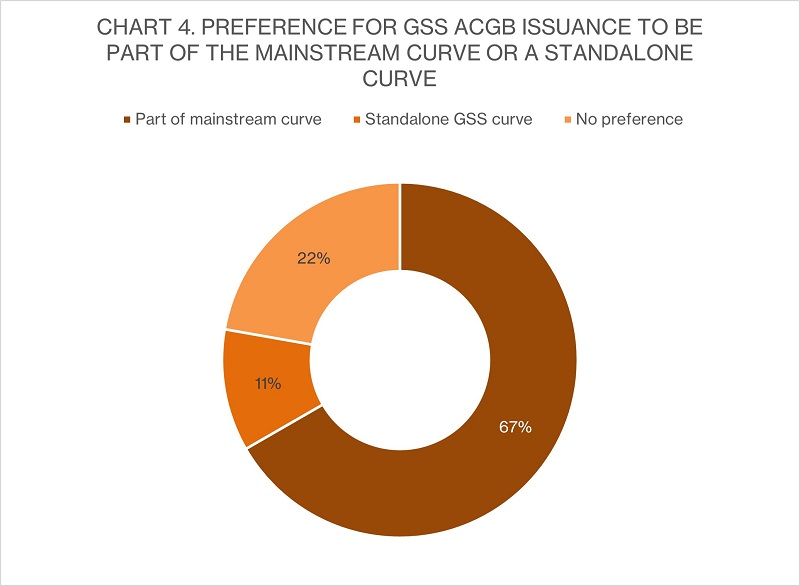

At the same time, two-thirds of investors responding to the KangaNews survey want forthcoming GSS ACGB lines to form part of the mainstream curve rather than standing alone as a separate programme (see chart 4). The approach taken on this issue has divided Australasian sovereign-sector issuers: the Australian states that have issued to date tend to view their GSS bonds as apart from their mainstream curves, whereas New Zealand Debt Management includes its first green bond among its vanilla price points – as will Western Australian Treasury Corporation when it debuts in June.

“There are arguments in favour of both approaches but ultimately they are not really that different, as the underlying credit is the same,” Hamlyn suggests. “The German approach of ‘pair’ bonds – which allows for direct comparability while building a standalone green curve – may have some benefits for funds that can only invest in sustainable issuance.”

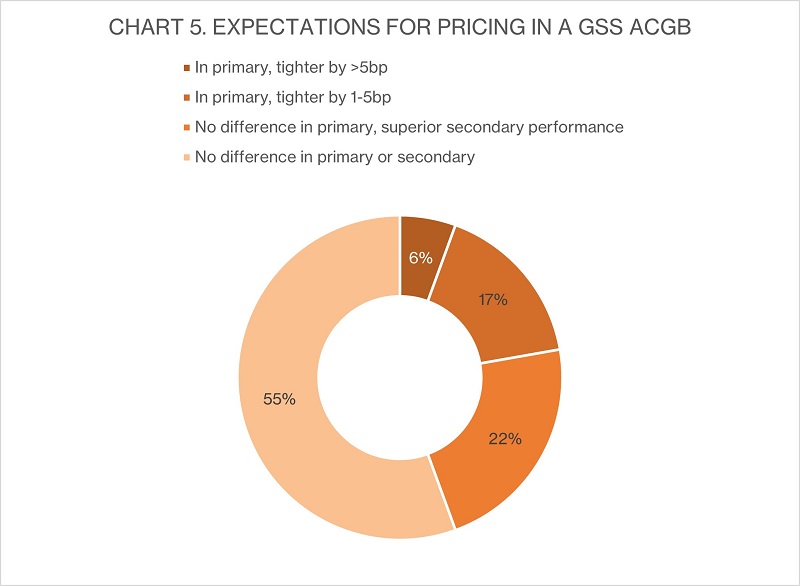

Whether included in the mainstream curve or not, if investors are correct the AOFM should not expect its GSS bonds to be pricing outliers. Just less than one-quarter of investors expect somewhat tighter primary pricing – though most of these anticipate just a few basis points of difference from vanilla issuance – and roughly the same number anticipate superior secondary price action (see chart 5). But the majority expect GSS ACGBs to behave exactly the same as mainstream bonds when it comes to pricing.

Source: KangaNews 16 May 2023

Ward believes a sovereign green bond might help alleviate concern about greenwashing and greenhushing in the wider market. But, once again, credibility will be critical – and doubly so if the AOFM hopes to achieve superior pricing.

“It is very important to support words with actions. There will always be technologies or projects that fail, and targets that are missed. The key is to address them honestly. Market users talk about the concept of a greenium and there is often a pricing incentive for these structures – but it is therefore imperative that they are issued for the right reasons.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news